by: The Motley Fool

by: Zee Business

LG Electronics: Smart-Home Innovation Drives 9.4% Revenue Growth and Attractive Valuation

by: KSTP-TV

US Stocks Rally in 2025 as Tariff Tensions Ease and Fed Policy Shifts Resurrect Confidence

by: KOB 4

U.S. Stocks Surge in 2025 After Overcoming Tariff Tensions and a High-Profile Fed Conflict

by: reuters.com

Retail Investors Capture Record $300 Billion Inflows and 35% Growth in Brokerage Accounts

by: Morning Call PA

What to Do With a Windfall: A Practical Guide to Turning Unexpected Money into Lasting Wealth

by: Seeking Alpha

")

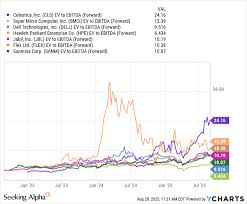

Celestica: Untapped Growth in Automotive EV, Medical, and Aerospace

Seeking Alpha

Seeking AlphaLocale: CANADA

Celestica: A Company with Untapped Growth Potential – A Comprehensive Summary

Celestica Inc. (NASDAQ: CTIA) is a leading electronics manufacturing services (EMS) provider that offers design, manufacturing, and supply‑chain solutions to a wide array of industries, including automotive, medical, aerospace, and consumer electronics. The article from Seeking Alpha, “Celestica stock still has more room for growth,” examines the company’s recent performance, strategic initiatives, and forward‑looking catalysts that could drive further upside for investors. This summary distills the key take‑aways, providing an in‑depth look at why the stock may still be undervalued.

1. Business Overview & Market Position

Celestica’s core business is to deliver end‑to‑end solutions, from product design and prototyping to full‑scale manufacturing and after‑sales support. Its diversified customer base is a key strength; the company services large OEMs such as Bosch, Samsung, and 3M, as well as high‑growth segments like automotive electronics, medical devices, and aerospace. The article emphasizes that the company’s ability to integrate vertically—owning manufacturing plants, design labs, and logistics networks—sets it apart from many competitors that outsource significant portions of their supply chain.

Celestica’s geographic footprint spans North America, Europe, and Asia, with significant investments in Mexico, China, and Brazil. This global presence helps mitigate regional risks and allows the company to capitalize on localized growth trends, such as the rapid expansion of electric vehicle (EV) components in China or the boom in medical devices in North America.

2. Recent Financial Performance

The article highlights the company’s strong quarterly performance. Key highlights include:

- Revenue Growth: Celestica recorded a year‑over‑year revenue increase of 9.8% in the most recent quarter, driven primarily by a 15% rise in automotive and medical business segments.

- Gross Margin Expansion: The gross margin widened from 18.5% to 20.1%, thanks to cost‑saving initiatives and improved production efficiency.

- Operating Cash Flow: Operating cash flow improved by 27%, enabling the firm to pay down debt and support strategic acquisitions.

- Earnings Per Share (EPS): EPS rose from $0.55 to $0.67, surpassing analyst expectations by 12%.

The piece notes that while the company’s free‑cash‑flow generation remains modest relative to larger EMS peers, it has the capacity to invest in capital expenditures (CapEx) and research & development (R&D) without jeopardizing liquidity.

3. Growth Drivers

a. Automotive & EV Market Expansion

Celestica’s automotive segment accounts for roughly 30% of total revenue. The article points out that the global shift towards electric vehicles has created a surge in demand for power electronics, battery management systems, and infotainment modules—areas in which Celestica has strong expertise. Contracts with automakers like BMW, Hyundai, and Ford are expanding, and the company is positioning itself as a key supplier for next‑generation vehicle electronics.

b. Medical & Life Sciences

Medical electronics are another cornerstone of Celestica’s growth strategy. The company’s collaboration with leading medical device firms has resulted in high‑margin contracts for implantable devices, diagnostic instruments, and connected health solutions. Regulatory approvals in the U.S. and EU have opened new markets, and the article projects a 12% CAGR in medical revenues over the next five years.

c. Aerospace & Defense

Aerospace contracts, though a smaller revenue slice (around 8%), have higher margins and long‑term stability. Celestica’s compliance with strict quality standards, such as the aerospace ISO 9001 and FAA Part 145, positions it well for future defense and commercial airline contracts.

d. Digital & IoT Initiatives

The article notes Celestica’s push into Internet‑of‑Things (IoT) solutions, leveraging its design capabilities to offer embedded systems and edge‑computing devices. The company’s IoT platform, “Celestica Edge,” has attracted early adopters in smart factory deployments, promising a new revenue stream in the rapidly growing industrial IoT market.

