[ Mon, Nov 24th 2025 ]: Seeking Alpha

[ Mon, Nov 24th 2025 ]: The Motley Fool

[ Sun, Nov 23rd 2025 ]: Zee Business

[ Sun, Nov 23rd 2025 ]: Seeking Alpha

[ Sun, Nov 23rd 2025 ]: Entrepreneur

[ Sun, Nov 23rd 2025 ]: USA Today

[ Sun, Nov 23rd 2025 ]: The Globe and Mail

[ Sun, Nov 23rd 2025 ]: WSFA 12 News

[ Sun, Nov 23rd 2025 ]: Insider Monkey

[ Sun, Nov 23rd 2025 ]: Seeking Alpha

[ Sun, Nov 23rd 2025 ]: 24/7 Wall St

[ Sun, Nov 23rd 2025 ]: Seeking Alpha

[ Sun, Nov 23rd 2025 ]: The New Indian Express

[ Sun, Nov 23rd 2025 ]: The Financial Express

[ Sun, Nov 23rd 2025 ]: Seeking Alpha

[ Sun, Nov 23rd 2025 ]: CNBC

[ Sun, Nov 23rd 2025 ]: The Wall Street Journal

[ Sun, Nov 23rd 2025 ]: The New Zealand Herald

[ Sun, Nov 23rd 2025 ]: WTOP News

[ Sun, Nov 23rd 2025 ]: Kiplinger

[ Sun, Nov 23rd 2025 ]: Forbes

[ Sun, Nov 23rd 2025 ]: TheStreet

[ Sun, Nov 23rd 2025 ]: USA Today

[ Sun, Nov 23rd 2025 ]: The Motley Fool

[ Sun, Nov 23rd 2025 ]: The Motley Fool

[ Sun, Nov 23rd 2025 ]: Seeking Alpha

[ Sun, Nov 23rd 2025 ]: The Motley Fool

[ Sun, Nov 23rd 2025 ]: The Globe and Mail

[ Sun, Nov 23rd 2025 ]: The Motley Fool

[ Sun, Nov 23rd 2025 ]: The Motley Fool

[ Sat, Nov 22nd 2025 ]: This is Money

[ Sat, Nov 22nd 2025 ]: The West Australian

[ Sat, Nov 22nd 2025 ]: montanarightnow

[ Sat, Nov 22nd 2025 ]: Kiplinger

[ Sat, Nov 22nd 2025 ]: Barron's

[ Sat, Nov 22nd 2025 ]: Barron's

[ Sat, Nov 22nd 2025 ]: Insider

[ Sat, Nov 22nd 2025 ]: Seeking Alpha

[ Sat, Nov 22nd 2025 ]: Seeking Alpha

[ Sat, Nov 22nd 2025 ]: 24/7 Wall St

[ Sat, Nov 22nd 2025 ]: The Motley Fool

[ Sat, Nov 22nd 2025 ]: The Motley Fool

[ Sat, Nov 22nd 2025 ]: moneycontrol.com

[ Sat, Nov 22nd 2025 ]: The Motley Fool

[ Sat, Nov 22nd 2025 ]: Seeking Alpha

[ Sat, Nov 22nd 2025 ]: Seeking Alpha

[ Sat, Nov 22nd 2025 ]: The Motley Fool

[ Sat, Nov 22nd 2025 ]: Seeking Alpha

Michael Burry Takes Bold Short on Nvidia, Questioning AI Chip Giant's Valuation

TheStreet

TheStreetLocale: UNITED STATES

Michael Burry, the “Big Short” icon, takes a bold stance on Nvidia’s lofty valuation

An in‑depth look at the latest move by a contrarian investor who is betting against one of the most celebrated AI‑chip makers.

Who is Michael Burry?

Michael Burry rose to fame for his early recognition of the 2008 subprime mortgage crisis, a fact dramatized in The Big Short. The medical doctor‑turned‑investor has built a reputation for striking contrarian bets that often outperform the market—most notably his short position on American Airlines during the pandemic and his long bet on Tesla in the early 2010s. Burry’s public commentary is closely watched by traders, and his moves are typically taken seriously by the broader investment community.

The latest “fire shot” against Nvidia

In a recent press release from the private equity firm that manages Burry’s portfolio (as reported by MSN Money), the fund disclosed that it has entered into a short position on Nvidia’s stock. The move was described as a “fire shot” – a quick, high‑risk bet that the company’s valuation is unsustainable. The position is being executed via a series of put options, allowing the fund to profit from a decline in Nvidia’s share price without a full liquidation of the underlying equity.

