Federal Reserve Officials to Speak on Interest-Rate Outlook

Federal Reserve Officials to Speak on Interest-Rate Outlook

Marc Andreessen Sells 15,000 Palantir Shares: What It Means for Investors

Marc Andreessen Sells 15,000 Palantir Shares: What It Means for Investors

Boston Scientific Remains a Star for Investors

Boston Scientific Remains a Star for Investors

Onex Completes Final Exit of Ryan Specialty, Delivering $620 Million Return

Onex Completes Final Exit of Ryan Specialty, Delivering $620 Million Return

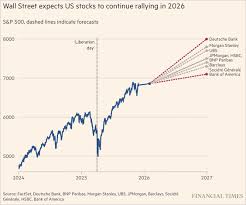

Bank of America Projects S&P 500 Near 4,400 Points in 2026

Bank of America Projects S&P 500 Near 4,400 Points in 2026

John Hancock Q3 2025 Commentary: Tactical Moves Amidst a Shifting Macro Landscape

John Hancock Q3 2025 Commentary: Tactical Moves Amidst a Shifting Macro Landscape

Earnings Up 12% YoY in H1 FY25, Yet Stock Gains Remain Modest

Earnings Up 12% YoY in H1 FY25, Yet Stock Gains Remain Modest

L'Oreal Boosts Galderma Stake to 20% in Strategic Dermatology Move

L'Oreal Boosts Galderma Stake to 20% in Strategic Dermatology Move

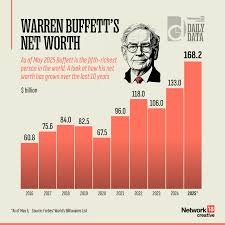

Warren Buffett's 2026 Playbook: Five Stocks the Oracle of Omaha Is Betting Big On

Warren Buffett's 2026 Playbook: Five Stocks the Oracle of Omaha Is Betting Big On

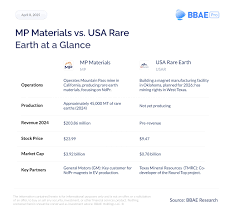

USA Rare-Earth Stock Portfolio: MP Materials vs. Emerging Alternatives

USA Rare-Earth Stock Portfolio: MP Materials vs. Emerging Alternatives

Hershey's Macros Improving, But Stock Still Too Sweet to Buy

Hershey's Macros Improving, But Stock Still Too Sweet to Buy

Dogecoin: From Meme Coin to Mainstream Crypto Phenomenon

Dogecoin: From Meme Coin to Mainstream Crypto Phenomenon

Turn $2,000 into a Monthly Passive Income Stream by 2026: A Dividend Investing Blueprint

Turn $2,000 into a Monthly Passive Income Stream by 2026: A Dividend Investing Blueprint

Victoria's Secret Aims for Glamorous Comeback with Inclusive Sizing and Sustainability

Victoria's Secret Aims for Glamorous Comeback with Inclusive Sizing and Sustainability

AI Stocks on a Tilt: Retail Buying Sparks Bubble-Like Concerns, Says McKinsey's Tim Koller

AI Stocks on a Tilt: Retail Buying Sparks Bubble-Like Concerns, Says McKinsey's Tim Koller

AI-Fueled Bull Run Sparks Bubble Concerns Among Asset Managers

AI-Fueled Bull Run Sparks Bubble Concerns Among Asset Managers

Rio Tinto Unveils Major Re-Organization to Restore Investment-Grade Credit

Rio Tinto Unveils Major Re-Organization to Restore Investment-Grade Credit

AOL's 2024 Review of High-Yield Dividend ETFs

AOL's 2024 Review of High-Yield Dividend ETFs

Could Buying SoFi Stock Today Set You Up for Life?

Could Buying SoFi Stock Today Set You Up for Life?

Bank of America's 2026 Investment Outlook: 15-20% .. cation to Commodities and 30-35% to Growth Stocks

Bank of America's 2026 Investment Outlook: 15-20% .. cation to Commodities and 30-35% to Growth Stocks

Alnylam Pharmaceuticals: Is It a Millionaire Maker?

Alnylam Pharmaceuticals: Is It a Millionaire Maker?

