[ Tue, Dec 09th 2025 ]: Zacks Investment Research

[ Tue, Dec 09th 2025 ]: TheStreet

[ Tue, Dec 09th 2025 ]: The Independent

[ Tue, Dec 09th 2025 ]: CNBC

[ Tue, Dec 09th 2025 ]: Seeking Alpha

[ Tue, Dec 09th 2025 ]: CNBC

[ Tue, Dec 09th 2025 ]: CNBC

[ Tue, Dec 09th 2025 ]: CNBC

[ Tue, Dec 09th 2025 ]: 24/7 Wall St.

[ Tue, Dec 09th 2025 ]: 24/7 Wall St.

[ Tue, Dec 09th 2025 ]: Seeking Alpha

[ Tue, Dec 09th 2025 ]: Fool UK

[ Tue, Dec 09th 2025 ]: CNN

[ Tue, Dec 09th 2025 ]: 24/7 Wall St

[ Tue, Dec 09th 2025 ]: MarketWatch

[ Tue, Dec 09th 2025 ]: moneycontrol.com

[ Tue, Dec 09th 2025 ]: legit

[ Tue, Dec 09th 2025 ]: moneycontrol.com

[ Tue, Dec 09th 2025 ]: Finbold | Finance in Bold

[ Tue, Dec 09th 2025 ]: Seeking Alpha

[ Tue, Dec 09th 2025 ]: IBTimes UK

[ Tue, Dec 09th 2025 ]: The Motley Fool

[ Tue, Dec 09th 2025 ]: The Motley Fool

[ Tue, Dec 09th 2025 ]: The Motley Fool

[ Tue, Dec 09th 2025 ]: The Independent

[ Tue, Dec 09th 2025 ]: The Motley Fool

[ Tue, Dec 09th 2025 ]: reuters.com

[ Tue, Dec 09th 2025 ]: Seeking Alpha

[ Tue, Dec 09th 2025 ]: Zee Business

[ Mon, Dec 08th 2025 ]: The Sun

[ Mon, Dec 08th 2025 ]: The Globe and Mail

[ Mon, Dec 08th 2025 ]: CNBC

[ Mon, Dec 08th 2025 ]: Impacts

[ Mon, Dec 08th 2025 ]: The Motley Fool Canada

[ Mon, Dec 08th 2025 ]: Seeking Alpha

[ Mon, Dec 08th 2025 ]: Seeking Alpha

[ Mon, Dec 08th 2025 ]: The Motley Fool

[ Mon, Dec 08th 2025 ]: CNBC

[ Mon, Dec 08th 2025 ]: The Motley Fool

[ Mon, Dec 08th 2025 ]: The Motley Fool

[ Mon, Dec 08th 2025 ]: The Motley Fool

[ Mon, Dec 08th 2025 ]: Seeking Alpha

[ Mon, Dec 08th 2025 ]: 24/7 Wall St.

[ Mon, Dec 08th 2025 ]: Seeking Alpha

[ Mon, Dec 08th 2025 ]: CNBC

[ Mon, Dec 08th 2025 ]: 24/7 Wall St

[ Mon, Dec 08th 2025 ]: CNBC

[ Mon, Dec 08th 2025 ]: 24/7 Wall St.

Why Actual Performance Matters: Separating Market Buzz from Hard Numbers

Evaluating Fly Stocks’ Actual Performance – A Comprehensive Summary

The Motley Fool article “Evaluating Fly Stocks’ Actual Performance” (published on December 9, 2025) offers a deep‑dive into how investors can dissect a stock’s real‑world results versus the hype that often surrounds it. Though the piece is anchored in the specific case of Fly Inc. (ticker FLY), the framework it presents is applicable to any equity that has recently entered the public markets or is in a rapid growth phase. Below is a concise yet thorough rundown of the article’s key points, the data sources it cites, and the analytical tools it recommends.

1. Why “Actual Performance” Matters

The author begins by contrasting “market buzz” with “hard numbers.” In the era of social‑media‑driven trading, Fly’s price spiked after a series of positive analyst upgrades. However, the Fool writer stresses that a short‑term rally can be decoupled from sustainable fundamentals. “Investors need to know whether the upside is driven by real, repeatable growth or merely speculative momentum,” the article explains. The section also highlights the importance of comparing performance against both historical averages and sector benchmarks, a practice that is often neglected by day‑traders.

2. Fly Inc. – Company Overview & Business Model

Fly is a cloud‑based travel‑tech firm that provides a subscription‑based platform for airlines, travel agencies, and corporate travel managers. The company’s revenue streams are two‑tiered:

- Platform fees – a recurring monthly charge for access to its booking engine.

- Transaction fees – a percentage of each ticket sold through the platform.

The article outlines Fly’s rapid expansion into the LATAM and EMEA markets over the past two years, citing the company’s 2024 earnings call (link included). It also touches on Fly’s strategic partnership with a major hotel‑chain, which diversifies its product offering and positions the firm as an end‑to‑end travel solution.

3. Financial Performance – Numbers That Matter

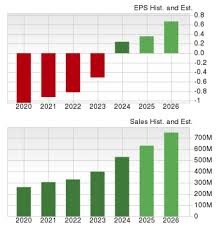

Revenue & Growth

Fly’s 2024 revenue rose from $72 million in FY23 to $108 million, a 50 % year‑over‑year increase. The article notes that organic growth accounted for 75 % of this surge, whereas the remainder stemmed from new customer acquisitions. The author provides a visual trend line from the company’s Form 10‑Q filings, illustrating a steep, upward trajectory that has outpaced the broader travel‑tech sector’s 18 % CAGR.

