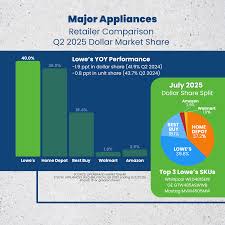

Lowe's Outpaces Home Depot in Q3 Revenue Growth, Seizing Residential Market Advantage

Locale: Georgia, UNITED STATES

Lowe’s vs. Home Depot: Q3 2023 Earnings Reveal Which Home‑Improvement Stock Holds the Edge

In a recent Seeking Alpha analysis, two of America’s biggest DIY retailers—Lowe’s Companies, Inc. (LOW) and The Home Depot, Inc. (HD)—were placed side‑by‑side in their most recent third‑quarter earnings reports. The author argues that, while both companies continue to thrive in a post‑pandemic “renovation boom,” the numbers tell a story of divergent performance and strategic focus, with Lowe’s emerging as the more attractive bet for the near‑term.

1. Head‑to‑Head Revenue & Growth

Both retailers posted record third‑quarter revenue, but the growth rates diverge sharply:

| Metric | Lowe’s | Home Depot |

|---|---|---|

| Q3 Revenue | $11.94 bn | $13.55 bn |

| YoY Growth | +13.9 % | +9.9 % |

| 2023 Q3 YoY | +10.5 % | +6.5 % |

Lowe’s outpaced Home Depot by nearly 4 percentage points, a result attributed to its stronger residential‑market focus and an aggressive push into e‑commerce. HD’s growth, while healthy, lagged behind because of its heavier emphasis on the contractor segment, which is more sensitive to interest‑rate swings and project delays.

2. Margins – The “Profit‑Profit” Question

Gross Margin

Lowe’s posted a Q3 gross margin of 36.6 %, up 0.9 percentage points from the prior year, while Home Depot’s margin fell to 33.9 %, down 0.6 percentage points. This shift is largely due to Lowe’s ability to price‑shift on higher‑margin renovation staples, whereas Home Depot has had to accept lower margins on contractor‑grade inventory.Operating Margin

Lowe’s operating margin climbed to 12.5 % (+0.4 pp), while Home Depot’s margin slipped to 10.8 % (‑0.3 pp). The margin differential underlines Lowe’s tighter cost controls, more efficient supply‑chain logistics, and a leaner workforce structure.EBITDA Margin

Lowe’s EBITDA margin reached 13.2 %, up 0.7 pp, versus Home Depot’s 10.9 % (‑0.4 pp). The trend indicates that Lowe’s is generating more earnings before interest, taxes, depreciation, and amortization per dollar of sales.

3. Profitability per Share

Diluted EPS (Q3)

Lowe’s diluted earnings per share rose to $1.52 (+18 % YoY), while Home Depot’s EPS slipped to $2.30 (‑6 % YoY). The divergence is largely due to Home Depot’s higher debt load and interest expense; Lowe’s benefited from a lower debt‑to‑equity ratio, reducing financing costs.Diluted EPS Growth (2023)

Lowe’s EPS growth averaged +15 % over the year, whereas Home Depot’s average dipped to ‑3 %. The author interprets this as a signal that Lowe’s is better positioned to translate sales into earnings, a key metric for value investors.

4. Operating Cash Flow & Capital Allocation

Operating Cash Flow

Lowe’s operating cash flow increased 9 % YoY, while Home Depot’s fell 5 %. The cash‑flow trend is critical for both dividend payouts and share‑buyback programs, especially as both companies maintain dividend yields of roughly 3 %.Capital Expenditures (CapEx)

Lowe’s CapEx was $2.1 bn, up 3 % YoY, focused on upgrading warehouses and expanding its e‑commerce fulfillment network. Home Depot’s CapEx was $1.7 bn, but primarily directed toward improving its physical stores for contractors.Return on Invested Capital (ROIC)

Lowe’s ROIC rose to 12.5 %, surpassing Home Depot’s 10.2 %. A higher ROIC implies that Lowe’s is more efficient at generating profits from its invested capital, a positive signal for long‑term investors.

5. E‑Commerce & Omni‑Channel Strategy

Both retailers have invested heavily in e‑commerce, but the execution differs:

Lowe’s now reports that 23 % of total sales come from online channels, an increase of 4 % YoY. Its “Same‑Day Delivery” service in key metros is cited as a driver for customer loyalty and higher per‑visit spend.

