Galp Energia: Market Underperformer with Long-Term Potential

Galp Energia: Market Underperformer with Long-Term Potential

Trump Media Stock: $1,000 Investment's Wild Ride in 2024

Trump Media Stock: $1,000 Investment's Wild Ride in 2024

Shoe Carnival's Transformation: Is Shoe Station Succeeding?

Shoe Carnival's Transformation: Is Shoe Station Succeeding?

Year-End Market Review: Mixed Performance & Lingering Uncertainty

Year-End Market Review: Mixed Performance & Lingering Uncertainty

Microsoft Poised for Strong Growth: A Top Pick for 2026?

Microsoft Poised for Strong Growth: A Top Pick for 2026?

Intel's Turnaround Story Gains Momentum, Sparking Investor Optimism

Intel's Turnaround Story Gains Momentum, Sparking Investor Optimism

Slate Pool Partners REIT: A Potential Income Stream for TFSAs

Slate Pool Partners REIT: A Potential Income Stream for TFSAs

AI Revolutionizes Retail: Stocks to Watch by 2026

AI Revolutionizes Retail: Stocks to Watch by 2026

Stocks Surge and Slide: Midday Market Movers (December 30, 2024)

Stocks Surge and Slide: Midday Market Movers (December 30, 2024)

Jim Cramer Warns End of 'Magical' Investing Era

Jim Cramer Warns End of 'Magical' Investing Era

Record Cash Holdings: Americans Sit on $12 Trillion, a Potential Market Warning

Record Cash Holdings: Americans Sit on $12 Trillion, a Potential Market Warning

AGF Investments Announces ETF Final Distributions for 2024/2025

AGF Investments Announces ETF Final Distributions for 2024/2025

PayPal Poised for a Comeback: Why Investors Might Be Missing Out

PayPal Poised for a Comeback: Why Investors Might Be Missing Out

Tesla Stock in 2025: Could $1,000 Grow Significantly?

Tesla Stock in 2025: Could $1,000 Grow Significantly?

