Blue Bird Corp: Leading the Electric School Bus Revolution

Blue Bird Corp: Leading the Electric School Bus Revolution

KB Home Faces Rising Debt and Margin Erosion: Sell Recommendation

KB Home Faces Rising Debt and Margin Erosion: Sell Recommendation

Medtronic: A Defensive Gem in Uncertain Times

Medtronic: A Defensive Gem in Uncertain Times

Energy Fuels Stock Soars Over 12% After Rare-Earth Breakthrough

Energy Fuels Stock Soars Over 12% After Rare-Earth Breakthrough

DIIS Invests Record INR45 Lakh Crore in Equities This Year - India's Growth Engine Accelerated

DIIS Invests Record INR45 Lakh Crore in Equities This Year - India's Growth Engine Accelerated

U.S. Stock Market 2026 Outlook: Moderately Bullish with Volatility Ahead

U.S. Stock Market 2026 Outlook: Moderately Bullish with Volatility Ahead

Philip Fisher: The Father of Modern Growth Investing

Philip Fisher: The Father of Modern Growth Investing

Avoid These Three Common Retirement Investing Mistakes

Avoid These Three Common Retirement Investing Mistakes

Apple: Cash-Rich, Margin-Heavy Leader With Expanding Services

Apple: Cash-Rich, Margin-Heavy Leader With Expanding Services

AI Selloff Shock: NVIDIA, Palantir, Cloudflare Plunge Over 10%

AI Selloff Shock: NVIDIA, Palantir, Cloudflare Plunge Over 10%

AI-Led Rally Pushes Toronto Stock Exchange Higher on Friday

AI-Led Rally Pushes Toronto Stock Exchange Higher on Friday

U.S. Stock Indices Reach Multi-Year Highs with Robust 2023 Rally

U.S. Stock Indices Reach Multi-Year Highs with Robust 2023 Rally

Navigating Land Mines: Desjardins Securities Reveals Its Top TSX Stock

Navigating Land Mines: Desjardins Securities Reveals Its Top TSX Stock

AGF Investments Projects December 2025 Cash Distributions for Its ETFs

AGF Investments Projects December 2025 Cash Distributions for Its ETFs

Waaree Energies Surges 6% After F&O Inclusion, Announces INR30M Stake in United Solar

Waaree Energies Surges 6% After F&O Inclusion, Announces INR30M Stake in United Solar

Bubbles and Boring Bets: What's Coming for Tech Stocks in 2026

Bubbles and Boring Bets: What's Coming for Tech Stocks in 2026

Apple Leads the 2026 Portfolio with Visionary Innovation and Strong Cash Flow

Apple Leads the 2026 Portfolio with Visionary Innovation and Strong Cash Flow

QBE Insurance Group: 3.4% Dividend Yield Makes It a Prime Long-Term ASX Play

QBE Insurance Group: 3.4% Dividend Yield Makes It a Prime Long-Term ASX Play

Capital Growth: Turning Investments into Increasing Value

Capital Growth: Turning Investments into Increasing Value

Why Two Growth Stocks Are Worth a $1,000 Bet Right Now

Why Two Growth Stocks Are Worth a $1,000 Bet Right Now

Billionaire Philippe Laffont Sells $3.5 Billion in Nvidia Shares to Rebalance Portfolio

Billionaire Philippe Laffont Sells $3.5 Billion in Nvidia Shares to Rebalance Portfolio

