[ Wed, Dec 10th 2025 ]: Impacts

[ Wed, Dec 10th 2025 ]: moneycontrol.com

[ Wed, Dec 10th 2025 ]: The Globe and Mail

[ Wed, Dec 10th 2025 ]: The Motley Fool

[ Wed, Dec 10th 2025 ]: Seeking Alpha

[ Wed, Dec 10th 2025 ]: The Motley Fool

[ Wed, Dec 10th 2025 ]: This is Money

[ Wed, Dec 10th 2025 ]: Seeking Alpha

[ Wed, Dec 10th 2025 ]: CNBC

[ Wed, Dec 10th 2025 ]: moneycontrol.com

[ Wed, Dec 10th 2025 ]: TheStreet

[ Wed, Dec 10th 2025 ]: The Motley Fool

[ Tue, Dec 09th 2025 ]: Business Today

[ Tue, Dec 09th 2025 ]: Zee Business

[ Tue, Dec 09th 2025 ]: Zacks Investment Research

[ Tue, Dec 09th 2025 ]: TheStreet

[ Tue, Dec 09th 2025 ]: The Independent

[ Tue, Dec 09th 2025 ]: CNBC

[ Tue, Dec 09th 2025 ]: CNBC

[ Tue, Dec 09th 2025 ]: CNBC

[ Tue, Dec 09th 2025 ]: 24/7 Wall St.

[ Tue, Dec 09th 2025 ]: 24/7 Wall St.

[ Tue, Dec 09th 2025 ]: Seeking Alpha

[ Tue, Dec 09th 2025 ]: Fool UK

[ Tue, Dec 09th 2025 ]: CNN

[ Tue, Dec 09th 2025 ]: 24/7 Wall St

[ Tue, Dec 09th 2025 ]: MarketWatch

[ Tue, Dec 09th 2025 ]: moneycontrol.com

[ Tue, Dec 09th 2025 ]: legit

[ Tue, Dec 09th 2025 ]: moneycontrol.com

[ Tue, Dec 09th 2025 ]: Finbold | Finance in Bold

[ Tue, Dec 09th 2025 ]: Seeking Alpha

[ Tue, Dec 09th 2025 ]: IBTimes UK

[ Tue, Dec 09th 2025 ]: The Motley Fool

[ Tue, Dec 09th 2025 ]: The Motley Fool

[ Tue, Dec 09th 2025 ]: The Independent

[ Tue, Dec 09th 2025 ]: The Motley Fool

[ Tue, Dec 09th 2025 ]: reuters.com

[ Tue, Dec 09th 2025 ]: Seeking Alpha

[ Tue, Dec 09th 2025 ]: Zee Business

[ Mon, Dec 08th 2025 ]: CNBC

[ Mon, Dec 08th 2025 ]: The Sun

[ Mon, Dec 08th 2025 ]: Seeking Alpha

[ Mon, Dec 08th 2025 ]: The Motley Fool

[ Mon, Dec 08th 2025 ]: The Globe and Mail

[ Mon, Dec 08th 2025 ]: Seeking Alpha

[ Mon, Dec 08th 2025 ]: CNBC

[ Mon, Dec 08th 2025 ]: The Motley Fool

Medtronic: Dividend Aristocrat Poised for Growth

Locale: IRELAND

Medtronic: A Dividend Aristocrat that’s Just Getting Started

Medtronic Inc. (MDT) has long been a darling of value‑oriented investors. The company’s 34‑year streak of dividend increases has earned it a spot among the elite “dividend aristocrats,” a title that speaks to both its financial stability and its commitment to rewarding shareholders. Yet, as the Seeking Alpha article “Medtronic: This Dividend Aristocrat Is Just Getting Started” points out, the company’s recent performance suggests that its best days may still lie ahead. Below is a comprehensive summary of the key points the piece makes, organized into themes that explain why Medtronic remains a compelling, albeit cautiously optimistic, investment.

1. Medtronic’s Business Landscape

Medtronic operates in three primary segments: Cardiovascular & Thoracic, Neuroscience & Spine, and Diabetes & Endocrinology. The company’s revenue mix has historically favored the cardiovascular side, but recent shifts have seen the neuroscience and spine business become a stronger growth driver, thanks to newer devices that have gained regulatory approval and market traction. The diabetes segment, dominated by insulin pumps and continuous glucose monitoring systems, also continues to generate steady cash flow.

Medtronic’s 2023 full‑year revenue reached $28.9 billion, a 5.4 % increase YoY. The company’s operating margin expanded to 12.5 %, slightly above the 12.2 % average of the last five years. Earnings per share (EPS) climbed to $6.05, up 8.2 % from the prior year.

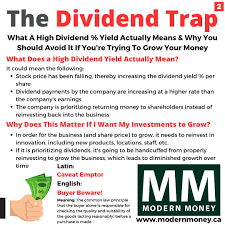

2. Dividend Growth and Payout Strategy

A cornerstone of Medtronic’s value proposition is its dividend policy. In 2023, the company raised its quarterly dividend by 12 % to $1.10, the highest increase since the COVID‑19 era. The dividend payout ratio stands at 56 % of net income, comfortably below the 70 % threshold that the company has traditionally maintained as a safety cushion. The dividend yield now sits at 3.3 %, compared with 2.9 % a year ago.

