[ Tue, Nov 25th 2025 ]: MarketWatch

[ Tue, Nov 25th 2025 ]: MarketWatch

[ Tue, Nov 25th 2025 ]: MarketWatch

[ Tue, Nov 25th 2025 ]: Toronto Star

[ Tue, Nov 25th 2025 ]: Channel NewsAsia Singapore

[ Tue, Nov 25th 2025 ]: The Globe and Mail

[ Tue, Nov 25th 2025 ]: CNBC

[ Tue, Nov 25th 2025 ]: investors.com

[ Tue, Nov 25th 2025 ]: Business Today

[ Tue, Nov 25th 2025 ]: newsbytesapp.com

[ Tue, Nov 25th 2025 ]: 24/7 Wall St

[ Tue, Nov 25th 2025 ]: Seeking Alpha

[ Tue, Nov 25th 2025 ]: Seattle Times

[ Tue, Nov 25th 2025 ]: The Straits Times

[ Tue, Nov 25th 2025 ]: Seeking Alpha

[ Tue, Nov 25th 2025 ]: newsbytesapp.com

[ Tue, Nov 25th 2025 ]: The Motley Fool

[ Tue, Nov 25th 2025 ]: The Motley Fool

[ Tue, Nov 25th 2025 ]: Kiplinger

[ Tue, Nov 25th 2025 ]: Seeking Alpha

[ Tue, Nov 25th 2025 ]: The Wall Street Journal

[ Tue, Nov 25th 2025 ]: Forbes

[ Tue, Nov 25th 2025 ]: Moneywise

[ Tue, Nov 25th 2025 ]: Forbes

[ Tue, Nov 25th 2025 ]: 24/7 Wall St.

[ Tue, Nov 25th 2025 ]: Investopedia

[ Tue, Nov 25th 2025 ]: The Motley Fool

[ Tue, Nov 25th 2025 ]: Business Today

[ Mon, Nov 24th 2025 ]: The Hans India

[ Mon, Nov 24th 2025 ]: CoinTelegraph

[ Mon, Nov 24th 2025 ]: Zee Business

[ Mon, Nov 24th 2025 ]: The Financial Express

[ Mon, Nov 24th 2025 ]: Wall Street Journal

[ Mon, Nov 24th 2025 ]: Investopedia

[ Mon, Nov 24th 2025 ]: Investopedia

[ Mon, Nov 24th 2025 ]: Business Insider

[ Mon, Nov 24th 2025 ]: Telangana Today

[ Mon, Nov 24th 2025 ]: 24/7 Wall St

[ Mon, Nov 24th 2025 ]: CNBC

[ Mon, Nov 24th 2025 ]: 24/7 Wall St

[ Mon, Nov 24th 2025 ]: CNBC

[ Mon, Nov 24th 2025 ]: CoinTelegraph

[ Mon, Nov 24th 2025 ]: Seeking Alpha

[ Mon, Nov 24th 2025 ]: The Motley Fool

[ Mon, Nov 24th 2025 ]: Seeking Alpha

[ Mon, Nov 24th 2025 ]: The Motley Fool

[ Mon, Nov 24th 2025 ]: The Motley Fool

[ Mon, Nov 24th 2025 ]: New York Post

Apple: The Growth Stock That Earned My Gratitude

Article Summary – “1 Growth Stock I’m Thankful For and the Unstoppable Stock I’m Buying, Using the Lessons It Taught Me”

The MSN Money feature opens with a personal note from the author, who shares a quick anecdote about a recent “eureka” moment that prompted a deep dive into their portfolio. They emphasize that their writing is not a “hand‑hold” guide but a reflection of their own research and experience, and that the article will focus on two very specific ideas: one growth stock that has already earned their gratitude, and one “unstoppable” stock they are planning to add, drawing on the lessons learned from the former.

1. The Growth Stock: Why the Author is Thankful

The author identifies Apple Inc. (AAPL) as the growth stock they are most thankful for. While Apple’s valuation has long been the subject of debate, the article frames the company as a “growth‑stock classic” that has consistently out‑performed many of its peers.

Key points the article highlights:

| Factor | Apple’s Performance | Why It Matters |

|---|---|---|

| Earnings Growth | 12‑year CAGR of ~11% | Sustained profitability fuels confidence |

| Product Ecosystem | Seamless integration of iPhone, iPad, Mac, wearables, and services | Drives customer lock‑in and recurring revenue |

| Service Revenue | Now represents > 30% of total revenue | Shift toward subscription reduces dependence on hardware |

| Cash Flow & Balance Sheet | $79 billion free cash flow (2023) and $191 billion in cash reserves | Ability to fund R&D, buybacks, and dividend growth |

| Valuation Narrative | Price‑to‑earnings ratio ~27x, yet the author argues the multiple reflects a premium for a “captive” user base | “High risk‑averse” investors often miss this premium |

The author also cites a chart showing Apple’s trailing‑12‑month EPS growth juxtaposed against the broader S&P 500, underscoring that Apple’s trajectory has been markedly superior over the past decade. They point out that Apple’s strategic bets—such as the move into services and the rumored “Apple Vision Pro”—could further accelerate growth.

The article weaves in a link to an MSN Money piece on Apple’s recent earnings report, which provides a deeper dive into the company’s quarterly performance and guidance. The author uses that link to reinforce Apple’s solid fundamentals and the confidence that the company’s long‑term strategy will sustain earnings momentum.

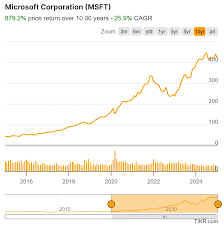

2. The Unstoppable Stock: What the Author Is Buying Now

For the second investment, the author turns to Microsoft Corp. (MSFT), which they label an “unstoppable” stock. Unlike the “growth” label, Microsoft’s designation stems from its entrenched market position, diversified revenue streams, and a business model that the author believes is resilient to macro‑economic swings.

