SpaceX IPO Could Turn Google into a $111 Billion Winner

SpaceX IPO Could Turn Google into a $111 Billion Winner

Millionaire YouTuber Hank Green Shares Gen-Z Inve .. rint: Discipline, Diversification, and AI Caution

Millionaire YouTuber Hank Green Shares Gen-Z Inve .. rint: Discipline, Diversification, and AI Caution

Federal Reserve Moves and Their Ripple Effect on Stocks, Crypto, and All Asset Classes

Federal Reserve Moves and Their Ripple Effect on Stocks, Crypto, and All Asset Classes

UK Treasury Proposes 20% Tax on Idle Cash in ISAs

UK Treasury Proposes 20% Tax on Idle Cash in ISAs

Bank of America Unveils 'Top 6' Investing Ideas Amid Grim 60-40 Outlook

Bank of America Unveils 'Top 6' Investing Ideas Amid Grim 60-40 Outlook

Paramount Sells 20% Stake in International Distri .. tion to Warner-Discovery Amid Democratic Scrutiny

Paramount Sells 20% Stake in International Distri .. tion to Warner-Discovery Amid Democratic Scrutiny

PFRDA Expands Pension Fund Investment Options to .. Estate, Infrastructure, and Equity-Linked Assets

PFRDA Expands Pension Fund Investment Options to .. Estate, Infrastructure, and Equity-Linked Assets

Palantir vs. Nvidia: Who Will Dominate the AI Stock Landscape in 2026?

Palantir vs. Nvidia: Who Will Dominate the AI Stock Landscape in 2026?

The 60/40 Portfolio Is Outdated - Here's the Strategy That Actually Wins

The 60/40 Portfolio Is Outdated - Here's the Strategy That Actually Wins

Fed's Hawkish Tilt Threatens 10-Year Treasury 'Danger Zone' for Stocks

Fed's Hawkish Tilt Threatens 10-Year Treasury 'Danger Zone' for Stocks

Procter & Gamble: 30 Years of Dividend Growth at 4.0%-4.3% Yield

Procter & Gamble: 30 Years of Dividend Growth at 4.0%-4.3% Yield

Why ETFs are a Smart Choice for New Investors

Why ETFs are a Smart Choice for New Investors

High-Yield Dividend ETFs: Five Picks Paying Over 5 % (2025 - December 10)

High-Yield Dividend ETFs: Five Picks Paying Over 5 % (2025 - December 10)

Market Panic Is a Short-Term Reaction, Not a Long-Term Warning

Market Panic Is a Short-Term Reaction, Not a Long-Term Warning

Mid-Cap and Small-Cap Stocks in a Correction: Wha .. the Numbers Tell Us About HDFC Securities Shares

Mid-Cap and Small-Cap Stocks in a Correction: Wha .. the Numbers Tell Us About HDFC Securities Shares

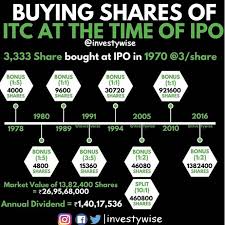

ITC Stocks: A Diversified, Dividend-Rich Anchor for Long-Term Portfolios

ITC Stocks: A Diversified, Dividend-Rich Anchor for Long-Term Portfolios

PSU Banks Beat Private Counterparts on Profitability and Returns

PSU Banks Beat Private Counterparts on Profitability and Returns

Low-Volatility Funds Rise Amid Market Turbulence

Low-Volatility Funds Rise Amid Market Turbulence

Johnson & Johnson and Procter & Gamble: The Top Dividend Aristocrats for a 10-Year Hold

Johnson & Johnson and Procter & Gamble: The Top Dividend Aristocrats for a 10-Year Hold

Civitas Resources Boosts Outlook with $2.6B Merger with SM Energy

Civitas Resources Boosts Outlook with $2.6B Merger with SM Energy

Warren Buffett's 184-Billion Dollar Warning: What the 2025 Article Tells Investors About 2026

Warren Buffett's 184-Billion Dollar Warning: What the 2025 Article Tells Investors About 2026