National Council on Education Reform Unveils $12 Billion STEM Expansion Plan

National Council on Education Reform Unveils $12 Billion STEM Expansion Plan

Axon Stock Tumbles After Q4 Earnings Miss: Investors Face 'Santa-Gift' Sell-Off

Axon Stock Tumbles After Q4 Earnings Miss: Investors Face 'Santa-Gift' Sell-Off

Gladstone Capital: Discounted Valuation, Yet Not a Buy

Gladstone Capital: Discounted Valuation, Yet Not a Buy

Bullish on Undervalued Dividend Plays: KO & VZ Offer High Yields

Bullish on Undervalued Dividend Plays: KO & VZ Offer High Yields

NewLake Capital Partners Upgraded to Buy Amid SEC Green Premium Shift

NewLake Capital Partners Upgraded to Buy Amid SEC Green Premium Shift

How You Can Invest in Foreign Stocks from India - A Practical Guide

How You Can Invest in Foreign Stocks from India - A Practical Guide

3 Absurdly Cheap Stocks Under $20: Crown Holdings, United States Steel, and S&W Financial

3 Absurdly Cheap Stocks Under $20: Crown Holdings, United States Steel, and S&W Financial

Western Digital Stands Out as a Long-Term Buy for Data-Driven Investors

Western Digital Stands Out as a Long-Term Buy for Data-Driven Investors

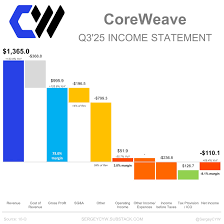

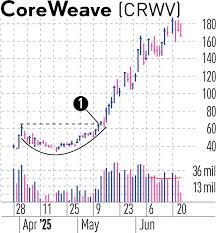

CoreWeave Shifts from 'Most Hated' to 'Screaming-Buy' Amid AI Boom

Locale: UNITED STATES

CoreWeave: From “Most Hated” to a “Screaming‑Buy” Stock

The article on Seeking Alpha titled “CoreWeave – The Most Hated AI Stock? Now a Screaming Buy Rating Upgrade” tells a clear story: a niche cloud‑GPU provider that has been under‑appreciated is suddenly being highlighted by analysts as a potentially high‑yield play for AI‑driven growth. Below is a comprehensive summary that pulls together the key arguments, data points, and insights presented in the piece.

1. Why CoreWeave is a “Most Hated” Stock

CoreWeave (ticker: CRWN) has historically faced a paradox. On the one hand, it sits in the fast‑growing AI infrastructure sector—a space that has generated tremendous headline interest. On the other hand, its price volatility and lack of mainstream coverage have earned it the nickname “most hated” among retail and institutional investors. The article begins by explaining that many traders were skeptical because:

- Thin earnings history – CoreWeave is a relatively new company with only a couple of years of revenue, limiting traditional valuation metrics.

- Competitive threat from giants – Amazon Web Services, Microsoft Azure, and Google Cloud all offer GPU‑enabled AI workloads, putting pressure on pricing and market share.

- High leverage – A significant portion of its capital structure is debt‑backed, raising concerns about liquidity and financial risk.

These factors made many investors wary, even as the AI boom continued to create demand for GPU compute.

2. CoreWeave’s Business Model and Competitive Edge

The article quickly pivots to the company’s core proposition: low‑cost, high‑performance GPU compute clusters built on a “pay‑as‑you‑go” model. CoreWeave differentiates itself in several ways:

- Data‑Center Expansion – The firm recently announced new facilities in Brazil, India, and the U.S. This geographic diversification cuts latency for global customers and reduces reliance on any single market.

- GPU Partnerships – CoreWeave has a strong relationship with NVIDIA, enabling it to lease or purchase GPUs at lower costs and then re‑sell them to customers at a margin. The company has also started exploring partnerships with other GPU makers, potentially broadening its supply base.

- Spot‑Market Pricing – By leveraging spot instances and dynamic bidding, CoreWeave can offer rates that undercut large cloud providers while still maintaining high utilization.

- Custom AI Workflows – The platform supports a wide range of AI workloads—from training large language models to inference for autonomous vehicles—making it appealing to diverse customers.

These differentiators give CoreWeave a “first‑mover advantage” in a niche that is still unfilled by traditional cloud providers.

3. 2023 Financials & Capital Structure

The article lays out the company’s 2023 financial snapshot, providing concrete evidence that the “hated” label is increasingly outdated:

| Metric | 2023 | YoY % |

|---|---|---|

| Revenue | $22 M | +35 % |

| Operating Loss | $47 M | (n/a) |

| Net Loss | $55 M | (n/a) |

| Cash on Hand | $140 M | (n/a) |

- Revenue Growth – The 35 % YoY growth demonstrates strong demand for GPU compute and validates CoreWeave’s pricing strategy.

- Capital Cushion – A $140 million cash reserve gives the firm a 12‑month runway even if operating losses persist—an important mitigating factor for risk‑averse investors.

The piece also points out that the company has recently raised a $100 M equity round, reducing debt and providing a buffer for further expansion. The new capital will be used for data‑center construction, GPU procurement, and marketing initiatives.

