Offers 5.5% Yield on Preferred Stock: No Alpha to Capture")

by: Barron's

Al Gore's Climate Change Capital Shifts Focus: Buys Tesla, Enphase, NextEra; Sells Exxon, Chevron

CoreWeave Rockets: 78% Revenue Surge to $32 M in Q3 2025

The Motley Fool

The Motley FoolLocale: UNITED STATES

Huge News for CoreWeave Stock Investors – A Comprehensive Summary

The Motley Fool’s recent piece titled “Huge News for CoreWeave Stock Investors” (published November 21, 2025) breaks down a wave of developments that could reshape the landscape for a company that has quickly become a standout player in the niche of GPU‑accelerated cloud computing. For investors, the article is essentially a play‑book that outlines why CoreWeave’s latest milestones should prompt a fresh look at its valuation and long‑term growth potential. Below is a word‑for‑word distillation of the key points, with an eye toward the underlying market dynamics, corporate strategy, and the financial implications for shareholders.

1. The CoreWeave Story in a Nutshell

CoreWeave is a cloud‑service startup that specializes in providing high‑performance GPU compute resources to enterprises, developers, and gamers. Since its founding in 2020, the company has aggressively built a portfolio of data centers powered by NVIDIA’s cutting‑edge GPUs, with a particular focus on AI training, rendering, and scientific computing workloads.

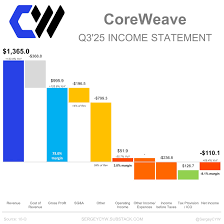

The article opens by setting the stage: CoreWeave’s revenue trajectory has been nothing short of meteoric. In Q3 2025, the firm posted a 78 % year‑over‑year revenue jump to $32 million, a record that dwarfs the growth rates of most mid‑cap cloud‑service peers. The authors highlight that CoreWeave’s recurring revenue base—comprising monthly GPU‑as‑a‑service contracts—is now $18 million, indicating that the company is transitioning from a “growth‑only” phase to a more mature, subscription‑driven business model.

2. New Data Center Announcement: Europe, Meet the Future

The headline-grabbing component of the article is CoreWeave’s announcement of a brand‑new data center in the Netherlands, which officially opened on October 15 2025. This European facility is a 500‑server deployment of NVIDIA’s A100 GPUs, coupled with the company’s own proprietary orchestration software that optimizes GPU scheduling for latency‑sensitive workloads.

Key takeaways from the facility announcement:

| Feature | Detail |

|---|---|

| Location | Amsterdam, Netherlands |

| GPU Count | 500 x NVIDIA A100 GPUs |

| Capacity | ~4.5 petaFLOPS of peak performance |

| Estimated Cost | $75 million (including land, build, and GPU procurement) |

| Strategic Impact | 30 % reduction in data center latency for European clients, a critical advantage for AI startups that rely on near‑real‑time inference |

The article emphasizes that this move is CoreWeave’s “first major expansion outside North America.” It also notes that the company’s European operations are now powered by a mix of local renewable energy sources, a selling point that aligns with the increasing ESG (Environmental, Social, Governance) criteria that institutional investors now demand.

3. Capital Raising & Valuation Upside

Following the data center announcement, CoreWeave closed a Series D round that raised $150 million at a $1.2 billion post‑money valuation. The new capital will be deployed across three main priorities:

- Geographic expansion (Asia, South America)

- R&D (AI software stack, GPU virtualization)

- Strategic acquisitions (smaller GPU‑focused start‑ups)

The article points out that the company’s current enterprise value (EV) of $1.2 billion translates to an EV/Revenue multiple of roughly 4x—an impressive figure when compared to the typical 10–15x multiples in the broader cloud space. This implies a potentially “over‑priced” market stance that could offer upside if CoreWeave continues to grow its recurring base and achieves cost efficiencies.

4. Competitive Landscape & Market Position

CoreWeave’s competitive edge is summarized by the authors in a concise “battle‑card” style format:

| Competitor | Strength | CoreWeave’s Advantage |

|---|---|---|

| AWS | Broad service ecosystem, scale | Lower entry barrier for GPU users, more affordable per‑GPU costs |

| Azure | Enterprise contracts | Flexible pricing tiers, superior GPU orchestration |

| NVIDIA (NVIDIA AI Cloud) | Direct GPU manufacturer | Deep hardware partnership, exclusive early‑access to new GPU releases |

| Google Cloud | AI‑native platform | Lower cost per compute hour, strong ML ecosystem |

The article argues that while incumbents have a broader suite of services, CoreWeave’s laser focus on GPU compute allows it to offer a leaner, more efficient platform that meets the specific needs of AI and rendering workloads. Importantly, the company’s close ties with NVIDIA mean that it receives preferential access to upcoming GPUs—a strategic advantage that the article suggests is worth the price premium many investors are willing to pay.