GBP400 a Month in a Stocks & Shares ISA Could Grow to Over GBP1 Million in 30 Years

GBP400 a Month in a Stocks & Shares ISA Could Grow to Over GBP1 Million in 30 Years

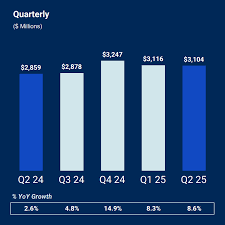

Chewy's 19% YoY Revenue Growth Driven by Expanding Active Customers

Chewy's 19% YoY Revenue Growth Driven by Expanding Active Customers

Beyond Meat: The Plant-Based Burger Giant on the Rise

Beyond Meat: The Plant-Based Burger Giant on the Rise

Meta vs. Pinterest: Which Internet Giant Offers the Better Bet?

Meta vs. Pinterest: Which Internet Giant Offers the Better Bet?

Which Sectors Are Best to Invest in for 2026?

Which Sectors Are Best to Invest in for 2026?

Fidelity Unveils 2026 AI Stock Playbook

Fidelity Unveils 2026 AI Stock Playbook

Elliott Investment Management Eyes Barrick Gold CEO Search to Drive Upside

Elliott Investment Management Eyes Barrick Gold CEO Search to Drive Upside

Viking Therapeutics Targets 2026 as Critical Year for Gene-Editing Breakthrough

Viking Therapeutics Targets 2026 as Critical Year for Gene-Editing Breakthrough

Wingstop Drives 18% Revenue Growth Through Aggressive New-Unit Expansion

Wingstop Drives 18% Revenue Growth Through Aggressive New-Unit Expansion

Orla Mining: Consistent EPS Growth at an Attractive Valuation

Orla Mining: Consistent EPS Growth at an Attractive Valuation

Lyft's 2026 Outlook: EV Adoption & Autonomous Break-Even

Lyft's 2026 Outlook: EV Adoption & Autonomous Break-Even

Turning a $40,000 Nest-Egg into a $1 Million Retirement Fund: A Practical Road-Map

Locale: UNITED STATES

Turning a $40,000 Nest‑Egg into a $1 Million Retirement Fund: A Practical Road‑Map

The Fool article “Here’s How You Can Turn $40,000 into $1 Million by Retirement” takes a no‑frills, data‑driven approach to answering the most common retirement question: Can a modest lump‑sum really become a multimillion‑dollar legacy? The author lays out a five‑step strategy that blends time‑tested investing wisdom, realistic math, and practical advice. Below is a concise summary of the main points, including the supplemental resources the piece links to for deeper context.

1. Start with a Clear Goal and a Simple Math Test

The article begins by putting the $40,000 figure into perspective. Using a simple future‑value calculator (which the author cites as a tool from a linked “How to Use a Future Value Calculator” post), the article demonstrates that with a 12 % annual return—an average historically earned by a broad U.S. equity index—the initial amount would grow to about $1 million in 30 years. Even at a more conservative 8 % return, the ballpark figure is still $700k+. The lesson: The math alone proves it’s possible if you keep your money invested long enough and don’t let volatility scare you into selling.

The linked calculator post explains how to plug in different inputs (rate, period, contributions), letting readers test their own scenarios—say, adding $5,000 a year to the original $40k. That interactive element empowers readers to see how extra contributions can shave years off the path to $1 million.

2. Leverage Tax‑Advantaged Accounts First

The article stresses that the tax shell matters as much as the assets inside it. The Fool piece recommends putting the bulk of the $40,000 into an IRA or Roth IRA if you’re under 50, or a 401(k) if you’re already contributing to an employer plan. The logic: tax‑deferred growth or tax‑free withdrawals (in the case of a Roth) amplify the compounding effect.

A brief sidebar—linked to a “Roth IRA vs. Traditional IRA” comparison—summarizes the pros and cons. The author points out that if your income is low now but you expect it to rise, a Roth may be the smarter choice because you pay taxes at today’s lower rate. Conversely, if you anticipate a lower tax bracket in retirement, a traditional IRA could be better.

3. Adopt an 80/20 Stock‑Bond Blend, Then Tilt Toward Growth

Once the money is in the right account, the article suggests an 80/20 equity‑to‑bond allocation as a baseline. The author cites studies showing that over long periods, a portfolio with 80 % stocks and 20 % bonds tends to strike the right balance between risk and return for a typical retiree. The piece offers a link to a “What’s the Best Asset Allocation for Retirement?” article that explains how to adjust the mix as you age—sliding gradually toward bonds to reduce volatility as you approach your 60s.