Nvidia Receives $5 Billion Investment from Intel, Solidifying AI Partnership

Nvidia Receives $5 Billion Investment from Intel, Solidifying AI Partnership

Wall Street Bullish: U.S. Stocks Forecasted for Optimism in 2024

Wall Street Bullish: U.S. Stocks Forecasted for Optimism in 2024

Rupeezys: Simplifying Investing for Indian Retail Investors

Rupeezys: Simplifying Investing for Indian Retail Investors

Eaton Corporation: Growth Story Meets Valuation Concerns

Eaton Corporation: Growth Story Meets Valuation Concerns

Decoding Buffett & Munger's Investing Secrets: A Deep Dive

Decoding Buffett & Munger's Investing Secrets: A Deep Dive

Understanding Beta: A Key Metric for Investment Risk

Understanding Beta: A Key Metric for Investment Risk

Analyst Picks: Top PSU Stocks for Potential Gains

Analyst Picks: Top PSU Stocks for Potential Gains

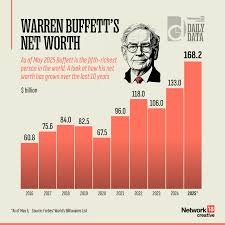

Berkshire Hathaway: A History of Wealth Creation

Berkshire Hathaway: A History of Wealth Creation

AI Investors Acknowledge Bubble, Yet Pour in Capital

AI Investors Acknowledge Bubble, Yet Pour in Capital

Is Nvidia Undervalued? Analyst Claims Stock is Cheaper Than Competitors

Is Nvidia Undervalued? Analyst Claims Stock is Cheaper Than Competitors

Jim Cramer's 2024 Investment Guide: AI, Value, and Selective Risk-Taking

Jim Cramer's 2024 Investment Guide: AI, Value, and Selective Risk-Taking

Wall Street Unanimously Forecasts Stock Market Rally - But Wait Until 2026

Wall Street Unanimously Forecasts Stock Market Rally - But Wait Until 2026

Wall Street Predicts Stock Market Rally - But Not Until 2026

Wall Street Predicts Stock Market Rally - But Not Until 2026

Investor Calls Microsoft His 'Forever Stock' - Here's Why

Investor Calls Microsoft His 'Forever Stock' - Here's Why

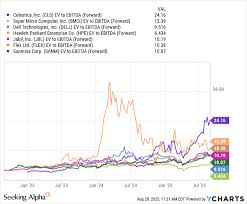

Celestica: Quiet Compounder Delivering Outperformance

Celestica: A Quiet Compounder Delivering Outperformance – And Still Room to Grow

Celestica (CLS) isn’t a name that typically dominates headlines, but for investors seeking consistent growth and value, it's quietly been delivering impressive results. Seeking Alpha contributor Kyle Tetting recently shared his experience with the company in an article titled "I've 3xed My Investment But I'm Still Buying More," highlighting its compelling investment thesis and continued potential. This analysis dives into why Celestica is a compelling opportunity, examining its business model, recent performance, future prospects, and risks.

What Does Celestica Do? A Niche in Outsourced Manufacturing

Celestica isn’t a consumer-facing brand; it's an electronics manufacturing services (EMS) provider. Essentially, they design, manufacture, and distribute electronic products for other companies – acting as a crucial behind-the-scenes partner. They don't create the technology themselves, but they build it to their clients' specifications. This outsourcing model is driven by several factors: OEMs (Original Equipment Manufacturers) often prefer to focus on core competencies like design and marketing while offloading manufacturing to specialists like Celestica to reduce costs, improve efficiency, and gain access to specialized expertise.

Celestica operates across two segments: Technology Solutions and Industrial Solutions. The Technology Solutions segment serves the communications, aerospace & defense, industrial, medical, and automotive sectors with complex, higher-margin products. The Industrial Solutions segment focuses on more standardized manufacturing for a broader range of industries, including consumer electronics and networking equipment. This diversification helps mitigate risk associated with reliance on any single industry or customer.

A History of Transformation and Value Creation

Kyle Tetting’s personal investment journey began several years ago when Celestica was undergoing a significant transformation. The company had previously been burdened by legacy businesses and underperformance. However, management initiated a strategic shift focusing on higher-growth, higher-margin areas and divesting non-core assets. This involved shedding the global component business in 2017 (a move that significantly improved profitability) and concentrating on integrated manufacturing services.

This restructuring, combined with favorable industry trends – increased outsourcing of electronics manufacturing and a surge in demand for specialized electronic products – has fueled Celestica’s impressive performance. Tetting notes he's seen his investment triple, demonstrating the power of identifying and investing in companies undergoing positive change.

Recent Performance & Financial Highlights:

The Seeking Alpha article highlights several key financial metrics that underscore Celestica’s strength:

- Strong Order Book: Celestica consistently reports a robust backlog of orders, indicating strong demand for its services. This provides visibility into future revenue and helps manage capacity planning.

- Improving Margins: The shift towards higher-margin Technology Solutions work has steadily improved operating margins. They've demonstrated an ability to price their services effectively due to the specialized nature of their offerings.

- Healthy Free Cash Flow Generation: Celestica consistently generates significant free cash flow, allowing for reinvestment in the business (R&D, capacity expansion) and returning capital to shareholders through dividends and share buybacks. This is a critical indicator of financial health and sustainability.

- Disciplined Capital Allocation: Management has demonstrated a commitment to using capital efficiently – prioritizing strategic acquisitions that complement existing capabilities and returning excess cash to investors.

Future Growth Drivers & Opportunities

The investment thesis for Celestica isn’t solely based on past performance; several factors point towards continued growth:

- Aerospace & Defense Spending: Increased global defense spending, particularly in North America and Europe, is a significant tailwind for the Technology Solutions segment. Celestica's expertise in building complex systems for this sector positions them to benefit directly.