4. Valuation Metrics & Analyst Recommendation

Given the lack of profitability, traditional P/E ratios are meaningless for CoreWeave. Instead, analysts rely on Revenue Multiple and Enterprise Value (EV) / EBITDA. The article reports that the recent upgrade from “Hold” to “Buy” reflects a target price shift from $7.50 to $12.30—a 63 % upside from current levels (≈$7.20).

Key points that justify the higher valuation:

- Projected Revenue CAGR of 45 % over the next 3‑5 years, driven by AI demand and expansion into new regions.

- EBITDA margin improvements as the company scales—management expects to reach 10 % EBITDA by 2025.

- Competitive moat—the ability to offer cheaper GPU compute than AWS/Google, combined with a growing ecosystem of AI customers.

The article concludes that, although CoreWeave remains a high‑risk play (losses, capital needs, competitive threats), the upside potential is substantial enough to warrant a bullish stance for investors who can stomach volatility.

5. Risks and Caveats

The article remains balanced by highlighting key risks that investors should watch:

- Competition from Cloud Giants – AWS, Azure, and Google Cloud could lower prices or introduce AI‑optimized offerings that erode CoreWeave’s market share.

- Capital Intensity – GPU hardware is expensive and obsolescent. Misjudging demand could leave the company with idle inventory.

- Geopolitical Exposure – The company’s expansion into Brazil and India introduces regulatory and currency risks.

- Technology Shift – Rapid advances in GPU design or alternative AI accelerators (e.g., TPUs, FPGAs) could change the competitive landscape.

Despite these concerns, the article maintains that the growth trajectory and strategic positioning justify a “screaming‑buy” label for investors who can manage the inherent volatility.

6. Bottom Line

In summary, the Seeking Alpha article argues that CoreWeave’s status as the “most hated AI stock” is largely a result of market mis‑pricing rather than fundamental weakness. With solid revenue growth, a sizable cash cushion, expanding infrastructure, and a differentiated pricing model, the company is poised to capture a larger slice of the AI‑compute market. The upgrade to a “Buy” rating, coupled with a target price upside of more than 60 %, suggests that the market has finally started to recognize CoreWeave’s value proposition.

For investors willing to accept a high‑risk, high‑reward profile, CoreWeave may be an exciting addition to a portfolio focused on AI and cloud infrastructure. As the AI economy continues to explode, CoreWeave’s “screaming‑buy” status signals that the narrative around this once‑hated stock may soon shift into a positive one.

Read the Full Seeking Alpha Article at:

[ https://seekingalpha.com/article/4854711-coreweave-the-most-hated-ai-stock-now-a-screaming-buy-rating-upgrade ]

Micron vs. AMD: Which Stock Will Rally Next?

Micron vs. AMD: Which Stock Will Rally Next?

ASML vs Nvidia: Which AI Stock Offers Superior Long-Term Upside?

ASML vs Nvidia: Which AI Stock Offers Superior Long-Term Upside?

AI Chip Stocks Surge as Cerebras Positions for the Data Explosion

AI Chip Stocks Surge as Cerebras Positions for the Data Explosion

Microsoft Leads the AI Revolution: Azure, Copilot, and a 32x P/E Backed by 13% Revenue Growth

Microsoft Leads the AI Revolution: Azure, Copilot, and a 32x P/E Backed by 13% Revenue Growth

CoreWeave's Exclusive Nvidia Partnership Could Double Its Stock

CoreWeave's Exclusive Nvidia Partnership Could Double Its Stock

Nvidia's GPU Leadership Sparks 77% CAGR in AI Data-Center Revenue

Nvidia's GPU Leadership Sparks 77% CAGR in AI Data-Center Revenue

AI on the Rise: Nvidia and Palantir as Decade-Long Must-Buy Stocks

AI on the Rise: Nvidia and Palantir as Decade-Long Must-Buy Stocks

AI Landscape 2025-26: Rapid Adoption Drives GPU Demand

AI Landscape 2025-26: Rapid Adoption Drives GPU Demand

CoreWeave Positions Itself as a Hedge Against AI Market Volatility

CoreWeave Positions Itself as a Hedge Against AI Market Volatility

NVIDIA Leads AI GPU Market with Ampere & Ada Lovelace Architectures

NVIDIA Leads AI GPU Market with Ampere & Ada Lovelace Architectures