[ Yesterday Evening ]: The Motley Fool

[ Yesterday Evening ]: The Motley Fool

[ Yesterday Evening ]: The Motley Fool

[ Yesterday Afternoon ]: The Motley Fool

[ Yesterday Afternoon ]: The Motley Fool

[ Yesterday Morning ]: The Motley Fool

[ Yesterday Morning ]: The Motley Fool

[ Yesterday Morning ]: The Motley Fool

[ Yesterday Morning ]: The Motley Fool

[ Yesterday Morning ]: The Motley Fool

[ Yesterday Morning ]: The Motley Fool

[ Last Friday ]: The Motley Fool

[ Last Friday ]: The Motley Fool

[ Last Friday ]: The Motley Fool

[ Last Friday ]: The Motley Fool

[ Last Friday ]: The Motley Fool

[ Last Friday ]: The Motley Fool

[ Last Friday ]: The Motley Fool

[ Last Friday ]: The Motley Fool

[ Last Friday ]: The Motley Fool

[ Last Friday ]: The Motley Fool

[ Last Friday ]: The Motley Fool

[ Last Thursday ]: The Motley Fool

[ Last Thursday ]: The Motley Fool

[ Last Thursday ]: The Motley Fool

[ Last Thursday ]: The Motley Fool

[ Last Thursday ]: The Motley Fool

[ Last Thursday ]: The Motley Fool

[ Last Thursday ]: The Motley Fool

[ Last Thursday ]: The Motley Fool

[ Last Thursday ]: The Motley Fool

[ Last Thursday ]: The Motley Fool

[ Last Thursday ]: The Motley Fool

[ Last Thursday ]: The Motley Fool

[ Last Thursday ]: The Motley Fool

[ Last Thursday ]: The Motley Fool

[ Last Thursday ]: The Motley Fool

[ Last Wednesday ]: The Motley Fool

[ Last Wednesday ]: The Motley Fool

[ Last Wednesday ]: The Motley Fool

[ Last Wednesday ]: The Motley Fool

[ Last Wednesday ]: The Motley Fool

[ Last Wednesday ]: The Motley Fool

Nvidia Invests $2 Billion in AI Chip Startup Tenstorrent

Locales: UNITED STATES, TAIWAN PROVINCE OF CHINA

Santa Clara, CA - March 22, 2026 - Nvidia, the undisputed leader in graphics processing units (GPUs) and a key player in the artificial intelligence revolution, today announced a $2 billion investment in Tenstorrent, an innovative startup specializing in AI chip design. The move isn't simply an investment; it's a strategic acquisition of a significant stake that aims to integrate Tenstorrent's unique architecture into Nvidia's already powerful AI platform. This bold decision signals Nvidia's intent to not just maintain its dominance but to proactively shape the future of AI hardware, even as competition intensifies.

Beyond GPUs: A Diversification of AI Architecture

For years, Nvidia's GPUs have been the workhorse of the AI industry, powering everything from large language models (LLMs) like GPT-4 to complex image recognition systems. However, Tenstorrent isn't building another GPU. Instead, the company is pioneering a fundamentally different approach to AI chip architecture. While Nvidia's GPUs excel in parallel processing - handling many calculations simultaneously - Tenstorrent's designs prioritize efficient processing of specific AI workloads, potentially achieving greater performance with lower power consumption. Early reports suggest their architecture lends itself particularly well to sparse models, a growing area of focus in AI research aimed at reducing computational cost without sacrificing accuracy.

This is a critical distinction. The AI landscape is rapidly evolving. One-size-fits-all solutions are becoming less viable. Different AI applications - from generative AI to robotics to edge computing - demand optimized hardware. Nvidia's investment in Tenstorrent demonstrates an understanding that diversification of chip architecture is crucial to address this expanding range of requirements.

Competition Heats Up: The Race for AI Supremacy

The AI chip market isn't a static environment. Several companies are vying for market share, challenging Nvidia's long-held lead. AMD, with its Instinct line of GPUs, has been steadily gaining ground. Intel, leveraging its manufacturing capabilities, is also making significant inroads with its dedicated AI accelerators. Furthermore, a wave of startups, like Cerebras Systems and Graphcore, are developing specialized AI hardware designed to outperform traditional GPUs in specific areas. The recent surge in custom silicon development by major tech companies like Google (TPUs) and Amazon (Trainium) further intensifies the competitive pressure.

Nvidia's acquisition of a stake in Tenstorrent isn't just about technological innovation; it's about competitive defense. By embracing an alternative architecture, Nvidia mitigates the risk of being disrupted by a competitor with a superior solution for a specific AI application. It's a form of 'future-proofing' - ensuring that Nvidia can offer the optimal hardware for all AI workloads, regardless of how the field evolves. The move is reminiscent of Intel's earlier acquisitions aimed at diversifying beyond CPU architecture into areas like FPGA and AI acceleration.

Analysts Weigh In: A Smart Long-Term Play

"This is a textbook example of a dominant player strategically reinforcing its position," says Dr. Anya Sharma, lead AI hardware analyst at Tech Insights Group. "Nvidia isn't just buying technology; they're buying options. Tenstorrent's architecture provides a valuable hedge against future advancements and changing market demands. It also opens up opportunities for Nvidia to explore entirely new AI applications."

Other analysts point to the potential for synergistic integration. Nvidia's CUDA platform, the dominant programming model for GPUs, could be extended to support Tenstorrent's architecture, creating a unified AI development environment. This would lower the barrier to entry for developers and accelerate the adoption of Tenstorrent's technology.

The Future of AI Hardware: A Multi-Chip World?

This deal may foreshadow a future where AI systems rely on a heterogeneous mix of processors - GPUs, CPUs, and specialized AI accelerators like those developed by Tenstorrent. A single server may house multiple types of chips, each optimized for a particular task, working in concert to deliver optimal performance and efficiency. This represents a departure from the current trend of relying primarily on GPUs for all AI workloads.

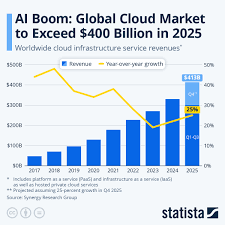

The $2 billion investment underscores the massive and accelerating growth projected for the AI chip market. Experts predict the market will exceed $400 billion by 2030, driven by the proliferation of AI in virtually every industry. Nvidia's aggressive move demonstrates its determination to capture a significant share of this lucrative market and maintain its position as the driving force behind the AI revolution.

Read the Full The Motley Fool Article at:

[ https://www.fool.com/investing/2026/03/21/massive-news-nvidia-just-made-a-2-billion-bet-on-n/ ]

[ Last Thursday ]: The Motley Fool

[ Last Thursday ]: The Motley Fool

[ Last Monday ]: The Motley Fool

[ Thu, Mar 05th ]: The Motley Fool

[ Thu, Mar 05th ]: The Motley Fool

[ Fri, Feb 20th ]: The Motley Fool

[ Sat, Feb 14th ]: The Motley Fool

[ Tue, Feb 10th ]: The Motley Fool

[ Fri, Feb 06th ]: The Motley Fool

[ Tue, Feb 03rd ]: The Motley Fool

[ Thu, Jan 29th ]: Seeking Alpha

[ Thu, Jan 15th ]: The Motley Fool