Tech Titans: Amazon, Nvidia, AMD, and TSM Dominate Evercore ISI's Picks

Tech Titans: Amazon, Nvidia, AMD, and TSM Dominate Evercore ISI's Picks

PayPal Faces Uncertainty as 2026 Begins

PayPal Faces Uncertainty as 2026 Begins

Citadel Shifts Investments: Amazon Down, Palantir Up

Citadel Shifts Investments: Amazon Down, Palantir Up

Berkshire Hathaway Outperforms S&P 500 Significantly Since 1965

Berkshire Hathaway Outperforms S&P 500 Significantly Since 1965

Nvidia: AI Growth Reliance Creates Risk

Nvidia: AI Growth Reliance Creates Risk

Gokaldas Exports Shares Plummet 95%, Hit 28-Month Low

Gokaldas Exports Shares Plummet 95%, Hit 28-Month Low

Groww Launches New Small-Cap Mutual Fund

Groww Launches New Small-Cap Mutual Fund

Balaji Amines Shares Surge 10% on Strong Q3 Results

Balaji Amines Shares Surge 10% on Strong Q3 Results

Small-Cap Stocks Lead 2024 Market Rally

Small-Cap Stocks Lead 2024 Market Rally

Trump Proposes $5M CEO Pay Cap for Defense Contractors to Boost Production

Trump Proposes $5M CEO Pay Cap for Defense Contractors to Boost Production

Karma Investing: A Contrarian Strategy for Market Profits

Karma Investing: A Contrarian Strategy for Market Profits

AK Lauren's 2024-2026 Investment Strategy: A $300,000 Portfolio

AK Lauren's 2024-2026 Investment Strategy: A $300,000 Portfolio

Bank of America Predicts 2026 Economic Boom: 'Run It Hot' Scenario

Bank of America Predicts 2026 Economic Boom: 'Run It Hot' Scenario

RKLB's 2025 Rollercoaster: A Deep Dive into Remarkable Logistics' Struggles

RKLB's 2025 Rollercoaster: A Deep Dive into Remarkable Logistics' Struggles

Stockdale Capital Partners Diversifies Beyond Distressed Retail

Stockdale Capital Partners Diversifies Beyond Distressed Retail

Albemarle (ALB) Poised for Gains: Analysts Predict Lithium Rally in 2026

Albemarle (ALB) Poised for Gains: Analysts Predict Lithium Rally in 2026

JPMorgan Upgrade Drives Tata Elxsi & Tata Technologies Shares Higher

JPMorgan Upgrade Drives Tata Elxsi & Tata Technologies Shares Higher

90% of Investors Plan to Hold AI Stocks by 2026: Survey Reveals AI Investment Rush

90% of Investors Plan to Hold AI Stocks by 2026: Survey Reveals AI Investment Rush

Quantum Computing Stocks to Watch in 2026: IonQ, Rigetti, and IBM

Quantum Computing Stocks to Watch in 2026: IonQ, Rigetti, and IBM

Motley Fool Highlights Nvidia and ASML as Long-Term Growth Stocks

Motley Fool Highlights Nvidia and ASML as Long-Term Growth Stocks

Goldman Sachs Reveals Top Stock Picks for 2026

Goldman Sachs Reveals Top Stock Picks for 2026

S&P 500 & Dow Jones Hit Record Highs Amidst Rally

S&P 500 & Dow Jones Hit Record Highs Amidst Rally

2026 Market Outlook: Transformative Year Ahead

2026 Market Outlook: Transformative Year Ahead

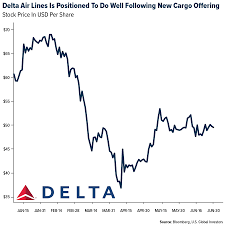

Delta Airlines Stock Faces Investor Concerns Amidst Industry Headwinds

Delta Airlines Stock Faces Investor Concerns Amidst Industry Headwinds

Mobile Payment Worldwide (MPWR): Potential Buy Opportunity Explored

Mobile Payment Worldwide (MPWR): Potential Buy Opportunity Explored

Amazon (AMZN) Stock: A 2026 Investment Outlook

Locale: UNITED STATES

Is Amazon Still a Buy in 2026? A Deep Dive into the E-Commerce and Cloud Giant

The Motley Fool article from January 7, 2026, titled “Is Amazon Stock a Buy for 2026?” paints a largely optimistic picture for the tech behemoth, arguing that despite significant growth already achieved, Amazon (AMZN) remains a compelling investment opportunity. The core thesis revolves around the enduring strength of its core businesses – e-commerce and cloud computing (AWS) – coupled with promising expansions into new, high-growth areas like advertising, healthcare, and potentially even space exploration. However, the article doesn’t shy away from acknowledging the challenges, including increased competition and macroeconomic uncertainties. Here's a comprehensive summary of the key arguments and considerations presented:

Dominating E-Commerce – But Evolving with the Times

The article acknowledges that Amazon’s dominance in e-commerce isn’t a given forever. Competition from players like Walmart, Shopify, and Temu is intensifying, forcing Amazon to innovate and adapt. However, the Fool argues Amazon isn’t simply focused on maintaining market share; it’s actively transforming how e-commerce operates.