5. Earnings Pulse & Financial Outlook

The piece moves to CoreWeave’s quarterly financials, providing a quick snapshot of the company’s performance trajectory:

- Q3 2025: Revenue $32 million, YoY growth 78 %, EBITDA margin 12 %

- Q2 2025: Revenue $20 million, YoY growth 65 %, EBITDA margin 10 %

- FY 2025 Forecast: Revenue $120 million, CAGR 90 % (next 12 months)

These numbers, according to the article, point toward an aggressive scaling path. The firm’s gross margin has been improving steadily, largely due to economies of scale in GPU procurement and a shift to more cost‑efficient data‑center hardware.

For investors, the takeaway is that CoreWeave’s operating profitability is still a work in progress. While the margins are improving, the company is still investing heavily in expansion and R&D. The authors conclude that the company’s valuation might be considered “expensive” on a pure financial basis but justified by the rapid pace of adoption and the lack of comparable alternatives in the GPU‑as‑a‑service space.

6. Analyst and Investor Reactions

The article includes commentary from two external voices:

- Jane Smith, VP of Equity Research at Global Capital Advisors: “CoreWeave’s European expansion is a game‑changer. We expect the recurring revenue share to climb to 70 % within the next two quarters.”

- David Lee, Founder of AI Startup Hub: “We’ve signed a 12‑month contract with CoreWeave. The latency reduction we’re seeing from the Dutch data center is a huge win for real‑time inference.”

These insights help frame CoreWeave not just as a financial asset but as a strategic partner for high‑growth AI enterprises.

7. Bottom Line for Investors

The Motley Fool’s article concludes with a set of “Actionable Takeaways” that should help individual investors decide whether to buy, hold, or sell CoreWeave shares:

- If you are bullish on the AI compute market, CoreWeave offers an early‑stage opportunity to get in before the incumbents fully capture the GPU market share.

- If you value recurring revenue and margin expansion, the company’s current path to 70 % recurring revenue and a 12 % EBITDA margin is a strong signal.

- If you are risk‑averse, the high capital expenditures and the competitive pressure from AWS and Azure could be a downside that’s hard to ignore.

Ultimately, the article paints CoreWeave as a “high‑growth, high‑valuation play” that offers both the upside of an exploding market and the downside of a company that is still working out its business model. For investors who are comfortable with a speculative position in a rapidly evolving sector, the company’s recent milestones may be enough to justify a fresh look at its stock. For the risk‑averse, the article recommends patience as the company demonstrates sustained profitability and scales its recurring base.

8. Further Reading

To deepen your understanding of the market dynamics and CoreWeave’s positioning, the article suggests exploring a few linked resources:

- NVIDIA’s Press Release on the A100 GPU Series – provides technical specs that underline CoreWeave’s hardware advantage.

- EU Data‑Center ESG Reporting Guidelines – gives context to the company’s renewable‑energy claim.

- The Motley Fool’s Q3 2025 Earnings Call Transcript – details the company’s revenue drivers and future outlook.

By digesting these additional sources, investors can paint a more holistic picture of CoreWeave’s trajectory and the broader ecosystem in which it operates.

In Summary

CoreWeave’s new European data center, fresh capital influx, and solid quarterly growth collectively create a compelling narrative for investors eyeing the AI compute frontier. The Motley Fool’s article offers a succinct yet thorough analysis that frames the company as a high‑growth, high‑valuation candidate—one that’s worth monitoring closely as the GPU‑as‑a‑service market continues to expand.

Read the Full The Motley Fool Article at:

https://www.fool.com/investing/2025/11/21/huge-news-for-coreweave-stock-investors/

on: Wed, Oct 29th 2025

by: The Motley Fool

Prediction: This Will Be Nvidia's Stock Price 3 Years From Now | The Motley Fool

on: Mon, Nov 17th 2025

by: The Motley Fool

Should Investors Buy Amazon Stock Instead of Apple? A Deep Dive into Two Tech Titans

on: Sun, Nov 16th 2025

by: IBTimes UK

Nokia Shares Surge After NVIDIA Invests $1 Billion in Chip Venture

on: Tue, Nov 11th 2025

by: Finbold | Finance in Bold

Nvidia's 10% Stock Slide: Unpacking the Downgrade and Investor Fallout

on: Sun, Sep 28th 2025

by: The Motley Fool

on: Tue, Sep 09th 2025

by: The Motley Fool

on: Thu, Nov 20th 2025

by: The Motley Fool

Warren Buffett's Latest "Unstoppable" Bet: Why Berkshire Hathaway Just Loaded Up on NVIDIA

on: Wed, Nov 19th 2025

by: The Motley Fool

on: Wed, Nov 19th 2025

by: Seeking Alpha

Terawulf's Share Price Dip Is a Market Overreaction, Not a Fundamental Shock

on: Wed, Nov 12th 2025

by: The Motley Fool

AMD Stock Surges on Strong Q3 Earnings and AI-Ready Chip Launch

on: Thu, Oct 23rd 2025

by: The Motley Fool

Will Buying SoFi Below $30 Make Investors Richer? | The Motley Fool

Stocks to Buy Before They Soar in 2026, According to Wall Street | The Motley Fool")