by: moneycontrol.com

by: TheWrap

Paramount Sells 20% Stake in International Distribution to Warner-Discovery Amid Democratic Scrutiny

by: Fortune

")

by: newsbytesapp.com

Unlocking Higher Yields: A Beginner's Guide to Investing in Non-Convertible Debentures

by: Seeking Alpha

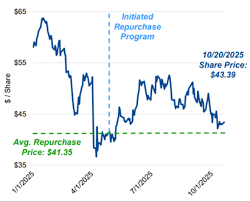

Griffin Corporation (GFF) Receives Fresh Sell Rating Amid Declining Revenue and Rising Debt

Receives Fresh Sell Rating Amid Declining Revenue and Rising Debt")

High-Yield Energy Stocks: A Three-Stock Strategy for 2025

The Motley Fool

The Motley FoolLocale: UNITED STATES

High-Yield Energy Stocks: A Three‑Stock Strategy for 2025

The Motley Fool’s December 10, 2025 article, “3 No‑Brainer High‑Yield Energy Stocks to Buy With”, offers investors a concise yet comprehensive look at three energy companies that the author believes deliver attractive dividend yields, strong fundamentals, and resilience in a shifting market. The piece is framed around the premise that, despite the growing emphasis on renewable energy, traditional energy firms still represent solid cash‑generating assets—particularly for income‑focused portfolios. Below is a detailed summary of the key points and the reasoning behind each pick.

1. Exxon Mobil (XOM)

Dividend Profile and Yield

Exxon Mobil is highlighted for its historically robust dividend payout, which consistently averages around 5.5% to 6% in recent years. The article notes that the company’s dividend has grown for over 30 consecutive quarters, underscoring a long‑term commitment to shareholder returns.

Earnings Stability

The author points out Exxon’s diversified portfolio—including upstream (exploration & production), midstream (pipeline transport), and downstream (refining & marketing) operations—as a buffer against market volatility. This integration allows Exxon to smooth earnings during periods of fluctuating oil prices.

Valuation and Growth Catalysts

Exxon is described as trading at a discount to its 12‑month average P/E ratio, which the article interprets as a buying opportunity. Moreover, the piece cites the upcoming pipeline expansion projects and the company’s investment in advanced drilling technologies as potential catalysts for future earnings growth.

Risk Considerations

While praising Exxon’s stability, the author also notes the company’s exposure to regulatory risks and the broader shift toward decarbonization. Nonetheless, the argument is that the high dividend yield offsets these risks for income‑seeking investors.

2. Chevron (CVX)

Dividend Yield and Growth

Chevron’s dividend yield is cited in the range of 5.0% to 5.5%, and the company has a similar track record of consecutive dividend increases as Exxon. The article emphasizes Chevron’s disciplined capital allocation strategy—particularly its systematic reduction of debt—which has bolstered investor confidence.

Market Position

Chevron’s strength lies in its upstream focus, coupled with a sizeable global refining footprint. The article highlights recent acquisition of upstream assets in Brazil and the U.S. Midwest as evidence of the company’s proactive growth strategy.

Financial Health

Chevron’s balance sheet is described as “robust,” with a debt‑to‑equity ratio that has improved year over year. The author also references the company’s strong free‑cash‑flow generation, which supports its dividend policy and allows for potential share repurchases.

Valuation

Compared to its peers, Chevron is positioned at a modestly higher valuation multiple, but the article argues that this is justified by its superior dividend payout and relatively low risk profile.

3. Phillips 66 (PSX)

Dividend and Yield

Phillips 66 is singled out for its attractive dividend yield of approximately 5.8%–6.2%. Unlike the upstream giants, Phillips 66 is a midstream and downstream company, which the article claims gives it a steadier revenue base amid fluctuating crude prices.

Business Model

The piece underscores Phillips 66’s extensive refining network and its logistics infrastructure, including pipelines and storage facilities. This network enables the company to capture value across the entire oil value chain, from crude delivery to refined product sales.

Strategic Moves

Recent strategic initiatives, such as the acquisition of a refining stake in the Midwest and investments in renewable fuel blending, are highlighted as ways the company is positioning itself for a transition‑ready future.

