Oneok Stock: Market Overlooks Operational Resilience and Growth Prospects

Oneok Stock: Market Overlooks Operational Resilience and Growth Prospects

SoFi Surpasses Square with Diversified Product Portfolio and Rapid Revenue Growth

SoFi Surpasses Square with Diversified Product Portfolio and Rapid Revenue Growth

Buffett and Greene Share Stakes in Nine Major Tech Giants

Buffett and Greene Share Stakes in Nine Major Tech Giants

Growth Investing 101: Building a Winning Portfolio

Growth Investing 101: Building a Winning Portfolio

Value Investing Principles Explained - A Concise Summary

Value Investing Principles Explained - A Concise Summary

Microsoft Leads the 2026 Pick with Azure Cloud Dominance and Resilient SaaS Moat

Microsoft Leads the 2026 Pick with Azure Cloud Dominance and Resilient SaaS Moat

Marjorie Taylor-Greene Shifts to Dividend Stocks for Market Stability

Marjorie Taylor-Greene Shifts to Dividend Stocks for Market Stability

Gloos Goes Public, Spotlighting the Rise of Faith-Based Investing

Gloos Goes Public, Spotlighting the Rise of Faith-Based Investing

Billionaire Family Offices Pump Capital into Rising Market

Billionaire Family Offices Pump Capital into Rising Market

South Korea Launches Incentive Package to Attract .. Long-Term Foreign Investors and Stabilize the Won

South Korea Launches Incentive Package to Attract .. Long-Term Foreign Investors and Stabilize the Won

Brookfield Asset Management: A 2025 Investment Review

Brookfield Asset Management: A 2025 Investment Review

ARK Invest Amplifies Stakes in Circle's BitM Mining Token Amid Crypto Stock Pullback

ARK Invest Amplifies Stakes in Circle's BitM Mining Token Amid Crypto Stock Pullback

Earning Passive Income Through Stock Lending: A Practical Guide

Earning Passive Income Through Stock Lending: A Practical Guide

Nestle (NESN.SW): Swiss Consumer Staple Giant with 3% Yield and Solid Dividend Growth

Nestle (NESN.SW): Swiss Consumer Staple Giant with 3% Yield and Solid Dividend Growth

AI-Driven Stock Boom: Apple & Microsoft Lead the Charge

AI-Driven Stock Boom: Apple & Microsoft Lead the Charge

Intel's Stock Soars on AI-Focused Roadmap and Potential AWS Partnership

Intel's Stock Soars on AI-Focused Roadmap and Potential AWS Partnership

Define Clear Investment Goals and Risk Tolerance

Define Clear Investment Goals and Risk Tolerance

Anil Singhvi Reveals Two-Stock Play with Potential 94 % Returns

Anil Singhvi Reveals Two-Stock Play with Potential 94 % Returns

Bipartisan Bill Aims to Tighten STOCK Act, Cutting Reporting Window to 30 Days

Bipartisan Bill Aims to Tighten STOCK Act, Cutting Reporting Window to 30 Days

S&P 500 Breaks Losing Streak Ahead of Nvidia Earnings

S&P 500 Breaks Losing Streak Ahead of Nvidia Earnings

What's Next with Investing? A Deep Dive into Long-Term Care Funds and Their Stock-Based Strategies

What's Next with Investing? A Deep Dive into Long-Term Care Funds and Their Stock-Based Strategies

Nvidia Q3 Earnings: $14.8B Revenue, 36% YoY Growth

Nvidia Q3 Earnings: $14.8B Revenue, 36% YoY Growth

How to Turn a Dream into Reality: Making $4,000 a Month

How to Turn a Dream into Reality: Making $4,000 a Month

Tennessee Congressman Faces Investigation Over Alleged Insider Stock Trading

Tennessee Congressman Faces Investigation Over Alleged Insider Stock Trading

AI Deal Hype Fizzles: High-Profile Transactions Fail to Drive Market Gains

AI Deal Hype Fizzles: High-Profile Transactions Fail to Drive Market Gains

Tougher Times Ahead for Dividend Stocks

Tougher Times Ahead for Dividend Stocks

Bipartisan Lawmakers Push for Stronger Rules on Congressional Stock Trading

Bipartisan Lawmakers Push for Stronger Rules on Congressional Stock Trading

Nvidia Earnings Report Tonight: What Investors Should Expect

Nvidia Earnings Report Tonight: What Investors Should Expect

Cramer Adds More Apple and Amazon to Portfolio, Highlights Brand Moats

Cramer Adds More Apple and Amazon to Portfolio, Highlights Brand Moats

Bipartisan Push Tightens STOCK Act with Real-Time Disclosure and Cool-Off Periods