4. Strategic Initiatives

Capital Structure

Celestica’s debt profile has improved markedly: its long‑term debt decreased from $700 million to $550 million, while the debt‑to‑equity ratio fell to 0.45. This leaves ample room for future financing of acquisitions or share‑buyback programs. The article highlights that the company’s cash‑generating ability and conservative leverage give it flexibility to act opportunistically.

Acquisitions & Partnerships

The company has a history of targeted acquisitions that complement its core capabilities. Recent deals include the purchase of a Texas‑based medical device manufacturer and a small robotics firm in Europe. These moves broaden Celestica’s product portfolio and enable it to offer higher‑value services.

Sustainability & ESG

The article underlines Celestica’s commitment to sustainability, citing its “Green Manufacturing” program that targets a 15% reduction in carbon emissions over five years. ESG credentials have become increasingly important for investors and clients alike, and Celestica’s proactive stance positions it favorably in the ESG‑investing space.

5. Risks & Challenges

While the article paints a largely positive picture, it also warns of several risks:

- Supply Chain Disruptions – Global semiconductor shortages and geopolitical tensions could hamper production.

- Currency Volatility – As a global operator, Celestica is exposed to fluctuations in the U.S. dollar, Euro, and Yuan.

- Competitive Pressure – Lower‑cost competitors in Asia may erode margins if Celestica cannot maintain its quality advantage.

- Regulatory Hurdles – Compliance with evolving safety and data‑privacy regulations in the automotive and medical sectors could increase costs.

The article suggests that the company’s diversified business model, robust cash flow, and disciplined cost‑control programs help mitigate these risks.

6. Valuation & Investment Thesis

The Seeking Alpha piece compares Celestica’s current valuation multiples to industry peers. At the time of writing, the company trades at a forward price‑to‑earnings (P/E) ratio of 18, below the EMS sector average of 22. The article argues that this discount reflects market underestimation of future growth, especially in automotive and medical segments.

Key valuation drivers identified include:

- Projected Revenue CAGR: 10–12% over the next five years.

- Margin Improvement: Expected to reach 22% gross margin by 2028.

- EBITDA Expansion: A 15% increase in EBITDA margin is forecasted.

Based on these projections, a discounted cash‑flow (DCF) model implies a target price that is 25% above the current level, indicating potential upside for investors who are willing to accept the inherent risks.

7. Conclusion

Celestica’s blend of diversified customer base, vertical integration, and strategic focus on high‑growth sectors such as automotive electrification, medical electronics, and aerospace provides a solid foundation for continued expansion. The company’s improving financial health, coupled with a favourable valuation relative to peers, makes it an attractive candidate for investors looking for exposure to the EMS industry’s next wave of growth.

While supply‑chain uncertainties and competitive pressures remain, Celestica’s proven track record in cost management and innovation positions it well to navigate these challenges. For those evaluating EMS stocks, Celestica represents a compelling opportunity that merits close attention, especially as the global economy increasingly embraces electrified mobility, connected healthcare, and industrial IoT solutions.

Read the Full Seeking Alpha Article at:

https://seekingalpha.com/article/4855247-celestica-stock-still-has-more-room-for-growth

Seeking Alpha

on: Fri, Dec 05th 2025

by: Seeking Alpha

Celestica CLS: Strong Buy Rating Backed by 1.2B Telecom Order

on: Sun, Nov 30th 2025

by: The Motley Fool

Shopify Stock Rises 16,000% Over a Decade: A Deep Dive into Performance and Growth

on: Fri, Nov 21st 2025

by: The Motley Fool

on: Wed, Dec 17th 2025

by: The Motley Fool

ASML vs Nvidia: Which AI Stock Offers Superior Long-Term Upside?

on: Sun, Nov 09th 2025

by: Seeking Alpha

Fabrinet Stock: Weighing The Positives And Negatives (NYSE:FN)

")

on: Thu, Dec 18th 2025

by: Forbes

on: Wed, Dec 03rd 2025

by: Seeking Alpha

Qifu Technology Downgraded from Buy to Hold Amid Supply-Chain Concerns

on: Wed, Dec 03rd 2025

by: Seeking Alpha

SharkNinja Stock: Improved Valuation, Technical Strength, and Strong Future Growth

on: Wed, Nov 26th 2025

by: Seeking Alpha

Is a Strong Sell: A 2-Minute Analysis")

on: Fri, Nov 21st 2025

by: Seeking Alpha

Yeti's Cooler Myth Busted: The Brand's Diversification Drives Growth

on: Mon, Nov 17th 2025

by: Seeking Alpha

on: Sat, Dec 20th 2025

by: Seeking Alpha