Turning a Modest Inheritance into a Long-Term Asset

Turning a Modest Inheritance into a Long-Term Asset

BOE Boosts Tax-Efficient Income with Global Equity Rating Upgrade

BOE Boosts Tax-Efficient Income with Global Equity Rating Upgrade

Metal Stocks Surge on Fed-Rate Cut Hopes and Booming Silver Market

Metal Stocks Surge on Fed-Rate Cut Hopes and Booming Silver Market

Dan Ives Unveils $700 2026 Target for Apple

Dan Ives Unveils $700 2026 Target for Apple

AU SFB Shares Surge to Record High After FDI Ceiling Raised to 74 %

AU SFB Shares Surge to Record High After FDI Ceiling Raised to 74 %

Top Cheap Stocks Under $10 to Buy in December 2024 - A Look Ahead to 2026

Top Cheap Stocks Under $10 to Buy in December 2024 - A Look Ahead to 2026

Apple Analyst Projects 31% Upside to 2026 Target Price

Apple Analyst Projects 31% Upside to 2026 Target Price

ISA Basics: Unlocking GBP20,000 of Tax-Free Savings

ISA Basics: Unlocking GBP20,000 of Tax-Free Savings

Union Pacific Merger Upside Already Priced In, Fueling Growth in U.S. Production Volumes

Union Pacific Merger Upside Already Priced In, Fueling Growth in U.S. Production Volumes

What If You'd Invested $3,500 in Tesla 12 Years Ago? The $250,000 Journey

What If You'd Invested $3,500 in Tesla 12 Years Ago? The $250,000 Journey

TDS Series A Preferred Yields 7.1% -- Highest Investment-Grade Return Today

TDS Series A Preferred Yields 7.1% -- Highest Investment-Grade Return Today

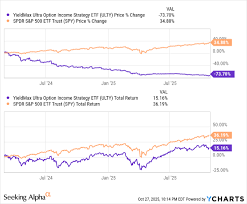

YieldMax Ultra Option Income ETF Lowers Distribution Targets Amid Strategy Shift

YieldMax Ultra Option Income ETF Lowers Distribution Targets Amid Strategy Shift

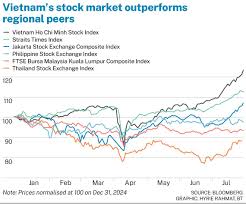

Vietnam's Stock Market Surges Over 30% in 2025, VN-Index Hits Record 2,900 Points

Vietnam's Stock Market Surges Over 30% in 2025, VN-Index Hits Record 2,900 Points

Jim Cramer Signals a "Reevaluation" of Costco While Hailing a Positive Development for Linde

Top 5 S&P 500 Dividend Aristocrats to Buy Before 2026

Jim Cramer Signals a "Reevaluation" of Costco While Hailing a Positive Development for Linde

Top 5 S&P 500 Dividend Aristocrats to Buy Before 2026

Unlocking Higher Yields: A Beginner's Guide to Investing in Non-Convertible Debentures

newsbytesapp.com

newsbytesapp.comLocale: INDIA

How to Invest in Non‑Convertible Debentures (NCDs): A Practical Guide

Non‑convertible debentures (NCDs) have emerged as a popular fixed‑income investment for retail investors looking to diversify beyond traditional bank deposits and government securities. The recent article on NewsBytes (https://www.newsbytesapp.com/news/lifestyle/how-to-invest-in-non-convertible-debentures/story) offers a concise yet comprehensive overview of what NCDs are, why they can be attractive, the risks involved, and a step‑by‑step roadmap to buying them. Below is a distilled summary that captures the essential points, while also pointing you toward related resources for deeper dives.

1. What Are Non‑Convertible Debentures?

- Definition: An NCD is a debt instrument issued by corporations (or sometimes public sector entities) that pays a fixed or floating coupon. Unlike convertible debentures, NCDs cannot be converted into equity shares.

- Issuer Types: Typically issued by private sector companies, Public‑Sector Undertakings (PSUs), and state‑owned enterprises looking for capital without diluting ownership.

- Maturity: Usually ranges from 1 to 10 years, with a small subset extending to 12–15 years.

2. Why Consider NCDs?

| Feature | Explanation |

|---|---|

| Higher Yields | Because they carry higher credit risk than government securities, NCDs offer coupons that can be 2–3% above comparable treasury bonds. |

| Regular Income | Most NCDs pay semi‑annual or quarterly coupons, making them suitable for income‑seeking investors. |

| Tax Efficiency | Under Indian tax law, the interest earned on NCDs is tax‑free for tax‑exempt NCDs, or taxed as per the investor’s slab for taxable ones. |

| Liquidity | While not as liquid as bank deposits, many NCDs can be traded on the National Stock Exchange (NSE) and BSE after 90 days. |

| Credit Flexibility | Corporations can issue NCDs to tap into a broader investor base without diluting equity holders. |

3. Risks to Keep in Mind

- Credit Risk – The primary risk; if the issuer defaults, investors may lose principal or interest. Credit rating agencies like CRISIL, ICRA, and CARE assign grades that help gauge default probability.