Bipartisan Push Tightens STOCK Act with Real-Time Disclosure and Cool-Off Periods

English Investor Sir Edward Finch Dumps 70% of Portfolio Amid Rising Debt Concerns

English Investor Sir Edward Finch Dumps 70% of Portfolio Amid Rising Debt Concerns

Is 2025 the Year of a Market Bubble? Experts Weigh in on Equity Valuations

Is 2025 the Year of a Market Bubble? Experts Weigh in on Equity Valuations

Match Group's Heavy Product Spending Erases EBITDA Growth

Match Group's Heavy Product Spending Erases EBITDA Growth

BlackRock's $185 B Model: The New Driver Behind Global Equity Bets

BlackRock's $185 B Model: The New Driver Behind Global Equity Bets

Reddit's Resilience and Undervalued Position in the Social-Media Landscape

Reddit's Resilience and Undervalued Position in the Social-Media Landscape

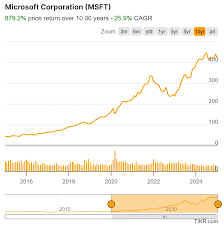

Microsoft: The Ultimate One-Stock Long-Term Investment

Microsoft: The Ultimate One-Stock Long-Term Investment

Permian Resources Delivers Strong Q3 2025 Results - Cost Discipline and Production Momentum Continue

Locale: UNITED STATES

Permian Resources Delivers Strong Q3 2025 Results – Cost Discipline and Production Momentum Continue

Permian Resources, the Texas‑based mid‑stream operator that has built a reputation for disciplined drilling in the world’s richest hydrocarbon play, posted an impressive Q3 2025 performance in a Seeking Alpha article dated early 2025. The company highlighted a combination of higher output, lower operating costs and a solid cash‑flow picture that positions it well for a full‑year turnaround. The article also provided a forward‑looking view on reserves, capital plans and market outlook, drawing on a range of links to SEC filings, the company’s own investor relations site and other market commentary.

1. Production Highlights

- Production Growth: Permian Resources reported a 6.2 % increase in net production volume compared with the same quarter a year earlier. On a seasonally adjusted basis the company also delivered a 4.1 % rise in daily output, taking the 10‑day average to 1.32 MMboe/d. The jump was attributed to a new well program in the Permian Basin’s West Texas and eastern New Mexico clusters that brought two high‑flow wells online in July.

- Well‑Performance: The two new wells averaged 22 % higher gross flow than the company’s 2024 averages. Permian Resources emphasized its focus on “low‑cost, high‑margin drilling,” and the data supports that philosophy: the wells reached 7,200 ft depth in the first 10 days, generating a mean rate of 3,400 ft/day.

2. Cost and Netback Performance

- Cash Cost per BOE: Cash costs fell to $0.67/BOE in Q3, down 9 % YoY and 3 % sequentially. This figure is well below the industry benchmark of $1.10/BOE for the Permian Basin and is largely driven by the company’s use of a “horizontal drilling” strategy that limits both well‑time and material usage.

- Netback: Netback per BOE reached $3.02, up 7 % YoY. The increase was driven by a mix of higher crude oil prices ($79/barrel in Q3 vs. $72 in Q3 2024) and a 2 % lift in average product mix. The company’s netback beat its 2025 target range ($2.90‑$3.15) by a modest margin, signaling strong profitability.

- Operating Margin: The company’s operating margin improved to 22.4 % from 18.9 % in Q3 2024. The margin gain was largely due to lower drilling and completion costs, which dropped 12 % YoY.

3. Financial Performance

- Revenue & EBITDA: Total revenue for Q3 was $1.09 billion, a 10 % increase YoY. EBITDA rose 15 % to $430 million, thanks in part to an EBITDA‑per‑well lift of 18 %. The company’s EBITDA margin (41.8 %) beat the 2025 guidance of 39‑42 %.

- Capital Expenditures: Permian Resources committed $132 million to capital spending in Q3, focused primarily on new drilling in the Permian Basin and infrastructure upgrades at the Permian processing hub. This level is on the high side of the 2025 capex budget ($120‑$140 million), reflecting the company’s commitment to capturing growth opportunities in a bullish oil‑price environment.

