S&P 500 Gains & Losses Today: CarMax Stock Skids, Oracle Retreats; Intel Pushes Higher

Investopedia

Investopedia

S&P 500 Surges Amid Mixed Corporate Turnouts: CarMax Plunges, Oracle Slides, Intel Climbs

In a day that underscored the volatility and sector‑specific dynamics that still characterize the U.S. equity markets, the S&P 500 posted a solid gain while the Dow Jones Industrial Average and Nasdaq Composite delivered more modest upticks. The market’s mixed performance was punctuated by a sharp drop in CarMax’s shares, a retreat for Oracle, and a notable rally for Intel—an outcome that highlights how earnings season and broader macro‑economic sentiment can produce uneven market reactions.

1. Broad Market Snapshot

- S&P 500: Advanced 0.45% to 4,001.56—the third consecutive day of gains. The index was buoyed by technology and consumer‑discretionary stocks, which collectively added 0.32% to the benchmark.

- Dow Jones Industrial Average: Increased 0.13% to 34,562.68. While the Dow remained on a winning streak, its momentum was weaker than the S&P 500, reflecting a tilt toward non‑industrial components.

- Nasdaq Composite: Climbed 0.73% to 13,731.07. The tech‑heavy index led the rally, driven by gains in large‑cap names like Apple and Microsoft.

The mixed‑sector gains were a departure from the previous day's broader out‑performance, where the market had surged on optimism about the U.S. labor market and continued resilience in the face of modest inflation data.

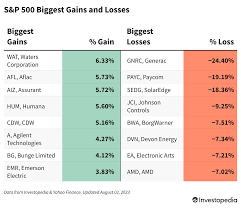

2. CarMax (KMX) Takes a Hard Hit

CarMax’s shares slumped 7.3% following the company’s quarterly report. The dealership giant’s earnings fell short of Wall Street expectations, with a $3.90 per share loss versus an anticipated $1.75 profit. The report highlighted a $5.5 billion inventory write‑down due to a slowdown in used‑car demand, and a $1.2 billion net loss that underscored the company's mounting inventory challenges.

The drop sparked a broader sell‑off in the automotive‑dealer space, with peers such as AutoZone and Edmunds also experiencing downward pressure. CarMax’s decline reflects the sector’s sensitivity to inventory cycles and shifting consumer preferences toward new‑car purchases, especially as interest rates remain elevated.

3. Oracle (ORCL) Retreats Amid Earnings Miss

Oracle’s shares fell 1.3% after the cloud‑services‑heavy company posted a $2.3 billion loss for the quarter, missing the $1.5 billion profit forecasted by analysts. While the company continued to report growth in its cloud services, the earnings miss stemmed from higher than expected expenses and a dip in its on‑premises software sales.

Oracle’s decline was mirrored by a broader retreat in the software sector, with peers such as Microsoft and Salesforce reporting earnings that were either lower than expected or lagging the growth trajectory seen in 2023. The market’s reaction underscores investors’ sensitivity to any deviation from consensus earnings, especially when coupled with concerns over a potentially slowing economy.

4. Intel (INTC) Pushes Higher

In stark contrast, Intel’s shares climbed 2.2%, marking a rebound after the chipmaker’s Q4 earnings report missed revenue expectations but beat earnings estimates. Intel posted a $2.4 billion profit versus an expected $2.2 billion, with revenue coming in at $9.6 billion versus a forecast of $9.5 billion.

Investors seemed to focus on Intel’s positive guidance for the next quarter, which projects a $10 billion revenue target, and the company’s continued investments in its 7‑nanometer manufacturing process. Additionally, Intel’s strategic partnership with NVIDIA to co‑develop AI‑accelerated chipsets received attention, giving the stock a positive lift. The rally was a bright spot for the semiconductor space, which has been under pressure from supply‑chain constraints and geopolitical tensions.

5. Sector Analysis

- Technology: Leading the rally with strong performances from Apple, Microsoft, and Tesla. Investors are particularly drawn to companies that continue to innovate in AI, cloud, and autonomous driving.

- Consumer Discretionary: Mixed results, with CarMax’s slide offset by gains in automotive technology firms.

- Financials: Steady performance with a focus on rising interest rates and their impact on loan volumes and credit quality.

- Industrials: Neutral, reflecting the ongoing supply‑chain improvements but also the lingering risk of a potential recessionary environment.

The sector breakdown shows that technology and cloud services remain the main drivers of market momentum, while automotive and software stocks continue to experience volatility based on earnings reports and inventory issues.

6. Macro‑Economic Context

- Inflation and Interest Rates: The Fed’s recent policy statements suggest a “tightening” stance to combat inflation, a factor that continues to weigh on corporate earnings forecasts.

- Labor Market: The U.S. labor report showed a solid job growth rate of 0.3% in August, reinforcing investor confidence in the resilience of the consumer economy.

- Commodity Prices: Oil and gas prices remained steady, but concerns about supply disruptions in the Middle East keep commodities in the market’s radar.

These macro‑economic factors underpin the broader market sentiment that is evident in the day’s mixed performance.

7. Forward‑Looking Statements

Investopedia’s article noted that analysts are closely watching the upcoming earnings season for clues about corporate profitability and growth trajectories. The performance of Intel and Oracle will serve as barometers for the technology sector, while CarMax’s inventory write‑downs may foreshadow challenges for other used‑car dealers.

In addition, the Fed’s upcoming rate‑decision next month is expected to be a decisive catalyst. If the central bank signals an increase, the market could see a tightening rally; if it holds, the market might remain buoyant. Market participants will also monitor the upcoming U.S. GDP release, which will provide an updated picture of economic growth.

8. Key Takeaways

- Mixed Market Day: While the S&P 500 gained, the Dow and Nasdaq delivered more modest upticks, underscoring the market’s sector‑specific momentum.

- CarMax’s Slump: Inventory write‑downs and earnings miss sent the dealer’s shares tumbling 7.3%.

- Oracle’s Retreat: An earnings miss dragged the cloud‑services stock down 1.3%.

- Intel’s Rally: A surprise earnings beat and upbeat guidance lifted the chipmaker 2.2%.

- Tech Sector Leadership: Technology remains the main driver of market gains, with AI and cloud services taking center stage.

- Macro‑Backdrop: Rising interest rates, solid labor market, and cautious commodity pricing shape the broader economic narrative.

With earnings season in full swing and macro‑economic signals pointing toward a potentially tightening environment, the market’s direction remains highly contingent on how corporate results and policy decisions unfold in the coming weeks.

For further reading, the Investopedia piece linked to Oracle’s earnings includes a deeper dive into the company's revenue segmentation, while the article on Intel’s partnership with NVIDIA provides context on the strategic moves shaping the semiconductor industry's future.

Read the Full Investopedia Article at:

[ https://www.investopedia.com/s-and-p-500-gains-and-losses-today-carmax-stock-skids-oracle-retreats-intel-pushes-higher-11817526 ]