- Automotive Electrification: The transition to electric vehicles (EVs) requires significantly more electronics than traditional internal combustion engine vehicles. Celestica’s capabilities in power management, battery technology integration, and advanced driver-assistance systems (ADAS) make it a key partner for automotive OEMs.

- 5G Infrastructure Buildout: The ongoing deployment of 5G networks globally creates demand for specialized electronic components and infrastructure equipment, which Celestica supports.

- Reshoring/Nearshoring Trends: Geopolitical tensions and supply chain disruptions are driving companies to reconsider their manufacturing locations, with a trend towards reshoring (bringing production back to domestic markets) or nearshoring (relocating production closer to home). This could benefit Celestica's North American operations.

- Continued Outsourcing Trend: The general trend of OEMs outsourcing manufacturing is expected to continue as companies seek to optimize costs and focus on core competencies.

Risks & Considerations

While the outlook for Celestica appears positive, several risks warrant consideration:

- Customer Concentration: Although Celestica has diversified its customer base, reliance on a few key accounts remains a potential risk. Loss of a major client could negatively impact revenue.

- Macroeconomic Slowdown: A global economic recession or slowdown would likely dampen demand for electronics manufacturing services across all sectors.

- Supply Chain Disruptions: While Celestica has worked to mitigate supply chain issues, continued disruptions impacting component availability and logistics could affect production schedules and costs.

- Competition: The EMS industry is competitive, with larger players like Foxconn and Jabil vying for business. Celestica must continue to innovate and differentiate itself to maintain its market position.

- Currency Fluctuations: As a global company, Celestica's earnings are exposed to currency fluctuations which can impact reported results.

Conclusion: A Compelling Value Play with Upside Potential

Celestica represents a compelling investment opportunity for those seeking a stable and growing value stock. The company’s strategic transformation, strong financial performance, and favorable industry trends create a solid foundation for continued success. While risks exist, the potential rewards – driven by secular growth trends in key sectors – appear to outweigh them. Kyle Tetting's experience underscores the power of identifying companies like Celestica that are quietly compounding value over time, making it a worthwhile addition to many investors’ portfolios. The company’s relative obscurity also means its valuation may be overlooked by some, potentially providing further upside as awareness grows.

Read the Full Seeking Alpha Article at:

[ https://seekingalpha.com/article/4856337-celestica-ive-3xed-my-investment-but-im-still-buying-more ]

Medtronic: A Defensive Gem in Uncertain Times

Medtronic: A Defensive Gem in Uncertain Times

Amazon's Business Mosaic: Retail, AWS, and Emerging Frontiers Drive Growth

Amazon's Business Mosaic: Retail, AWS, and Emerging Frontiers Drive Growth

Western Digital Stands Out as a Long-Term Buy for Data-Driven Investors

Western Digital Stands Out as a Long-Term Buy for Data-Driven Investors

Vision Investing: Cirrus Logic's Strategic Trajectory

Vision Investing: Cirrus Logic's Strategic Trajectory

A Deep Dive Into Cava: Why Growth-Stock Investors Are Dividing

A Deep Dive Into Cava: Why Growth-Stock Investors Are Dividing

Celestica's Risk/Reward Profile Remains Unconvincing

Celestica's Risk/Reward Profile Remains Unconvincing

Procter & Gamble Faces Modest Growth Outlook Amid Overvaluation Concerns

Procter & Gamble Faces Modest Growth Outlook Amid Overvaluation Concerns

Apple: The Growth Stock That Earned My Gratitude

Apple: The Growth Stock That Earned My Gratitude

Amazon Stock: 2-Minute Strong Buy Analysis

Amazon Stock: 2-Minute Strong Buy Analysis

Marvell's Networking Dominance: 45% of Revenue Drives Growth

Marvell's Networking Dominance: 45% of Revenue Drives Growth