The timing of this bet is notable. Nvidia has been riding a wave of strong demand for AI processors, its earnings have grown at double‑digit rates, and its market cap now exceeds $1 trillion. Burry’s decision to short the stock reflects his conviction that the current price no longer reflects realistic growth prospects, a viewpoint that challenges the prevailing narrative that AI‑driven technology will continue to outpace all other sectors.

Burry’s rationale – a mix of fundamentals and sentiment

Burry’s reasoning, as outlined in his public statement and subsequent interview, hinges on three key themes:

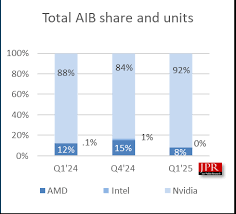

Valuation Multiples – Nvidia trades at a forward P/E of over 70 and a price‑to‑sales ratio of more than 25. Burry argues that these multiples are more in line with a speculative bubble than a sustainable business model. He compares Nvidia’s metrics with those of other semiconductor giants such as AMD and Intel, noting that even in an AI‑boosted environment, the traditional earnings framework remains the benchmark.

AI Growth Overestimation – While AI demand is real, Burry cautions that the hype has inflated expectations. He points to diminishing returns in the AI market: more firms entering the space, commoditization of chip production, and potential slowing of enterprise spend as the technology matures. In a recent comment on a finance forum, he suggested that “AI’s high‑growth narrative may be a short‑lived hype cycle rather than a long‑term paradigm shift.”

Competitive Dynamics – Nvidia faces increasing pressure from rivals. AMD’s recent GPU launches and Intel’s push into integrated GPU solutions erode Nvidia’s market share. The emergence of specialized AI accelerators from companies like Google’s TPU and AWS’s Inferentia chips could further fragment the market. Burry stresses that Nvidia’s cost structure and supply chain constraints could become bottlenecks in a highly competitive landscape.

Market reaction and implications

The short announcement caused a brief dip in Nvidia’s share price, as investors adjusted to the possibility of a downward correction. However, the reaction was muted compared to other high‑profile short positions, perhaps because many traders are already factoring a “soft landing” scenario into their pricing. Analysts noted that the short could be defensive rather than purely bearish; Burry’s team may also be hedging other long positions in the semiconductor space.

Investors who have followed Burry’s track record might now reassess their exposure to Nvidia. Some portfolio managers may consider a modest short or a protective put spread to guard against a potential price wobble, especially if the company reports weaker-than‑expected earnings or if macroeconomic data signals a tightening cycle that could dampen AI spend.

Contextual links and background

The MSN Money article also references several additional sources for deeper insight:

SEC filings – Burry’s short position was disclosed in a routine 13F filing, providing details on the option contracts and the size of the bet. These filings are useful for quantifying the exact exposure and potential upside/loss scenario.

Nvidia’s quarterly report – The company recently posted record revenue driven largely by its Data Center segment. Burry cites the company’s earnings forecast as a key point of contention, arguing that it may be overstated relative to industry fundamentals.

Historical performance of Burry’s portfolio – A linked profile of Burry’s investment firm showcases past bets, illustrating his pattern of betting against hot stocks while maintaining a diversified portfolio.

Commentary on AI market valuation – Several analyst reports caution that the AI sector may be experiencing a “price‑to‑earnings inflation” similar to what was seen in the late‑2000s tech boom. These reports provide a macro backdrop to Burry’s micro‑level thesis.

Bottom line

Michael Burry’s latest “fire shot” against Nvidia signals a growing skepticism among seasoned contrarians regarding the sustainability of the AI boom. While Nvidia remains a powerhouse in the semiconductor industry, Burry’s valuation concerns and competitive worries serve as a reminder that even the most celebrated growth companies are not immune to fundamental scrutiny. For investors, the bet underscores the importance of monitoring both company‑specific fundamentals and broader market sentiment when allocating capital to high‑growth, high‑valuation sectors.

Read the Full TheStreet Article at:

https://www.msn.com/en-us/money/other/big-short-michael-burry-fires-shots-at-nvidia-stock/ar-AA1QWO2G

[ Thu, Nov 20th 2025 ]: The Motley Fool

[ Tue, Nov 18th 2025 ]: The Motley Fool

[ Mon, Nov 17th 2025 ]: 24/7 Wall St

[ Mon, Nov 17th 2025 ]: Insider

[ Mon, Nov 17th 2025 ]: The Motley Fool

[ Mon, Nov 17th 2025 ]: Finbold | Finance in Bold

[ Mon, Nov 17th 2025 ]: 24/7 Wall St

[ Sun, Nov 16th 2025 ]: This is Money

[ Wed, Nov 12th 2025 ]: Seeking Alpha

[ Tue, Nov 11th 2025 ]: The Motley Fool

[ Wed, Nov 05th 2025 ]: Seeking Alpha