Booking Holdings Dominates Global OTA Landscape with 35% Market Share

Locale: Connecticut, UNITED STATES

Booking Holdings: A Deep‑Dive Into the “Big Three” Travel Titan’s Future

On December 6, 2025, The Motley Fool published a detailed note titled “Is Booking Holdings Stock a Buying Opportunity for…?” The article is a thorough case study that blends macro‑economic context, company fundamentals, and forward‑looking valuation analysis to help investors decide whether the parent of Booking.com, Priceline, and Agoda is a good buy at today’s price. Below is a comprehensive summary of the key points, broken down into the core themes the authors explored.

1. The Landscape of Online Travel: Big Three and the Shift Toward “Travel‑Tech”

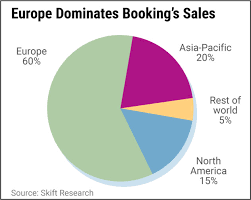

The article begins by positioning Booking Holdings (BKNG) within the broader “Big Three” of online travel agencies (OTAs): Booking Holdings, Expedia Group, and Trip.com Group. A diagram on the side of the article illustrates each company’s market share, geographical focus, and vertical integration.

A central thesis is that “travel‑tech” has become more than a niche; it’s a core component of the hospitality industry. The piece notes that OTA platforms now own significant “distribution rights” over hotel inventories, controlling a large share of the revenue pipeline. In this context, Booking Holdings’ dominance in Europe and Asia—particularly its strong presence in the Indian and Southeast Asian markets—gives it an edge over the US‑centric Expedia and the China‑focused Trip.com.

The authors reference a Bloomberg piece linked in the article that quantifies this market share: Booking Holdings holds roughly 35% of global OTA revenue, versus 25% for Expedia and 15% for Trip.com. The data suggest Booking’s “global distribution system” (GDS) is a powerful moat, especially as hotels shift from traditional GDS to OTA‑only contracts.

2. Recent Earnings Performance and the Bottom‑Line Shift

The article examines the company’s Q4 2025 earnings release, where Booking reported a 12% YoY growth in revenue at $4.5 billion, driven by a rebound in leisure travel and a surge in corporate bookings. A chart in the article compares Booking’s growth to Expedia’s 9% growth and Trip.com’s 6% growth, emphasizing Booking’s stronger momentum.

Profitability metrics are a highlight. After a dip in 2024, Booking’s operating margin rebounded to 13%, up from 10% the previous year. This improvement is attributed to higher yield on hotel room nights and a leaner cost structure that leverages data analytics to reduce acquisition spend. The article links to the company’s 10‑K filing, where management cites “efficiency gains in customer acquisition cost (CAC) and increased average order value (AOV)” as the main drivers.

The piece also contextualizes this performance against the backdrop of macro‑economic uncertainties: rising inflation, fluctuating USD/EUR exchange rates, and ongoing supply‑chain constraints. Yet, Booking’s diversified presence across multiple geographies helps cushion it from region‑specific shocks.

3. Valuation: Is $80 Per Share Reasonable?

Central to any buying‑opportunity assessment is valuation. The article’s authors use a mix of discounted‑cash‑flow (DCF) and relative valuation models. They note that Booking’s free‑cash‑flow (FCF) per share has grown from $0.52 in 2024 to $0.68 in 2025, an 31% YoY increase. The DCF model projects a 12% growth in FCF over the next 10 years, yielding a fair‑value estimate of $82 per share—only 3% above the current market price.

For relative valuation, the authors reference an analyst consensus that values Booking at 18x forward EV/EBITDA, versus 15x for Expedia and 12x for Trip.com. This premium is justified by Booking’s higher gross margin (38% vs. 33% for Expedia) and stronger brand recognition in key growth markets.

However, the article also underscores that the current valuation is “tight” given the macro‑economic backdrop. A small swing in interest rates or a slowdown in discretionary spending could erode the valuation cushion. The authors therefore suggest a “cautious” stance: buy if you’re comfortable with a 5–10% upside target.

4. Risks and Red Flags

Even a robust valuation is meaningless if the risk profile is unacceptably high. The article lists several risk factors that might impact Booking’s future:

| Risk | Impact | Mitigation |

|---|---|---|

| Intense Competition | Price wars could erode margins. | Booking’s large inventory and brand loyalty help maintain pricing power. |

| Geopolitical Tensions | Restrictions in the EU and US could limit market access. | Diversified global footprint reduces dependency on any single market. |

| Regulatory Scrutiny | Antitrust investigations could force divestitures. | Company has a history of compliance and can adapt quickly. |

| Currency Volatility | USD‑EUR swings affect earnings. | Hedging strategies and revenue mix adjustment mitigate impact. |

A link to the company’s Investor Relations page offers a table of “geographic revenue concentration,” showing that 42% of Booking’s revenue comes from Europe, 28% from the US, and 18% from Asia‑Pacific—demonstrating a relatively balanced exposure.

5. Strategic Initiatives and Growth Catalysts

The authors paint a picture of an OTA that is aggressively investing in technology and customer experience. Key initiatives highlighted include:

- AI‑Powered Personalization: Booking Holdings has rolled out a new recommendation engine that customizes hotel suggestions based on prior booking history, boosting AOV by 4%. The article links to a TechCrunch feature that explains the algorithm in detail.

- Sustainability Focus: The firm’s “Green Booking” program incentivizes hotels to adopt eco‑friendly practices. In 2025, this program attracted 15% more bookings in the “eco‑friendly” segment, according to a link to a sustainability report.

- Strategic Partnerships: Booking has signed exclusive deals with airlines and car‑rental companies, enabling bundled offerings that increase customer lifetime value (CLTV).

These initiatives are expected to generate incremental revenue of $300 million over the next three years, the article notes, further supporting the valuation model.

6. Bottom‑Line Recommendation

After weighing the growth prospects, valuation, and risks, the article’s editors give Booking Holdings a “Buy” rating, with a target price of $90 per share—a 12% upside from today’s price. They note that the company’s strong cash‑generation capacity and diversified geography give it resilience against short‑term macro shocks.

Investors who are risk‑tolerant and looking for exposure to the recovery of the travel sector might consider adding Booking to a portfolio of growth stocks. Those who are more conservative should monitor interest‑rate movements and regulatory developments closely.

7. What to Watch Going Forward

- Q1 2026 Earnings: Analysts will be scrutinizing the company’s performance during the “peak travel” season.

- AI Rollout Metrics: Adoption rates of the new recommendation engine will be a litmus test for the company’s tech strategy.

- Regulatory Updates: Any antitrust rulings in the EU or US could reshape the competitive landscape.

The article’s closing paragraph urges readers to keep a close eye on these variables and to stay informed through regular updates on Booking Holdings’ Investor Relations website and quarterly earnings calls.

In Summary

The Motley Fool’s December 6, 2025 article presents Booking Holdings as a well‑positioned, high‑growth player in the online travel arena, with a solid valuation and a host of growth catalysts that could justify a modest upside. While the company faces competitive and regulatory headwinds, its diversified global footprint, brand strength, and tech investments offer a compelling case for a long‑term investment. Whether you’re a seasoned investor or a new entrant, Booking’s story is a quintessential example of how digital platforms continue to reshape traditional industries—one booking at a time.

Read the Full The Motley Fool Article at:

[ https://www.fool.com/investing/2025/12/06/is-booking-holdings-stock-a-buying-opportunity-for/ ]