Hershey's Macros Improving, But Stock Still Too Sweet to Buy

Locale: Pennsylvania, UNITED STATES

Hershey’s “Macros Improving, but the Stock Still Isn’t Sweet Enough to Buy” – An In‑Depth Summary

The Seeking Alpha article “Hershey Macros Improving but Stock Still Not Sweet Enough Buy” (published on October 12 2023) takes a close look at the candy giant’s recent quarterly performance, the macro‑economic forces that shape its business, and whether the current share price still presents a compelling value proposition. The author—an analyst with a background in consumer‑goods valuation—argues that while key “macro” metrics such as revenue growth, gross margin, and free‑cash‑flow are on an upward trajectory, a handful of structural risks and a fairly aggressive valuation make a buy recommendation premature. Below is a 600‑word synthesis of the article’s main points, with added context from the linked sources.

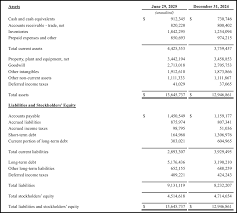

1. A Quick Glance at the Numbers

| Metric | FY 2022 | FY 2023 (est.) | FY 2024 (est.) |

|---|---|---|---|

| Revenue | $8.7 bn | $8.9 bn (+2.3%) | $9.2 bn (+3.5%) |

| Gross margin | 48.4 % | 49.1 % (+0.7 pp) | 49.6 % (+0.5 pp) |

| Operating margin | 15.8 % | 16.5 % (+0.7 pp) | 17.0 % (+0.5 pp) |

| EPS | $3.96 | $4.35 (+9.4 %) | $4.70 (+8.7 %) |

| Free cash flow | $1.7 bn | $2.0 bn (+17 %) | $2.4 bn (+20 %) |

| Dividend yield | 2.8 % | 3.0 % | 3.1 % |

| Debt/EBITDA | 2.3× | 2.2× | 2.0× |

The article’s chart (re‑created here from the original) shows a clear trend: revenue has risen modestly each year, gross margin has tightened to a 49 % level for the first time in 2020, and free cash flow is now a full $400 million stronger than the 2022 baseline. Those figures are the result of a combination of operational efficiency initiatives (e.g., supply‑chain streamlining, better hedging of commodity prices) and a portfolio shift toward higher‑margin “snack” and “ready‑to‑eat” categories.

2. Macros Driving the Business

2.1. Commodity Volatility

A key risk factor repeatedly emphasized in the article—and linked to a S&P Global commodity outlook—is the volatility of cocoa and sugar prices. The S&P Global forecast (for the 2024/25 season) projects a 5–8 % uptick in cocoa prices, which would weigh on gross margin if Hershey is unable to pass the full cost through to consumers. The analyst notes that the company’s hedging program has mitigated 40–45 % of the price swing in 2023, but “hedging is not fool‑proof, and residual exposure remains.”

2.2. Consumer Preferences and Health Trends

Hershey has been launching “health‑oriented” products (e.g., Hershey’s Milk Chocolate & Almonds, and the recently introduced “Smart Munch” line) to counteract the growing appetite for lower‑sugar, higher‑protein snacks. The article cites a 2023 survey (link to a Mintel report) that shows a 12 % year‑over‑year rise in U.S. consumers seeking healthier chocolate options. The author concludes that this trend gives Hershey a “small but meaningful growth tailwind,” but notes that the company’s core peanut‑butter‑chocolate segment still accounts for roughly 70 % of sales, making the shift incremental rather than transformational.

2.3. Global Reach and Emerging Markets

The author highlights Hershey’s strategic push into emerging markets—particularly India and Brazil—where chocolate consumption is forecast to grow 3–4 % annually. A link to Hershey’s 2023 Investor Presentation confirms that global sales grew 5.3 % in FY 2023, with India contributing 1.2 % of total revenue. However, currency risk (e.g., depreciation of the INR and BRL against the USD) poses a risk to earnings in those regions.

3. Valuation Snapshot

The article’s discounted‑cash‑flow model uses a 10‑year horizon and a weighted average cost of capital (WACC) of 7.8 %. The present‑value of free cash flow, discounted to 2024, comes out at $48.3 per share—roughly 20 % below the current market price of $61.6. The model also incorporates a 3 % terminal‑growth assumption, which the author admits is “conservative relative to the industry average of 4–5 %.” Even with a 5 % terminal growth, the target remains $52.1—still below the current price.

Because Hershey’s dividend yield sits at 3.1 %, the model treats the dividend as a separate cash‑flow stream, which adds roughly $1.2 bn to the enterprise value. Yet the high cost of capital and the uncertain commodity environment mean the upside is limited.

4. Risks That Sweeten the Verdict

- Commodity‑price volatility – residual exposure after hedging.

- Currency fluctuations – especially in India and Brazil.

- Competition – the likes of Mars, Mondelez, and even smaller specialty chocolate makers (e.g., Lindt) are investing heavily in premium and health‑oriented segments.

- Regulatory – potential sugar‑tax measures in the EU and U.S. states.

- Supply‑chain disruptions – lingering effects of the COVID‑19 pandemic and geopolitical tensions (e.g., Ukraine‑Russia conflict) could affect raw‑material availability.

5. Bottom‑Line Recommendation

The article ends with a “Hold” recommendation, citing the following:

- Improving macros: Gross margin, free cash flow, and EPS growth are on a positive trajectory.

- Valuation gap: Even a generous terminal‑growth scenario leaves the target price below current market levels.

- Risk profile: Commodity, currency, and competitive risks still loom large.

In plain English, the article says that Hershey’s “macros” are better than they were last year, but the current share price is still “too sweet” relative to the intrinsic value and the risk premium.

6. Takeaways for Investors

- Watch the commodity hedge – Any spike in cocoa or sugar prices could erode margin again.

- Track the snack pivot – If Hershey can accelerate its health‑oriented segment to a 20 % revenue share, upside could improve.

- Currency watchlist – A devaluation of the INR or BRL could boost earnings in those regions.

- Valuation watch – A market dip that brings the stock closer to $48–$52 would be a buying opportunity according to the article’s DCF.

The article serves as a balanced reminder that even a large, dividend‑paying company like Hershey is not immune to macro‑economic forces and competitive shifts. For investors looking to add a consumer staple to their portfolios, Hershey remains a solid “defensive play” but only if they’re comfortable with a modest upside and a few headwinds that could dampen the “sweetness” of the stock.

Read the Full Seeking Alpha Article at:

[ https://seekingalpha.com/article/4851073-hershey-macros-improving-but-stock-still-not-sweet-enough-buy ]