Balance Sheet and Dividend Sustainability

Phillips 66’s balance sheet is described as healthy, with a moderate debt level and ample cash reserves. The article cites the company’s dividend payout ratio, which sits at a sustainable 60–70%, indicating that dividends are well‑backed by earnings.

Risk Profile

The article acknowledges that Phillips 66 is subject to commodity price swings and regulatory pressures related to environmental standards. However, the author argues that the company’s diversified operations mitigate these risks relative to pure upstream peers.

Contextual Themes Discussed in the Article

Energy Transition and Market Dynamics

The author briefly touches on the global shift toward renewable energy and the potential impact on oil demand. While this trend poses long‑term headwinds, the article contends that the transition will be gradual, and the immediate market conditions still favor high‑yield energy stocks. It references a linked analysis on “The Energy Transition: How Much Oil Will Still Be Needed?” to illustrate that fossil fuels remain integral to global infrastructure for the foreseeable future.

Dividend‑Focused Investment Strategy

Throughout the piece, there is a strong emphasis on income generation. The article argues that, for investors with a moderate risk tolerance or for those seeking a reliable cash flow stream, high‑yield energy stocks are a “no‑brainer.” It cites a separate link to “Why Dividend Stocks Matter for Your Portfolio” to back this assertion.

Risk‑Reward Assessment

Each stock’s risk factors are balanced against the potential reward. For example, Exxon and Chevron’s high dividend yields are juxtaposed with their exposure to geopolitical risk (e.g., sanctions on Russia, U.S.‑China trade tensions). Phillips 66’s diversified operations are presented as a hedge against upstream volatility. The article encourages readers to consider these dynamics when evaluating their own portfolio allocation.

Bottom‑Line Takeaway

The Motley Fool’s article recommends that investors who prioritize dividend income, robust cash flow, and a degree of operational diversification consider adding Exxon Mobil, Chevron, and Phillips 66 to their holdings. The author frames these three names as “no‑brainer” buys because they combine historically strong dividend growth, solid financial health, and strategic positioning in a market that still heavily relies on fossil fuels. The article concludes by advising readers to align their investment decisions with their risk tolerance and income objectives, while keeping an eye on regulatory developments and the evolving energy landscape.

In sum, the piece offers a concise, data‑driven argument for a focused high‑yield energy strategy, backed by recent company performance, valuation metrics, and broader market context. It serves as a useful starting point for income investors looking to weigh the merits of traditional energy stocks amid a world increasingly aware of climate change.

Read the Full The Motley Fool Article at:

https://www.fool.com/investing/2025/12/10/3-no-brainer-high-yield-energy-stocks-to-buy-with/

on: Sat, Nov 22nd 2025

by: The Motley Fool

November 2025 Dividend Picks: PG, JNJ, and NextEra Lead the Charge

on: Wed, Dec 03rd 2025

by: The Motley Fool

Enbridge's 5.6% Yield Outpaces U.S. Large-Cap and High-Dividend ETFs

on: Thu, Nov 13th 2025

by: 24/7 Wall St

November 2025 High-Yield Playbook: The Top Dividend Stars in the S&P 500

on: Sat, Dec 06th 2025

by: The Motley Fool

Realty Income Surpasses ANaly Capital in Dividend Growth and Stability

on: Sun, Nov 30th 2025

by: 24/7 Wall St

Turn a $2,500 Investment into a $4,000-Per-Year Dividend Income Stream

on: Sat, Nov 29th 2025

by: The Motley Fool

Bristol Myers Squibb's 4.5% Dividend: A 2025 Income Opportunity

on: Mon, Nov 24th 2025

by: The Motley Fool

on: Sun, Nov 23rd 2025

by: Seeking Alpha

Galaxy Digital's Data-Center Business Drives Recent Stock Rally

on: Mon, Dec 08th 2025

by: Seeking Alpha

Seeking Income Spotlight: Two Dividend Upgrades Exceeding 10%

on: Sun, Dec 07th 2025

by: The Motley Fool

Three Dividend-Yield Powerhouses to Add to Your Portfolio Right Now

on: Sun, Nov 30th 2025

by: Seeking Alpha

on: Tue, Nov 25th 2025

by: The Motley Fool

Berkshire Hathaway Eyes $2.5 Trillion Market Cap by 2030: A Bold Bullish Forecast