[ Thu, Jan 29th ]: socastsrm.com

[ Thu, Jan 29th ]: CNBC

[ Thu, Jan 29th ]: 24/7 Wall St.

[ Thu, Jan 29th ]: Investopedia

[ Thu, Jan 29th ]: Seeking Alpha

[ Thu, Jan 29th ]: Seeking Alpha

[ Thu, Jan 29th ]: The Motley Fool

[ Wed, Jan 28th ]: NY Post

[ Wed, Jan 28th ]: Seattle Times

[ Wed, Jan 28th ]: Barron's

[ Wed, Jan 28th ]: Local 12 WKRC Cincinnati

[ Wed, Jan 28th ]: WGME

[ Wed, Jan 28th ]: Fox 11 News

[ Wed, Jan 28th ]: wjla

[ Wed, Jan 28th ]: WTOP News

[ Wed, Jan 28th ]: The Globe and Mail

[ Wed, Jan 28th ]: CNBC

[ Wed, Jan 28th ]: New York Post

[ Wed, Jan 28th ]: Investopedia

[ Wed, Jan 28th ]: CNBC

[ Wed, Jan 28th ]: MarketWatch

[ Wed, Jan 28th ]: Goodreturns

[ Wed, Jan 28th ]: ThePrint

[ Wed, Jan 28th ]: reuters.com

[ Wed, Jan 28th ]: MarketWatch

[ Wed, Jan 28th ]: MarketWatch

[ Wed, Jan 28th ]: The Motley Fool

[ Wed, Jan 28th ]: The Motley Fool

[ Wed, Jan 28th ]: Channel NewsAsia Singapore

[ Wed, Jan 28th ]: Seeking Alpha

[ Wed, Jan 28th ]: Seeking Alpha

[ Wed, Jan 28th ]: The Motley Fool

[ Wed, Jan 28th ]: CNBC

[ Wed, Jan 28th ]: Seeking Alpha

[ Wed, Jan 28th ]: moneycontrol.com

[ Wed, Jan 28th ]: The Motley Fool

[ Tue, Jan 27th ]: Seeking Alpha

[ Tue, Jan 27th ]: Seeking Alpha

[ Tue, Jan 27th ]: The Motley Fool

[ Tue, Jan 27th ]: Seeking Alpha

[ Tue, Jan 27th ]: The Motley Fool

[ Tue, Jan 27th ]: The Motley Fool

[ Tue, Jan 27th ]: AOL

[ Tue, Jan 27th ]: 24/7 Wall St.

[ Tue, Jan 27th ]: Insider Monkey

[ Tue, Jan 27th ]: AOL

[ Tue, Jan 27th ]: YouTube

[ Tue, Jan 27th ]: USA Today

Comfort Systems USA: Strong Performance, Premium Valuation

Locale: UNITED STATES

Wednesday, January 28th, 2026 - Comfort Systems USA (CSUSA), a national leader in commercial HVAC services, continues to demonstrate robust operational performance. However, the question remains: does the stock price reflect a realistic outlook, or is it already factoring in too much optimism? This analysis dives deeper into CSUSA's current position, examining its strengths in execution alongside its increasingly challenging valuation.

A Consistent Record of Growth & Strategic Acquisitions

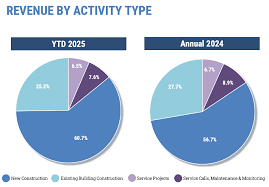

CSUSA's success isn't accidental. For years, the company has reliably demonstrated impressive organic growth, a testament to strong management and a keen understanding of the commercial HVAC market. This organic growth has been consistently supplemented by a strategic acquisition strategy. CSUSA doesn't just buy companies; it integrates them effectively, leveraging synergies and expanding its service offerings. This disciplined approach to mergers and acquisitions has been a cornerstone of its long-term success.

Crucially, the company's current backlog provides a solid foundation for continued revenue generation. The sustained demand for CSUSA's services is a clear indicator of both the health of the commercial construction sector and the company's ability to secure significant projects. Industry sources suggest that ongoing trends towards energy efficiency and increasingly complex HVAC requirements are further bolstering demand. Furthermore, the company is consistently reporting strong pricing power, allowing it to maintain healthy margins even amidst inflationary pressures.

Navigating a Fragmented Market

The commercial HVAC industry itself is notoriously fragmented, comprised of numerous regional and local players. This presents both challenges and opportunities for CSUSA. The challenge lies in coordinating a national network and maintaining consistent service quality across diverse geographic locations. However, the fragmentation also presents significant opportunities for further consolidation - opportunities CSUSA appears well-positioned to capitalize on. The company's established reputation and financial stability make it an attractive acquirer for smaller, family-owned businesses looking for an exit strategy.

The Valuation Concern: Is the Price Justified?

While CSUSA's operational performance is undeniably strong, the core concern for many analysts currently centers on the company's valuation. As of today, CSUSA's price-to-earnings (P/E) ratio is significantly elevated compared to both its historical averages and those of its peers. The Enterprise Value to EBITDA (EV/EBITDA) multiple paints a similar picture - a premium valuation that suggests the market is expecting exceptional future growth.

This isn't to say CSUSA is overvalued in an absolute sense. A strong company deserves a premium valuation. However, the question is whether the current price adequately discounts potential risks and leaves room for further appreciation. Several factors contribute to this stretched valuation. Optimism surrounding infrastructure spending, coupled with a generally bullish market sentiment, has undoubtedly played a role. Additionally, CSUSA's consistent execution has fostered investor confidence, driving up demand for the stock.

However, macroeconomic headwinds - including potential interest rate hikes and a possible slowdown in commercial construction - could quickly impact the company's earnings. If growth decelerates, the current valuation becomes increasingly difficult to justify. It's also worth noting that the HVAC sector is cyclical, and while demand is strong now, it's unlikely to remain at this level indefinitely.

Looking Ahead: Cautious Optimism and a Potential Entry Point

Comfort Systems USA remains a fundamentally sound company. Its strong execution, strategic acquisitions, and favorable position within a fragmented market are all compelling attributes. However, the current valuation leaves little margin for error. Current investors should closely monitor the company's performance and be prepared to adjust their positions if growth begins to slow.

For potential new investors, a period of observation may be prudent. Waiting for a more attractive entry point - perhaps a temporary dip in the stock price triggered by broader market volatility or company-specific news - could yield a better long-term return. While CSUSA is a quality company, paying a premium price for a stock requires a high degree of confidence in its ability to consistently exceed expectations. The company's next earnings report will be a critical factor in determining whether the current valuation is sustainable or requires a reassessment.

Read the Full Seeking Alpha Article at:

[ https://seekingalpha.com/article/4863327-comfort-systems-usa-execution-strong-valuation-stretched ]

[ Sat, Jan 24th ]: Seeking Alpha

[ Thu, Jan 22nd ]: Seeking Alpha

[ Wed, Jan 21st ]: Seeking Alpha

[ Wed, Jan 21st ]: Seeking Alpha

[ Wed, Jan 21st ]: Seeking Alpha

[ Tue, Jan 20th ]: Seeking Alpha

[ Sun, Jan 18th ]: Seeking Alpha

[ Wed, Dec 24th 2025 ]: Seeking Alpha

[ Sat, Dec 20th 2025 ]: Seeking Alpha

[ Tue, Dec 16th 2025 ]: Seeking Alpha

[ Sat, Dec 13th 2025 ]: The Motley Fool

[ Tue, Nov 25th 2025 ]: The Motley Fool