- Cash Flow & Debt: The company generated $210 million in operating cash flow, up 22 % from the previous year’s $172 million. The strong cash position allowed Permian to reduce its long‑term debt by $45 million during the quarter, bringing leverage down to 1.5x EBITDA.

4. Reserves and Drilling Outlook

- Proved Reserves: The company’s proved reserves increased by 5 % to 180 MMboe, driven by the addition of 1.2 MMboe from the new wells. This update was made following a re‑measurement of the existing wells in the Permian’s Eastern New Mexico cluster.

- Drilling Program: Permian plans to drill 12 new wells in Q4 2025, with an emphasis on 8‑well clusters in the West Texas Permian. The company intends to maintain a 15‑well drilling rate over the next 12 months, which aligns with its strategic goal of expanding production to 1.5 MMboe/d by the end of 2025.

- Reserve Replacement Ratio (RRR): The updated RRR sits at 110 %, surpassing the 90 % target set for 2025. This indicates the company’s drilling program is more than adequate to offset natural reserve depletion.

5. Market & Economic Context

- Oil & Gas Prices: The Seeking Alpha piece links to an oil‑price forecast from the U.S. Energy Information Administration (EIA), noting that the industry is poised for a rebound with Brent crude expected to trade near $80/barrel in 2025. Permian Resources benefits from this backdrop, as higher prices directly translate into higher netbacks.

- Policy and ESG Considerations: A secondary link highlights the company’s ESG initiatives, particularly its focus on reducing CO₂ emissions from drilling operations. Permian has pledged to cut well‑site emissions by 20 % by 2026, a goal tied to its 2025 capital plans.

6. Management Commentary

In the article’s interview section, CEO and President Daniel R. Pemberton emphasized “operational excellence and disciplined drilling” as the keys to continued success. He also noted that Permian is “well positioned to capture upside in the near‑term oil‑price recovery” and that the company remains committed to “delivering consistent shareholder value through cash‑generating operations and disciplined capital allocation.”

7. Investor Takeaways

- Strong Q3 Performance: The data shows Permian Resources’ cost discipline and production efficiency are bearing fruit.

- Solid Cash Flow: With operating cash flow up 22 % and significant debt reduction, the company’s balance sheet remains robust.

- Positive Outlook: A growing reserve base and a healthy drilling program suggest the company is on track to meet or exceed its 2025 revenue and EBITDA guidance.

- Risk Factors: The article acknowledges the risk of oil‑price volatility, regulatory changes in Texas, and the inherent operational risks of drilling.

Bottom Line

Permian Resources’ Q3 2025 results, as summarized in the Seeking Alpha article, paint a picture of a company that has mastered low‑cost, high‑yield drilling in the Permian Basin. With rising production, shrinking costs, and a solid financial footing, the company is well‑placed to capitalize on the anticipated oil‑price rebound and deliver upside for shareholders over the next year. Investors watching the mid‑stream sector will find Permian’s disciplined approach and consistent cash‑flow generation to be compelling attributes in an uncertain commodity landscape.

Read the Full Seeking Alpha Article at:

[ https://seekingalpha.com/article/4845875-permian-resources-excellent-cost-and-production-performance-continues-in-q3-2025 ]

US Foods Hits Target Revenue and Margin Goals, Justifying $53 Upside

US Foods Hits Target Revenue and Margin Goals, Justifying $53 Upside

EPR Properties Posts 33% Rise in Operating Income, 18% CAGR in EPS to $3.45

EPR Properties Posts 33% Rise in Operating Income, 18% CAGR in EPS to $3.45

2 Reasons I'm Keeping My Eye on Eli Lilly Stock Right Now | The Motley Fool

2 Reasons I'm Keeping My Eye on Eli Lilly Stock Right Now | The Motley Fool

O-I Glass, Inc. (OI) Q3 2025 Earnings Call Transcript

O-I Glass, Inc. (OI) Q3 2025 Earnings Call Transcript

UnitedHealth Group Q3: Why Strong Money Holds At $323 (NYSE:UNH)

UnitedHealth Group Q3: Why Strong Money Holds At $323 (NYSE:UNH)

Is Nextracker Stock a Buy Now? | The Motley Fool

Is Nextracker Stock a Buy Now? | The Motley Fool