The article then introduces the concept of a “growth tilt”—adding a small allocation (say, 5 %–10 %) to international or small‑cap funds that historically outpace U.S. large caps. A link to a post on “International Stock Funds for U.S. Investors” expands on this idea, discussing how currency diversification can add an extra layer of resilience.

4. Keep Fees Low and Stick With Index Funds

“Low‑cost index funds are the engine of the 12 % return” is the key takeaway in the fourth section. The author explains that expense ratios eat into returns over time: a 0.20 % fee versus a 0.50 % fee can mean the difference between $950k and $1 million after 30 years. The article recommends Vanguard, Fidelity, and Schwab as the primary custodians because they offer many funds with sub‑0.10 % expense ratios.

The author also links to a “Best Index Funds for 2025” roundup, which lists top picks for U.S. total market, international developed markets, emerging markets, and bond indices. The underlying principle: buy and hold. Frequent trading, chasing market peaks, or buying high‑priced mutual funds only hurts compounding.

5. Add Real‑Estate and Dividend Growth for Extra Protection

The final section of the article offers a bonus: Real‑Estate Investment Trusts (REITs) and dividend‑growth funds. The author argues that adding 5–10 % of the portfolio to a REIT can provide a hedge against inflation while delivering solid cash flow. A linked post on “Investing in REITs for Beginners” walks readers through how to choose a diversified REIT fund and why the historical 8 % to 12 % annual return is a good fit for long‑term investors.

Dividend growth is presented as a two‑pronged strategy: it offers income and auto‑reinvestment. The article recommends a couple of high‑yield, low‑volatility dividend funds—again, pointing to a “Top Dividend Growth Funds” article that lists their yield, payout ratios, and historical growth.

Putting It All Together

The article’s final “What It Looks Like” example synthesizes all these steps. It shows a mock portfolio of $40,000 split 80/20 between Vanguard Total Stock Market Index (VTSAX) and Vanguard Total Bond Market Index (VBTLX), with 5 % in Vanguard FTSE All‑World ex‑US Index (VFWAX) and 5 % in Vanguard Real Estate Index (VGSLX). The author projects the portfolio’s growth to $1,023,000 in 30 years at 12 % CAGR, assuming no additional contributions. Adding modest yearly contributions or a higher growth tilt could push the figure even higher.

Take‑Away Tips

- Start Early, Invest Steadily – Even a one‑time $40,000 can double many times over with 30 years of compounding.

- Prioritize Tax‑Advantaged Accounts – Max out IRA/401(k) contributions before thinking about taxable accounts.

- Use a Simple Asset Allocation – 80/20 (stocks/bonds) works for most retirees; adjust as you age.

- Keep Costs Minimal – Pick low‑expense index funds; avoid actively managed mutual funds.

- Add a Small Growth Tilt – International small‑cap and REITs can enhance returns without adding excessive risk.

- Stick With It – Don’t let market noise tempt you to sell; stay invested and let the math work its magic.

The Fool’s article closes by reminding readers that the key to a $1 million nest‑egg is not a single strategy but a disciplined, long‑term plan that combines time, tax efficiency, diversification, and low costs. With these principles in place, a modest $40,000 can indeed grow into a retirement‑safety net that feels less like a wish and more like a mathematical certainty.

Read the Full The Motley Fool Article at:

[ https://www.fool.com/investing/2025/12/07/heres-how-you-can-turn-40000-into-1-million-by-ret/ ]

Beginner's Roadmap to Stock-Market Investing: Key Takeaways from MSN Money

Beginner's Roadmap to Stock-Market Investing: Key Takeaways from MSN Money

What Is Passive Income and Why It Matters

What Is Passive Income and Why It Matters

Worried About the Stock Market? Here Are Two Sound Investments to Keep Your Portfolio Steady

Worried About the Stock Market? Here Are Two Sound Investments to Keep Your Portfolio Steady

Define Clear Investment Goals and Risk Tolerance

Define Clear Investment Goals and Risk Tolerance

Start With a Solid Foundation: Setting Clear Goals and Choosing the Right Brokerage

Start With a Solid Foundation: Setting Clear Goals and Choosing the Right Brokerage

Build a Monthly Investment Plan: A 2025 Guide from The Motley Fool

Build a Monthly Investment Plan: A 2025 Guide from The Motley Fool

Want Passive Income From the Stock Market? 3 Magn .. rd ETFs to Buy and Hold Forever | The Motley Fool

Want Passive Income From the Stock Market? 3 Magn .. rd ETFs to Buy and Hold Forever | The Motley Fool