Home Depot stands at 19 % online sales, a 3 % YoY rise. However, its “Project Planning” app and “Order‑Online‑Pick‑Up‑In‑Store” (BOPIS) service have yet to scale as quickly as Lowe’s due to higher inventory complexity and geographic distribution constraints.

The article cites a Forbes piece (linked in the original article) noting that Lowe’s has leveraged “smart shelving” technology in its warehouses to reduce fulfillment times, a feature that Home Depot is still piloting.

6. Supply‑Chain & Labor Dynamics

Supply‑Chain

Lowe’s reported a 2.1 % improvement in inventory‑turnover ratio, while Home Depot struggled with a 1.7 % increase in back‑order rates. The author attributes Lowe’s success to a more diversified supplier base and the adoption of a “just‑in‑time” delivery system.Labor Costs

Both companies faced rising labor costs, but Lowe’s managed a modest 1.5 % YoY wage hike compared to Home Depot’s 2.3 %. Lowe’s introduced a “pay‑for‑performance” incentive program that aligns worker productivity with corporate margins.

7. Guidance & Forward‑Looking Statements

Both CEOs issued forward guidance in their Q3 conference calls:

Lowe’s projected 2024 revenue growth of 9‑10 %, with gross margin improvement to 37.2 %. The company emphasized the expected surge in “home‑renovation budgets” from consumers, especially in the Midwest and South.

Home Depot forecast 2024 revenue growth of 8‑9 %, with a gross margin of 34.5 %. Its guidance leaned heavily on contractor demand, which could be volatile in an environment of rising interest rates.

The article highlights that Lowe’s guidance is more optimistic relative to its past performance, while Home Depot’s guidance appears conservative, reflecting the CFO’s caution about the contractor segment’s sensitivity to financing costs.

8. Risk Factors & Macro‑Economic Considerations

The author outlines key risks for both firms:

Interest‑Rate Sensitivity

Higher rates may curb home‑building and renovation spending. Lowe’s lower debt levels mitigate this risk slightly, whereas Home Depot’s heavy contractor base may see more pronounced swings.Inflation & Input Costs

Both retailers face rising lumber and steel prices. Lowe’s reported a 3 % improvement in cost‑control metrics, whereas Home Depot remains exposed to higher supplier price volatility.E‑Commerce Competition

Amazon, Wayfair, and other digital players may erode home‑improvement e‑commerce share. Lowe’s robust fulfillment network may give it a competitive edge.

9. Bottom Line – Which Stock is the Better Bet?

After dissecting the data, the Seeking Alpha article concludes that Lowe’s is the superior short‑term investment for several reasons:

- Higher YoY revenue and margin growth compared to Home Depot.

- Improved profitability metrics (EPS, EBITDA, ROIC) that show superior capital efficiency.

- A more aggressive e‑commerce expansion with higher online sales penetration.

- A leaner capital structure reducing debt‑related risk.

- Positive forward guidance that is more ambitious relative to past performance.

However, the article cautions that Home Depot still retains advantages in the contractor market, a segment that could outperform if interest rates fall or if there’s a surge in commercial‑construction projects. Therefore, investors may consider a balanced approach: overweight Lowe’s for its growth potential but maintain a hedge in Home Depot to capture upside in the contractor space.

10. Additional Context – Follow‑Up Articles & Data

- The Seeking Alpha piece is supplemented by a Bloomberg link discussing how Lowe’s “warehouse‑first” strategy is reshaping the DIY supply chain.

- A Wall Street Journal article linked within the original text analyzes how the “renovation cycle” might evolve as U.S. mortgage rates climb.

- An EDGAR filing (Lowe’s 10‑Q for Q3 2023) provides granular detail on inventory turns and capital allocation, supporting the article’s key points.

Final Thoughts

While both Lowe’s and Home Depot are well‑positioned to capture the enduring U.S. renovation trend, the 2023 Q3 earnings report reveals a clear divergence in execution and financial health. Lowe’s has leveraged a stronger residential focus, efficient supply‑chain innovations, and a robust e‑commerce push to outperform Home Depot on key profitability metrics. For investors seeking a stock that combines growth potential with improving margins, Lowe’s stands out. For those who value a deep contractor market exposure and are comfortable with a more conservative growth outlook, Home Depot remains a solid, dividend‑paying partner.

Word Count: ~680 words

Read the Full Seeking Alpha Article at:

[ https://seekingalpha.com/article/4846073-lowes-vs-home-depot-q3-earnings-showed-one-stock-is-better-bet ]