The article highlights several key strategies: the continued rollout of faster, cheaper delivery options – fueled by its extensive logistics network (and increasingly, drone delivery as evidenced by the linked article on Amazon’s drone initiative) – and the expansion of its Prime membership program. Prime isn’t just about free shipping anymore; it's becoming an entertainment and service hub. Streaming services (Prime Video), grocery delivery (Whole Foods and Amazon Fresh), and even prescription drug delivery (Amazon Pharmacy) are all bundled into the membership, increasing stickiness and driving recurring revenue. The increasing focus on “Just Walk Out” technology in physical stores is also presented as a long-term play to revolutionize the retail experience.

Importantly, the article points out Amazon’s shift towards third-party sellers. While competing with these sellers, Amazon also benefits from their presence, expanding product selection and generating commissions. This duality is a key feature of its business model.

AWS Remains the Growth Engine

While e-commerce is often the first thing people associate with Amazon, the article emphasizes that Amazon Web Services (AWS) is the primary driver of profitability and a significant source of future growth. The cloud computing market continues to expand rapidly, and AWS remains the clear market leader, despite challenges from Microsoft Azure and Google Cloud.

The article dives into AWS’s diversifying services beyond basic computing power. Artificial intelligence (AI) and machine learning (ML) are becoming central to AWS's offerings, providing tools and infrastructure for businesses to develop and deploy AI applications. This, coupled with specialized services for industries like healthcare and finance, positions AWS as more than just a commodity provider. The expansion of data centers globally, including investments in renewable energy to power them, is also highlighted as a commitment to long-term sustainability and growth.

Beyond the Core: Diversification into High-Growth Markets

The Fool stresses Amazon’s willingness to experiment and invest in new ventures. This is a critical part of its long-term strategy. Key areas highlighted include:

- Advertising: Amazon’s advertising business is growing at an impressive rate, leveraging its vast customer data and reach. The article suggests that advertising could eventually rival AWS in terms of revenue contribution.

- Healthcare: Amazon’s acquisition of One Medical and its foray into virtual care are seen as a potential game-changer in the healthcare industry. Disrupting the traditionally fragmented healthcare system is a massive opportunity, but also carries significant regulatory hurdles.

- Space Exploration (Project Kuiper): While still in its early stages, Project Kuiper – Amazon's satellite internet constellation – is presented as a high-risk, high-reward endeavor. Providing affordable internet access to underserved areas could unlock new markets and revenue streams, but faces competition from SpaceX’s Starlink.

- Grocery: The continued integration and expansion of Whole Foods and Amazon Fresh, coupled with innovations like cashierless checkout, aims to solidify Amazon’s position in the grocery market.

Risks and Considerations

The article isn’t entirely bullish. It acknowledges several risks:

- Competition: Increased competition across all its major segments presents a constant challenge. Maintaining market share will require continued innovation and aggressive pricing.

- Regulatory Scrutiny: Amazon's size and market power have attracted increased scrutiny from regulators, potentially leading to antitrust investigations and stricter regulations.

- Macroeconomic Factors: Economic downturns can impact consumer spending and business investment, affecting both e-commerce and AWS revenue. The article notes that higher interest rates could also slow down Amazon’s investment in new projects.

- Execution Risk: Expanding into new markets like healthcare and space exploration is inherently risky. Successfully navigating these challenges requires strong execution and a willingness to adapt.

The Verdict: A Buy, with Caveats

Ultimately, the Motley Fool article concludes that Amazon remains a buy for 2026. The company’s strong fundamentals, diversification strategy, and commitment to innovation outweigh the risks. However, the article emphasizes that Amazon is not a “set it and forget it” investment. Investors should be aware of the challenges and monitor the company’s performance closely. The price, even after recent gains, is deemed reasonable given Amazon's growth potential. The article suggests that patient, long-term investors are most likely to be rewarded. The key takeaway is that Amazon isn’t just an e-commerce company anymore; it’s a diversified technology conglomerate with the potential to shape the future of multiple industries.

Read the Full The Motley Fool Article at:

[ https://www.fool.com/investing/2026/01/07/is-amazon-stock-a-buy-for-2026/ ]

Amazon's Stock: Where Could It Be in Three Years?

Amazon's Stock: Where Could It Be in Three Years?

Is Amazon Stock Still a Buy After Record Gains?

Is Amazon Stock Still a Buy After Record Gains?

Amazon 2026 Outlook: Diversified Growth Engine Drives Buy Call

Amazon 2026 Outlook: Diversified Growth Engine Drives Buy Call

Amazon's Business Mosaic: Retail, AWS, and Emerging Frontiers Drive Growth

Amazon's Business Mosaic: Retail, AWS, and Emerging Frontiers Drive Growth

Lyft's 2026 Outlook: EV Adoption & Autonomous Break-Even

Lyft's 2026 Outlook: EV Adoption & Autonomous Break-Even

Shopify Stock Rises 16,000% Over a Decade: A Deep Dive into Performance and Growth

Shopify Stock Rises 16,000% Over a Decade: A Deep Dive into Performance and Growth

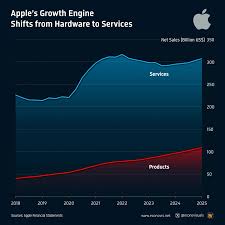

Apple Drives Growth with Services, Wearables, and AR Innovations

Apple Drives Growth with Services, Wearables, and AR Innovations

Amazon Stock: 2-Minute Strong Buy Analysis

Amazon Stock: 2-Minute Strong Buy Analysis