Two Harbors Faces Erosion of Book Value

Locales: California, Texas, New York, UNITED STATES

The Erosion of Book Value: More Than Just a Slowdown

The company's book value per share growth over the past year has been lackluster, a significant departure from previous periods of robust expansion. While acknowledging some positive investment returns, these have been consistently undermined by escalating hedging costs and the pervasive impact of a rising interest rate environment. This isn't simply a case of moderate deceleration; it signals a fundamental challenge in generating sustainable value. The underlying problem isn't necessarily lack of return, but rather a diminishing return after accounting for the costs of maintaining the portfolio and mitigating risk. A key question investors should ask is whether Two Harbors can adapt its investment strategy to generate sufficient returns to overcome these headwinds.

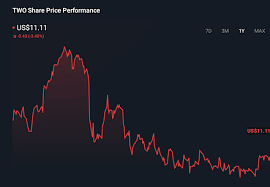

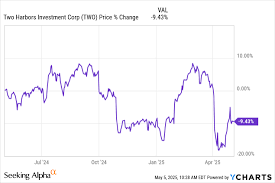

Earnings Failures: A Symptom of Deeper Issues The most recent earnings report delivered a clear message: Two Harbors is struggling to meet expectations. The reported earnings per share fell short of analyst consensus, and forward-looking guidance painted a cautious - some might say pessimistic - picture. This isn't an isolated incident, but rather a continuation of a pattern. While many REITs experienced some volatility in 2024, Two Harbors' performance has lagged behind its peers. This suggests that the challenges facing the company are not merely cyclical, but structural in nature. It begs the question: is the current operational model still fit for purpose?

Hedging Ineffectiveness: A Costly Shield

Two Harbors relies heavily on hedging strategies to shield its portfolio from adverse interest rate movements. However, recent evidence suggests these strategies are losing their effectiveness. The costs associated with hedging have surged, creating a significant drag on earnings. This could be attributed to a number of factors, including increased market volatility and the complexities of navigating a rapidly changing interest rate landscape. The efficacy of hedging isn't just about if it works, but how much it costs to implement. If the cost of protection outweighs the potential benefit, it's essentially a losing proposition. Investors should scrutinize the specifics of Two Harbors' hedging portfolio and assess its true cost-effectiveness.

Interest Rate Exposure: A Persistent Vulnerability

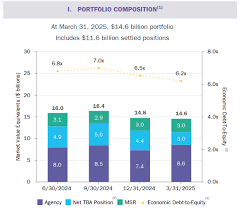

The inherent sensitivity of mortgage REITs to interest rate fluctuations is well-documented. Rising rates diminish the value of mortgage-backed securities and increase borrowing expenses. Two Harbors has attempted to mitigate this risk through various measures, but its vulnerability remains substantial. The Federal Reserve's hawkish stance in late 2025 and projected continuation into 2026 makes this a particularly pressing concern. While diversification into different mortgage types can help, it's unlikely to fully insulate the company from the impact of higher rates. The REIT's debt structure also plays a critical role; high levels of leverage amplify the negative effects of rising rates.

Valuation Disconnect: Premium Not Justified

Despite these challenges, Two Harbors continues to trade at a premium to its book value. This premium is predicated on the expectation of future growth, a belief that appears increasingly unfounded given the company's recent performance. The market seems to be pricing in a turnaround that isn't demonstrably materializing. A more realistic assessment of the company's prospects warrants a downward revision of its valuation. Furthermore, comparing Two Harbors' price-to-book ratio with those of its competitors reveals a significant discrepancy, highlighting the potential for overvaluation.

Looking Ahead: A Call for Re-evaluation

Two Harbors Investment Group is navigating a difficult environment. Tepid book value growth, underwhelming earnings, and heightened interest rate sensitivity represent significant headwinds. While the company has implemented strategies to address these challenges, their effectiveness remains questionable. A downgrade, therefore, is not merely warranted, but necessary. Investors should carefully reassess their positions in TWO, taking into account the evolving dynamics of the mortgage REIT sector and the company's specific vulnerabilities. A proactive approach to risk management is crucial in the current economic climate. The future of Two Harbors will depend on its ability to adapt, innovate, and generate sustainable returns in a challenging environment. The company needs to demonstrate a clear path to restoring book value growth and regaining investor confidence.

Disclaimer: I am not a financial advisor. This is not financial advice. Please consult with a qualified financial advisor before making any investment decisions.

Read the Full Seeking Alpha Article at:

[ https://seekingalpha.com/article/4865370-two-harbors-tepid-book-value-growth-underwhelming-earnings-downgrade ]