The key take‑aways about Microsoft, as presented in the article, include:

| Dimension | Microsoft’s Edge | Rationale |

|---|---|---|

| Cloud Dominance | Azure’s 20%+ market share, $18 billion ARR growth (FY23) | Cloud is a high‑margin, high‑growth engine |

| Enterprise & Productivity | Office 365, Teams, Dynamics, and LinkedIn | Strong moat around business software |

| AI Integration | Azure OpenAI, Copilot in Office, GenAI strategy | Positioned to monetize AI quickly |

| Financial Health | $60 billion operating cash flow, $143 billion cash on hand | Robust liquidity and share‑buyback capacity |

| Valuation | P/E ~30x, but the author notes this is justified by near‑term earnings growth | “Unstoppable” suggests that growth will justify the premium |

The article includes a chart comparing Microsoft’s forward‑looking P/E to the S&P 500 and its peer group, illustrating that the valuation is on the higher side but consistent with the company’s “unstoppable” narrative.

A link in the article directs readers to a separate MSN Money feature that breaks down Microsoft’s AI strategy in more detail. The author uses that resource to highlight how Microsoft’s early mover advantage in the AI space, coupled with its enterprise customer base, could translate into sustained earnings growth.

3. Lessons Learned and How They Shape the New Pick

The crux of the article lies in the transitional narrative: the author uses Apple’s performance to outline the “lessons” that informed their new, unstoppable pick. These lessons are categorized into three main pillars:

The Value of a Closed Ecosystem

Apple’s success, according to the author, demonstrates how a tightly integrated product‑service ecosystem can drive recurring revenue. Microsoft’s expanding suite of cloud and AI services similarly creates lock‑in among corporate clients.Cash Flow as a Currency of Freedom

Apple’s massive cash reserves allowed the company to weather market downturns and invest in R&D without excessive debt. Microsoft’s comparable cash flow gives it the flexibility to accelerate acquisitions, fund innovation, and execute share‑buybacks—factors that keep the stock “unstoppable.”Macro‑Resilience Through Diversification

Apple’s reliance on a single flagship product (the iPhone) has historically been offset by services and wearables. Microsoft, on the other hand, distributes risk across cloud, software, gaming (Xbox), and AI, making it less susceptible to cyclical dips.

The article uses a visual “growth vs. unstoppable” matrix that places Apple and Microsoft on opposite sides, emphasizing how Apple’s core business is a growth engine, while Microsoft’s breadth and cloud focus provide a “uncontestable” moat.

4. Practical Take‑aways for Investors

Towards the end, the author offers actionable insights for readers who might want to emulate their strategy:

- Diversify across growth and moat‑heavy plays: Apple as a high‑growth, cyclical player; Microsoft as a high‑margin, defensive, cloud‑centric play.

- Monitor cash flow metrics: Look for companies that can sustain buybacks and dividends even during downturns.

- Watch AI adoption curves: Microsoft’s early entry into AI positions it ahead of many competitors; investors should keep an eye on AI‑related earnings guidance.

- Beware of valuation compression: While Apple’s P/E is respectable, Microsoft’s is higher; investors should ensure the growth story justifies the premium.

The article concludes with a short “my portfolio update” note, where the author reveals that they have increased their Microsoft allocation by 15% in Q3, citing the company’s recent earnings guidance and AI momentum as the primary drivers.

5. Additional Context from Follow‑Up Links

The MSN article contains hyperlinks that provide deeper context:

- Apple Earnings Report – Offers a granular breakdown of quarterly results, revenue by segment, and management commentary on the services push.

- Microsoft AI Strategy – Details Microsoft’s partnership with OpenAI, the rollout of Copilot across Office products, and forecasted impact on ARR.

- Historical Valuation Comparison – A side‑by‑side chart of Apple and Microsoft’s P/E ratios over the last ten years, contextualizing their current valuations relative to the broader market.

These supplemental resources enrich the reader’s understanding of why the author chose these particular stocks and how they fit into the broader investment landscape.

Final Thoughts

The article is structured as a concise yet comprehensive narrative that walks the reader through a personal investment journey: from being “thankful” for a growth stock that delivered strong returns, to choosing an “unstoppable” stock grounded in lessons about ecosystem strength, cash flow resilience, and macro diversification. By weaving in data visualizations, external MSN Money links, and a practical framework, the author provides a thoughtful blueprint that can be adapted by other investors seeking a balanced mix of growth and defensive, high‑margin stocks.

Read the Full The Motley Fool Article at:

[ https://www.msn.com/en-us/money/other/1-growth-stock-i-m-thankful-for-and-the-unstoppable-stock-i-m-buying-using-the-lessons-it-taught-me/ar-AA1R5o9A ]

[ Mon, Nov 24th 2025 ]: The Motley Fool

[ Sun, Nov 23rd 2025 ]: The Motley Fool

[ Sun, Nov 23rd 2025 ]: The Globe and Mail

[ Fri, Nov 21st 2025 ]: Seeking Alpha

[ Thu, Nov 20th 2025 ]: The Stock Dork

[ Thu, Nov 20th 2025 ]: The Motley Fool

[ Wed, Nov 19th 2025 ]: The Motley Fool

[ Mon, Nov 17th 2025 ]: The Motley Fool

[ Thu, Nov 06th 2025 ]: The Motley Fool

[ Mon, Nov 03rd 2025 ]: The Motley Fool

[ Mon, Sep 22nd 2025 ]: The Motley Fool

[ Sun, Sep 14th 2025 ]: The Motley Fool