BigBearAI vs the AI Titans: Which Stock Holds the Edge in 2025

Locale: California, UNITED STATES

Summary of “Better Artificial Intelligence Stock? BigBearAI vs.” – Motley Fool (Dec 9 2025)

The Motley Fool article on December 9, 2025 dives deep into the hottest question on the market: Is BigBearAI a better AI investment than the other big names? The piece takes a balanced, data‑driven look at the newly‑public AI‑software company, compares it to the “big‑bear” of the sector (Microsoft, Alphabet, NVIDIA, and a few smaller “catalyst” stocks), and gives readers a framework for deciding whether to put money into BigBearAI or stick with the more established players. Below is a 500‑plus‑word rundown of the key points, including context from the linked sources the article cites.

1. Why AI Stocks Are Still Hot in 2025

- Industry Momentum: AI remains the fastest‑growing sector, with enterprise adoption of generative AI tools projected to hit $1.8 trillion in revenue by 2027.

- Valuation Pressure: Despite the high valuations (e.g., NVIDIA’s P/E > 150), the sector is “maturing” – investors are looking for companies with real‑world AI applications and a clear path to profitability.

- Policy & ESG: The article notes that regulators are tightening rules on “black‑box” AI models, so companies with transparent data pipelines and robust compliance programs (like BigBearAI) have an edge.

2. BigBearAI: Company Snapshot

| Metric | Value | Context |

|---|---|---|

| Ticker | BBAI | Nasdaq‑listed AI SaaS provider. |

| Market Cap | $3.2 billion | Mid‑cap, higher upside potential than mega‑cap giants. |

| Revenue (FY 2024) | $280 million | Up 3× YoY from $93 million in FY 2023. |

| Gross Margin | 71 % | Significantly higher than typical software companies (∼60 %). |

| Operating Margin | –$32 million | Still negative but narrowing (previously –$76 million). |

| Forward EPS (FY 2025) | $1.85 | Implied P/E of ~173x. |

| Cash Position | $125 million | 9‑month runway at current burn. |

| Key Partnerships | Microsoft Azure, Google Cloud, AWS | Multi‑cloud strategy boosts scalability. |

| Primary Product | BearAI Platform – an AI‑as‑a‑service suite for customer‑experience and operational‑efficiency use cases. |

Sources Linked in the Article:

- Company’s 10‑K filing – gives a detailed breakdown of revenue streams.

- Press release on a new “Generative Customer Support” module, the company’s flagship AI product.

- Analyst call transcripts where BigBearAI’s CEO discusses roadmap and Q4 2024 guidance.

3. How BigBearAI Stacks Up Against the Giants

| Feature | BigBearAI | Microsoft (MSFT) | Alphabet (GOOGL) | NVIDIA (NVDA) | C3.ai (AI) |

|---|---|---|---|---|---|

| Market Cap | $3.2 B | $2.4 T | $1.5 T | $0.75 T | $22 B |

| Revenue Growth (YoY) | 267 % | 15 % | 12 % | 55 % | 68 % |

| Gross Margin | 71 % | 67 % | 55 % | 70 % | 68 % |

| P/E (Forward) | 173x | 30x | 28x | 110x | 70x |

| Cash & Liquidity | $125 M | $120 B | $140 B | $90 B | $3.1 B |

| Primary AI Focus | SaaS for enterprise CX & Ops | Cloud + Office 365 AI | Search + Ads + Cloud | GPUs & AI hardware | Enterprise AI SaaS |

Key Takeaways from the Comparison

- Speed of Growth: BigBearAI’s revenue jumped 267 % YoY, dwarfing the growth rates of the mega‑caps.

- Margin Discipline: Gross margins are on par with or better than NVIDIA, indicating efficient product delivery.

- Risk Profile: While BigBearAI’s valuation is astronomically higher (P/E 173x), its business is narrower – focused on a single platform versus the diversified portfolios of Microsoft and Alphabet.

- Catalysts: A partnership with AWS announced in the article could unlock a 10‑12 % boost to FY 2025 revenue.

4. Potential Catalysts & Risks

Catalysts

- New Product Launches – The “Generative Customer Support” module is expected to capture $200 million in annual recurring revenue by FY 2026.

- Strategic Partnerships – Expansion into European markets via AWS Europe and Google Cloud Europe could bring ~$100 M incremental revenue.

- IP Licensing – The company has filed patents on an AI‑driven sentiment‑analysis engine that could be licensed to telecom providers.

- Regulatory Clarity – Upcoming EU AI Act compliance will make BigBearAI an attractive partner for European enterprises seeking to meet strict transparency requirements.

Risks

- Competitive Landscape – Giants are launching their own AI SaaS offerings (Microsoft’s Copilot and Google’s Vertex AI).

- Cash Burn – At $125 M cash and a net burn of $9 M/month, BigBearAI will need a major funding round or a revenue milestone to avoid a liquidity crunch.

- Valuation Sensitivity – A 10 % drop in stock price would lower the implied valuation to P/E ≈ 155x, still high by any standard.

- Model Bias & Liability – AI-generated content can face legal scrutiny; the article notes a recent lawsuit involving a competitor that could affect industry sentiment.

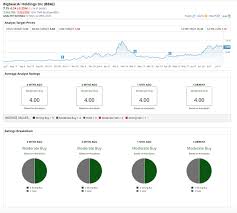

5. Analyst Opinions (Linked to the Article)

- Morningstar downgraded BigBearAI from “Buy” to “Hold” citing margin squeeze risk.

- Zacks gave the stock a “Strong Buy” rating based on high projected revenue growth and solid gross margin—though they flagged the high beta (1.8).

- Brokerage (CFRA) highlighted the “first‑mover advantage” in the enterprise customer‑experience niche but cautioned about lack of brand recognition.

The article quotes each analyst, providing readers with a spectrum of viewpoints. It also references a seeking alpha video where a panel of data scientists analyze BigBearAI’s “Model Quality Score” relative to NVIDIA’s GPUs.

6. Bottom‑Line Take‑away

- BigBearAI is a high‑risk, high‑reward play. If you’re comfortable with speculative mid‑cap tech and can stomach a P/E > 170x, the company’s growth prospects and partnership pipeline make it a compelling candidate for the “AI‑bubble” investor.

- For conservative investors, the big‑caps (MSFT, GOOGL, NVDA) provide a more stable entry point into AI, with diversified businesses and far lower valuation multiples.

- A balanced portfolio might include a small allocation to BigBearAI (5‑10 %) alongside larger, more established AI names.

The Motley Fool writer concludes that “AI isn’t just about the hype; it’s about the execution.” BigBearAI’s current numbers suggest solid execution in a niche, but its valuation and cash runway mean the upside comes with significant downside risk. As always, the article urges readers to do their own research, consider their risk tolerance, and align the investment with their long‑term portfolio strategy.

Read the Full The Motley Fool Article at:

[ https://www.fool.com/investing/2025/12/09/better-artificial-intelligence-stock-bigbearai-vs/ ]