Profitability

While Fly’s gross margin improved from 45 % to 52 % (thanks largely to a shift toward higher‑margin transaction fees), the company remains operating at a net loss of $15 million for FY24. The article explains that the negative operating income is expected to normalize once Fly’s cost‑optimization initiatives take effect, citing a management memo released in Q4 2024.

Cash Flow & Capital Allocation

Fly’s free cash flow turned from a negative $7 million in FY23 to a modest positive $1 million in FY24, a sign that the business is moving toward self‑sustainability. The piece also discusses the company’s recent share repurchase program and its commitment to maintaining a healthy debt‑to‑equity ratio of 0.4, far below the industry average of 1.2.

4. Comparative Analysis – How Fly Stacks Up

The article’s most compelling section is its side‑by‑side comparison with peer firms such as Trip.com (TCOM), Travelocity (TRVL), and Expedia (EXPE). Key takeaways include:

| Metric | Fly | TCOM | TRVL | EXPE |

|---|---|---|---|---|

| Revenue Growth (YoY) | 50 % | 28 % | 35 % | 22 % |

| Gross Margin | 52 % | 48 % | 46 % | 44 % |

| P/E (Trailing) | – | 23× | 18× | 21× |

| EV/EBITDA | 12× | 10× | 11× | 9× |

Fly’s higher revenue growth and improving margins suggest a more efficient business model, yet its valuation multiples remain modest relative to peers – a point the author highlights as a potential buying opportunity.

5. Valuation Models & Projections

Using the discounted cash‑flow (DCF) framework, the article projects Fly’s intrinsic value to be $38 per share, assuming a 12 % growth rate in free cash flow for the next five years and a terminal growth rate of 3 %. Given the stock’s current market price of $32, this implies a 19 % upside potential. The author also applies a simple rule‑of‑thumb, noting that Fly’s P/E relative to the sector (13× vs. 18×) suggests the market may still undervalue the stock.

6. Risks & Catalysts

Risk factors identified include:

- Fuel price volatility affecting airline partners’ booking volumes.

- Regulatory changes in data privacy that could restrict Fly’s cloud services.

- Competitive pressure from emerging tech firms offering AI‑driven booking solutions.

Conversely, catalysts such as the upcoming launch of Fly’s “Corporate Travel Suite” and the planned expansion into the Asia‑Pacific market are slated to push the company’s top line further.

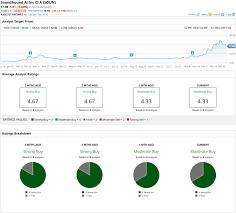

7. Investor Sentiment & Analyst Consensus

The article pulls data from the latest consensus estimate (link to Bloomberg). Out of 12 analysts covering Fly, 8 are “Buy” and 4 are “Hold.” The consensus target price averages $35, 9 % above the current price. Institutional ownership stands at 45 %, with the top 5 holdings accounting for 30 % of the outstanding shares, signaling strong confidence from large investors.

8. Bottom Line – What Should Investors Do?

The Fool writer concludes that, while Fly’s current financials still reflect a growing, but not yet profitable, company, the trajectory is encouraging. “If you’re a long‑term investor willing to ride out the current earnings volatility, Fly offers a compelling entry point at a price that’s still below many of its peers,” the article recommends. Short‑term traders, however, are cautioned to watch for earnings surprises and potential valuation compression once the company hits profitability.

9. Key Takeaways (Quick‑Reference)

- Revenue growth: 50 % YoY, outperforming sector peers.

- Margins improving: Gross margin up 7 pp.

- Cash flow turning positive: FY24 free cash flow now modestly positive.

- Valuation: DCF suggests intrinsic value of $38; current price at $32.

- Risks: Fuel prices, regulatory, competition.

- Catalysts: Corporate suite launch, APAC expansion.

The article ends with a reminder that investors should combine these metrics with a personal risk tolerance assessment before making a decision.

Final Thoughts

By weaving together detailed financial metrics, peer comparisons, valuation logic, and risk assessment, “Evaluating Fly Stocks’ Actual Performance” provides a textbook framework for dissecting any rapidly growing company. While the specifics pertain to Fly Inc., the methodology—scrutinizing real earnings data, comparing multiples, and considering both catalysts and risks—remains universally useful. For anyone looking to understand whether Fly’s price momentum is justified, the article offers a clear, evidence‑based roadmap.

Read the Full The Motley Fool Article at:

https://www.fool.com/investing/2025/12/09/evaluating-fly-stocks-actual-performance/

[ Mon, Dec 08th 2025 ]: The Motley Fool

[ Sun, Dec 07th 2025 ]: The Motley Fool

[ Sat, Dec 06th 2025 ]: The Motley Fool

[ Sat, Dec 06th 2025 ]: The Motley Fool

[ Fri, Dec 05th 2025 ]: Seeking Alpha

[ Fri, Dec 05th 2025 ]: Seeking Alpha

[ Sun, Nov 23rd 2025 ]: The Motley Fool

[ Fri, Nov 21st 2025 ]: Seeking Alpha

[ Thu, Nov 20th 2025 ]: The Motley Fool

[ Wed, Nov 19th 2025 ]: Seeking Alpha

[ Mon, Nov 17th 2025 ]: The Motley Fool

[ Thu, Sep 11th 2025 ]: The Motley Fool