- Liquidity Risk – Some NCDs may not trade actively, especially during market stress.

- Call Risk – Certain NCDs are callable after a specific period, meaning the issuer can redeem them early, potentially before maturity.

- Interest Rate Risk – Rising rates can depress the market value of existing NCDs.

The article emphasizes the importance of conducting due‑diligence—reviewing the issuer’s financial health, industry outlook, and credit rating before investing.

4. Tax Treatment

- Tax‑Exempt NCDs: These offer zero tax on both coupon and capital gains (subject to SEBI regulations).

- Taxable NCDs: Interest income is taxed according to the investor’s slab rate. Capital gains on sale are treated as long‑term (taxed at 20% with indexation) if held for 12 months or more.

- The article advises consulting a tax advisor for personalized advice, especially if you have mixed portfolios of taxable and tax‑free NCDs.

5. How to Buy NCDs – Step‑by‑Step

- Open a Demat & Trading Account

- Use a broker that offers NCD trading. Many leading platforms (e.g., Zerodha, Upstox, ICICI Direct) provide a simple interface for buying and selling NCDs.

- Verify Eligibility

- As of 2023, only retail investors with a minimum of ₹20,000 in a demat account can trade NCDs. Check the latest SEBI circular for updates.

- Do Your Research

- Look at the issuance prospectus, the credit rating, and the issuer’s financial statements. The article links to a resource titled “How to Read an Issuer’s Annual Report for NCD Investors.”

- Place an Order

- Use the “Order Book” in your broker’s platform. Enter the NCD’s ISIN (e.g., “INR1234567890”) and the quantity.

- Confirm Settlement

- Settlement occurs on T+2. Ensure your demat account has the required shares to cover the NCD purchase (some brokers allow borrow‑to‑buy).

- Monitor

- Track coupon dates, maturity, and any call notices. Set alerts on your broker’s app to stay updated.

6. Tips for a Smarter NCD Investment

| Tip | Why It Matters |

|---|---|

| Diversify Across Issuers | Concentrating on one company can magnify credit risk. |

| Prefer High‑Rated NCDs | Even within the same issuer, a BBB‑ rating is safer than a BB‑. |

| Consider Tax‑Exempt Options | If you’re in a high tax bracket, a tax‑free NCD can significantly boost after‑tax returns. |

| Read the Call Terms | Some issuers offer a call option after 3 years; this could truncate your earnings. |

| Watch Market Liquidity | A high Bid‑Ask spread can inflate transaction costs. |

7. Related Reading (From the Original Article)

- “What is a Credit Rating Agency? A Deep Dive into CRISIL, ICRA, and CARE” – Helps you understand how ratings are assigned.

- “How to Evaluate Corporate Bond Ratings” – Offers a framework for interpreting ratings in the context of industry risk.

- “Comparing Tax‑Free vs. Taxable NCDs: Which One is Right for You?” – A side‑by‑side tax analysis.

These links, embedded in the article, provide further context for each of the steps above.

8. Bottom Line

Non‑convertible debentures can be a valuable addition to a diversified portfolio, especially for investors seeking higher yields than bank deposits but with a tolerance for moderate credit risk. By following the article’s practical steps—opening a demat account, researching issuers, understanding tax implications, and monitoring your holdings—you can position yourself to take advantage of the attractive coupon rates that NCDs offer.

Remember: Always read the Issuer’s Prospectus and Credit Rating carefully. If you’re unsure, consider consulting a financial advisor before committing capital.

Read the Full newsbytesapp.com Article at:

[ https://www.newsbytesapp.com/news/lifestyle/how-to-invest-in-non-convertible-debentures/story ]

TDS Series A Preferred Yields 7.1% -- Highest Investment-Grade Return Today

High-Yield Bonds: A New Income Source for Retirees in a Low-Yield World

High-Yield Bonds: A New Income Source for Retirees in a Low-Yield World

Why High-Yield Bonds Matter Right Now

Why High-Yield Bonds Matter Right Now

AGNC Investment Corp: A Three-Year Outlook on Mortgage-Backed REIT Performance

AGNC Investment Corp: A Three-Year Outlook on Mortgage-Backed REIT Performance