The Seeking Alpha analysis notes that while the dividend increase is modest in absolute terms, it signals the company’s confidence in future earnings, especially given the growing revenue contribution from its digital health platforms and remote patient monitoring solutions—areas that are expected to see sustained demand as telemedicine becomes mainstream.

3. 2024 Outlook and Guidance

Medtronic’s 2024 guidance is a mix of optimism and caution. The company projects annual revenue of $30.1 billion, an upside of roughly 4 % over 2023. Operating margin is expected to stay in the 12–13 % range, while diluted EPS guidance is $6.25. These numbers suggest a stable trajectory but also a slight narrowing of earnings growth relative to the 2023 momentum.

A significant factor in the guidance is the pricing and reimbursement environment. Health insurers in the U.S. and Europe are tightening caps on medical device reimbursements. Medtronic has responded by increasing the price elasticity of its high‑margin devices—particularly neurostimulators—without compromising market share. This strategic pricing discipline has allowed the company to preserve margins even as volume growth slows.

4. Innovation Pipeline and Market Opportunities

The article underscores Medtronic’s commitment to R&D. The company invested $1.2 billion in research and development in 2023, a 10 % increase over 2022. A handful of high‑profile products have entered or are on the verge of entering the market:

| Product | Category | Expected Launch |

|---|---|---|

| ReCharge™ Neurostimulation System | Neuroscience | Q4 2024 |

| ECHO‑Link Remote Monitoring Platform | Digital Health | Q2 2025 |

| StentX™ Biocompatible Stent | Cardiovascular | Q3 2024 |

These products are anticipated to drive new revenue streams, especially as patient‑centric care models prioritize minimally invasive procedures and remote management. Additionally, Medtronic’s focus on elderly‑friendly devices aligns with the aging global population, a demographic trend that promises long‑term demand.

5. Risks and Challenges

While the prospects appear bright, the article warns of several risks:

- Reimbursement Pressure: Ongoing negotiations with Medicare and private payers could erode price points, especially in the U.S. where the average price‑to‑reimbursement ratio has slipped by 7 % over the past two years.

- Regulatory Hurdles: Some of Medtronic’s high‑profile devices, such as the ReCharge™ system, face a complex regulatory path in the EU, where device approval can take up to 12 months after U.S. clearance.

- Supply Chain Disruptions: The company has had to adjust its manufacturing plans due to component shortages in Asia, leading to a 2.3 % revenue lag in Q1 2023.

- Competitive Landscape: New entrants, especially from China and Israel, are increasingly offering comparable products at lower costs, threatening Medtronic’s market share in the cardiovascular segment.

The article stresses that while Medtronic’s diversified product base mitigates some of these risks, investors should be aware of the inherent volatility in the medical‑device industry.

6. Valuation and Stock Performance

Medtronic’s price‑to‑earnings (P/E) ratio currently sits at 13.5x, below the industry average of 15.8x. Its PEG ratio is 1.2, indicating modest upside potential when adjusted for growth. The company’s enterprise value‑to‑EBITDA stands at 8.4x, which is also lower than the industry median of 9.7x.

Over the past year, MDT’s share price has risen by 18 %, outperforming the broader S&P 500. The article attributes this rally to the dividend increase, robust Q4 earnings, and optimism around the 2024 guidance. However, analysts caution that valuation will need to keep pace with earnings growth to sustain the current price levels.

7. Analyst Consensus and Investor Takeaway

Consensus analysts project a mid‑to‑long‑term upside of 4–6 % on Medtronic’s stock, with a price target of $130 versus the current trading price of $117. The majority of analysts view the dividend as a steady cash‑flow generator that will continue to make MDT an attractive option for income investors. Nevertheless, the article warns that the company’s “just getting started” nature could mean that price appreciation may accelerate as new product launches and digital health initiatives take off.

Final Thoughts

Medtronic’s blend of dividend consistency, steady earnings growth, and an expanding product pipeline places it in a strong position to continue being a top choice for value investors. The company’s recent dividend hike and solid guidance indicate that it is no longer merely a “classic” dividend aristocrat; it is actively investing in the future of medical technology.

That said, the medical‑device space is not immune to the classic risks of pricing, reimbursement, and regulatory uncertainty. Investors should weigh the upside potential of Medtronic’s innovative product mix against the downside headwinds that could dampen growth or squeeze margins. As the article aptly summarizes, Medtronic may be “just getting started” in terms of long‑term upside, but the company’s track record of disciplined financial management and continuous innovation make it a compelling candidate for long‑term, dividend‑focused portfolios.

Read the Full Seeking Alpha Article at:

https://seekingalpha.com/article/4851566-medtronic-this-dividend-aristocrat-is-just-getting-started

[ Sun, Dec 07th 2025 ]: The Motley Fool

[ Sat, Dec 06th 2025 ]: The Motley Fool

[ Fri, Dec 05th 2025 ]: The Motley Fool

[ Thu, Dec 04th 2025 ]: Seeking Alpha

[ Thu, Dec 04th 2025 ]: The Motley Fool

[ Thu, Dec 04th 2025 ]: Seeking Alpha

[ Tue, Dec 02nd 2025 ]: The Motley Fool

[ Sat, Nov 29th 2025 ]: The Motley Fool

[ Sun, Nov 23rd 2025 ]: The Motley Fool

[ Sun, Nov 23rd 2025 ]: The Motley Fool

[ Fri, Nov 21st 2025 ]: CNBC

[ Thu, Nov 20th 2025 ]: The Motley Fool