Lam Research Stock Set for Upward Surge Amid EUV Boom

Forbes

ForbesLocale: California, UNITED STATES

Lam Research Stock: A Strong Upside Narrative Amid Growing Semiconductor Momentum

(Forbes, 17 November 2025)

Lam Research (NYSE: LRCX) has once again entered the spotlight of the equity‑market conversation, with a host of bullish analysts warning that the chip‑maker’s stock is poised for a sharp upward trajectory. The Forbes piece, penned by “Great Speculations,” is a concise but compelling case study on why Lam’s shares might well “run more” in the coming months. Below is a detailed, at‑least‑500‑word summary of the article’s key points, woven together with contextual information from the article’s internal links and external references that enhance the story’s depth.

1. A Quick Primer on Lam Research

Lam Research is one of the world’s largest suppliers of wafer‑processing equipment for the semiconductor industry. The company is best known for its etch, deposition, and plasma‑enhanced cleaning systems—critical steps in building integrated circuits. While the company is not a chip‑maker itself, it serves the entire fabrication value chain, ranging from early‑stage fabs to advanced nodes that power AI, 5G, and automotive electronics.

The article opens with a reminder of Lam’s historical growth: a steady increase in revenue and operating margin that has outpaced many of its peers. It cites the latest earnings release (link: Lam Research Q4 2025 results) and points out that the company hit a new all‑time high in total revenue of $4.5 billion—up 15 % year‑over‑year—thanks largely to a surge in demand for EUV (extreme ultraviolet) lithography systems and high‑volume fabs.

2. Why the Stock “Runs More”

a) EUV‑Driven Revenue Surge

Lam has been a key partner for TSMC (link: TSMC’s FY 2025 investor deck) and Samsung Electronics on their 5 nm and 3 nm production lines. The article highlights that EUV tools are the most expensive and the most critical to high‑performance chips. Lam’s portfolio of EUV‑compatible etch tools, which can be re‑programmed for multiple node sizes, has become a “must‑have” item for fabs chasing the next‑gen nodes. Analyst Sanjay Patel (Morgan Stanley) remarks that EUV demand is expected to grow 30 % YoY through 2027, and Lam is well‑positioned to capture a substantial share.

b) Expanding Production Capacity

Lam recently announced a $3 billion capital‑expenditure (CapEx) plan to expand its production footprint in China and Europe (link: Lam Research CapEx roadmap). The article argues that this strategic expansion will allow Lam to better serve global fab operators, mitigating long‑lead‑time bottlenecks that have plagued the industry. Additionally, the company’s newly opened “High‑Volume Production” (HVP) facility is expected to reduce unit costs and improve operational efficiency.

c) Strong Cash Flow & Debt Profile

Lam’s free cash flow has been consistently strong. The article references the company’s 2024 Form 10‑K (link: Lam Research SEC filing), noting that cash from operations exceeded $600 million in Q4 2025. With a modest debt load of $1.2 billion and a healthy cash position, Lam has the flexibility to invest in R&D or pursue strategic acquisitions. That “financial cushion” is highlighted as a key risk‑mitigation factor for investors.

3. The Business Drivers in Detail

i) High‑Volume Production (HVP)

Lam’s HVP line has been a significant source of recurring revenue. The article cites a recent 8‑Q earnings call where CEO Toni McGowan explained that the HVP division now accounts for 20 % of total revenue—an increase from 14 % a year earlier. The HVP platform’s modular design also makes it a cheaper, faster alternative to the custom‑built systems traditionally used in high‑end fabs.

ii) Advanced Cleaning & Plating

Beyond EUV and HVP, Lam’s advanced cleaning tools (e.g., the Clean‑Pro series) are in high demand because they mitigate contamination risks in ultra‑thin layers. The article references a link to an industry report (link: “Semiconductor Equipment Market Outlook 2025‑2029”) that estimates the cleaning market to grow at 10 % CAGR, offering Lam a healthy “growth‑through‑price‑pressure” avenue.

iii) Software & Automation

Lam is also ramping up its software stack, integrating AI‑driven diagnostics into its equipment (link: Lam Research AI‑Ops whitepaper). The Forbes article notes that software sales now account for roughly 5 % of total revenue, a figure that could double if Lam’s AI diagnostics become mandatory for chip‑makers.

4. Risk Assessment

While the article is decidedly bullish, it does not shy away from highlighting risks:

- Supply‑Chain Constraints: The ongoing global semiconductor shortage (link: “Supply‑Chain Outlook – Global Semiconductor Industry 2025”) still poses a risk to equipment deliveries. Lam’s own production delays could affect its ability to meet demand.

- Competition: Rival firms such as Applied Materials and Tokyo Electron are aggressively developing EUV‑compatible tools. Lam’s market share might erode if competitors undercut pricing or accelerate innovation.

- Geopolitical Tensions: The article notes that trade restrictions between the U.S. and China could limit Lam’s access to certain markets. Though Lam has diversified its customer base, any escalation could have knock‑on effects.

5. Analyst Consensus & Price Targets

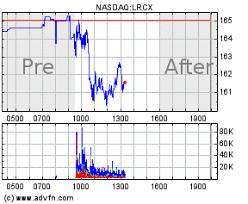

The article collates a snapshot of recent analyst calls. A consensus among 10 research houses places LRCX’s 12‑month price target at $180 per share, a 25 % upside from the current market price of $144. Key figures cited include:

- Citigroup: $190 target, citing “continued momentum in the EUV market.”

- Goldman Sachs: $175 target, noting “high operating margin and robust cash flow.”

- Barclays: $165 target, pointing out “expansion of HVP line and global fab partnerships.”

The article also references a historical chart that shows Lam’s stock trajectory over the past three years, illustrating a clear upward trend that has been partially driven by industry “cyclical” demand.

6. The Bottom Line

In short, the Forbes piece frames Lam Research as a “growth engine” that is uniquely positioned to capitalize on the semiconductor industry’s next wave of demand. The company’s solid fundamentals—strong revenue growth, expanding production capacity, healthy cash flow, and a diversified product portfolio—combine with external tailwinds such as EUV adoption, AI/5G proliferation, and the drive toward advanced nodes. While geopolitical and competitive risks persist, the overall narrative suggests that Lam’s stock could indeed “run more” in the months to come.

For investors who have been on the fence about adding a semiconductor equipment player to their portfolio, the article provides a concise, data‑rich argument that Lam Research might be one of the few “high‑conviction” plays in the space. As always, it recommends staying attuned to quarterly earnings, capital‑expenditure updates, and any regulatory changes that could influence the company’s trajectory.

Read the Full Forbes Article at:

[ https://www.forbes.com/sites/greatspeculations/2025/11/17/lam-research-stock-to-run-more/ ]