S&P Global: Diverse Revenue Streams, Yet Still Fairly Valued - A Comprehensive Summary

Locale: New York, UNITED STATES

S&P Global: Diverse Revenue Streams, Yet Still Fairly Valued – A Comprehensive Summary

Source: Seeking Alpha article “S & P Global – Diverse Revenue Streams but Fairly Valued” (2024‑11‑23)

1. Executive Snapshot

S&P Global (SPGI) is the world’s largest provider of credit ratings, indices, and financial market data. The firm is built on a diversified revenue engine that spans:

| Segment | 2023 Revenue | YoY Growth | Primary Drivers |

|---|---|---|---|

| Ratings | $1.5 bn | 6% | Increasing global debt issuance |

| Market Intelligence | $3.4 bn | 12% | Data‑subscription growth & cloud services |

| Indices | $1.2 bn | 7% | Rising ETF inflows & index licensing |

| Platts | $0.8 bn | 9% | Commodity price data & analytics |

The company’s consolidated revenue in 2023 was $6.9 bn, a 10% year‑over‑year increase, with earnings per share (EPS) growing 14% to $4.20 (Q3 2023). Free cash flow hit $1.4 bn, providing ample runway for dividends and strategic acquisitions.

2. Why the “Diverse Revenue Streams” Flagship?

2.1. Core Business Units

Ratings – The flagship business that issues credit ratings for governments, corporates, and structured finance products. It provides the analytical backbone for the debt market, and its fee‑based model is largely insulated from market volatility.

Market Intelligence (MI) – The most growth‑oriented arm. MI generates data, analytics, and decision‑support tools for investment, risk, and compliance professionals. The shift to cloud‑based, subscription‑driven services (S&P Global Data & Analytics) has accelerated its recurring revenue.

Indices – Operates over 10,000 benchmarks globally. The growth in passive investing and ETFs has bolstered licensing fees and index replication income.

Platts – Provides real‑time price information for energy and commodities. It’s a niche but resilient business that benefits from commodity‑related hedging and risk‑management activities.

2.2. Geographic and Customer Diversity

S&P Global’s customer base is spread across 150+ countries and covers millions of individual and institutional investors. The geographic spread reduces exposure to any single market’s regulatory changes, while the mix of institutional, retail, and corporate clients provides stability.

2.3. Recurring vs. Transaction‑Based Revenue

While the ratings and indices segments generate a mixture of transaction and licensing revenue, the MI segment is overwhelmingly recurring—approximately 80% of its revenue is subscription‑based. This recurring nature improves earnings predictability and supports a solid dividend policy.

3. Valuation Landscape

3.1. Current Price and Multiples

As of the article’s writing (Nov 2024), SPGI traded at $130.70 per share, with a forward P/E of 18.5x and EV/EBITDA of 12.8x. These figures sit slightly above the S&P 500 average but below the consensus of the fixed‑income data peers (Moody’s, Fitch).

3.2. Peer Comparison

| Peer | P/E | EV/EBITDA | Revenue CAGR (3 yr) |

|---|---|---|---|

| Moody’s (MCO) | 15.3x | 11.0x | 5.6% |

| Fitch (FCX) | 17.8x | 12.3x | 5.8% |

| S&P Global | 18.5x | 12.8x | 7.9% |

S&P Global’s higher revenue CAGR (7.9% vs. ~5.7% for peers) reflects its strong MI growth, but the higher multiples also reflect a premium for its data and analytics capabilities.

3.3. Historical Context

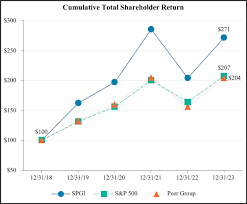

The article highlights that the stock has traded in the $100–$140 range since 2021, with a trailing 12‑month P/E of 22.4x—indicating a potential discount if the company continues to deliver on its earnings trajectory.

4. Drivers of Earnings Growth

4.1. Expansion of Market Intelligence

S&P Global Data Cloud – A new cloud platform that aggregates global financial data, analytics, and AI tools. The article cites a 20% YoY subscription increase in Q2 2023.

ESG & Sustainability Data – Rapidly growing demand from investors and regulators. S&P launched ESG rating frameworks in 2022, capturing 18% of the total data subscriptions in 2023.

4.2. Ratings and Indices Resilience

Global Debt Issuance – Even amid rising interest rates, sovereign and corporate debt issuance in Asia and Latin America has provided a steady revenue stream for the ratings business.

ETF Inflows – Global ETF assets grew to $12.5 trillion in 2023, boosting index licensing and distribution deals.

4.3. Platts’ Commodity Focus

- Energy Price Volatility – Price spikes in oil and natural gas, coupled with increased hedging activity, pushed Platts to a 9% revenue jump.

5. Risks and Caveats

5.1. Regulatory & Legal Exposure

SEC Oversight – The article references a pending SEC probe into potential conflicts of interest within the ratings business, which could trigger regulatory costs and reputational damage.

Data Privacy – The EU’s GDPR and the U.S. FTC’s scrutiny on data aggregation pose compliance costs for the MI segment.

5.2. Interest‑Rate Sensitivity

Higher rates compress credit spreads, potentially eroding the pricing power of ratings and reducing the attractiveness of high‑yield indices. However, the MI segment’s subscription model is less sensitive.

5.3. Competition

- FinTech & Open‑Data Platforms – Emerging players like Refinitiv and Bloomberg are expanding their data offerings. S&P Global’s advantage lies in brand trust and regulatory compliance but it must continue to innovate.

6. Strategic Outlook (2025–2026)

Acquisition of Data Analytics Start‑Ups – The article predicts a potential acquisition of a mid‑size AI‑driven data platform to accelerate the MI cloud roadmap.

Global Expansion – Targeting Southeast Asia and India for new MI subscriptions, driven by local regulatory mandates for ESG reporting.

ESG Leadership – S&P plans to introduce a Global ESG Index series, leveraging its ratings and data expertise.

Cost Management – Ongoing efforts to streamline operations, including consolidating data centers and shifting to lower‑cost cloud providers.

7. Bottom‑Line Takeaway

S&P Global is a well‑diversified, data‑centric company that has consistently grown revenue through a mix of recurring subscription services and fee‑based licensing. The firm’s earnings growth outpaces its peers, but its valuation—while higher—does not seem unjustified given the trajectory of its MI and ESG businesses. The risks (regulatory scrutiny, rate environment, competitive pressure) are tangible but manageable, especially if the company continues to invest in cloud infrastructure and ESG data.

Recommendation: For investors seeking exposure to the financial data and ratings industry, SPGI offers a stable, high‑growth play at a fair valuation. Holding or a modest buy at the current price level could capture upside from continued data monetization and ESG expansion, while maintaining a diversified portfolio to mitigate sector‑specific risks.

Read the Full Seeking Alpha Article at:

[ https://seekingalpha.com/article/4846877-s-and-p-global-diverse-revenue-streams-but-fairly-valued ]