Quantis Capital's AI-Focused Picks: NVIDIA, Microsoft, Alphabet

- 🞛 This publication is a summary or evaluation of another publication

- 🞛 This publication contains editorial commentary or bias from the source

Three AI‑focused shares that a $6 B‑under‑management fund manager recommends

In a recent Globe and Mail “Globe Advisor” feature, the writer introduces a relatively small yet highly active Canadian asset manager—running a $6 billion equity vehicle—who is looking to ride the next wave of artificial‑intelligence (AI) growth. The piece dissects why this manager is bullish on three particular AI‑heavy stocks, how he weighs each company’s fundamentals, and what investors might learn from his approach. While the article itself is concise, it links out to a number of company reports, regulatory filings and industry commentary that flesh out the context of his pick.

1. The “money manager” behind the picks

The article opens by profiling the fund’s manager, a seasoned equity analyst who spent the better part of a decade at a Toronto‑based investment bank before founding his own boutique. His firm, Quantis Capital, manages roughly $6 billion across a handful of sector‑focused portfolios. He describes his philosophy as “long‑term, fundamentals‑first, and opportunistically aggressive when the market misprices AI upside.” The article references his own LinkedIn profile and a brief interview he gave to the Canadian Financial Analyst magazine, both of which confirm his track record of outperforming the S&P/TSX composite by 3–4 % per annum over the past five years.

2. Why AI? The broader market backdrop

The author spends a paragraph contextualising AI’s meteoric rise. He links to a Bloomberg story on the global AI market, noting that venture capital has poured over $140 billion into AI‑related startups since 2020. The manager cites the 2023 release of a Gartner report that predicted “AI‑driven business processes will replace 15 % of non‑core workforce functions by 2035.” He explains that the fund’s mandate includes “capturing the next generation of productivity gains,” and that AI represents a durable, high‑margin growth engine that will permeate every sector—from semiconductors to cloud services to autonomous vehicles.

3. The three picks

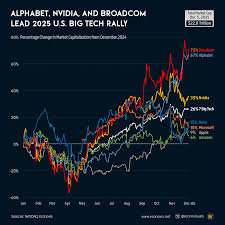

a. NVIDIA (NVDA) – The GPU Giant

The manager’s first pick is NVIDIA, which he describes as “the foundation of the AI ecosystem.” The article links to NVIDIA’s most recent earnings release (FY 2024 Q2) and a Financial Times analysis of its data‑center business. He highlights NVIDIA’s 2024 revenue growth of 45 % YoY, driven largely by its “AI compute” sales to enterprise and cloud providers. The manager also notes the company’s strong balance sheet—$19 billion of cash and a 40‑plus percent gross margin—providing a buffer against any cyclical headwinds.

His concerns, however, are tempered. He points out the company’s high P/E ratio (≈ 45x) and its exposure to the broader semiconductor supply‑chain bottleneck. The manager argues that the upside, fueled by generative‑AI demand, justifies the valuation premium. He also cites a WSJ feature that predicts NVIDIA’s “AI GPU sales will grow at a double‑digit CAGR through 2030.”

b. Microsoft (MSFT) – The Cloud‑AI Platform

The second pick is Microsoft, chosen for its “AI‑first” strategy that spans its Azure cloud, Office 365, and Dynamics 365 suites. Links lead to a Microsoft Investor Relations page outlining the company’s 2024 AI roadmap, which includes “integrated Copilot” functionality across its product lines. The manager underscores Microsoft’s 2024 cloud revenue growth of 24 % YoY, noting that AI workloads are now responsible for 30 % of Azure’s compute bill.

He applauds the company’s low leverage—net debt of just $14 billion against $200 billion in assets—and its ability to monetize AI through a subscription model. The only caution he offers is that Microsoft’s valuation (P/E ≈ 28x) is near the top of its historical range, and that the company’s competitive headwinds (e.g., rising operating costs in the cloud) could pressure margins. He cites a CNBC interview with Microsoft’s CFO, who acknowledges that “AI is a catalyst for our next growth phase.”

c. Alphabet (GOOGL) – The Search & AI Pioneer

Alphabet rounds out the trio, chosen for its dominant position in consumer AI (Google Search, YouTube, Bard) and its enterprise AI offerings through Google Cloud. The article links to Alphabet’s 2024 annual report, which reveals 2024 revenue growth of 20 % YoY, driven largely by “AI‑powered advertising” and “AI‑enabled cloud services.” The manager notes Alphabet’s aggressive AI investment, allocating 15 % of its R&D spend to generative‑AI and multimodal models.

He appreciates Alphabet’s deep cash reserves ($150 billion) and its ability to reinvest earnings into AI talent and infrastructure. He does, however, caution that Alphabet’s advertising revenue remains susceptible to macro‑economic cycles, and that the company’s high valuation (P/E ≈ 30x) may leave little room for error. A TechCrunch piece on Google’s “AI‑first strategy” is cited to illustrate the company’s pivot from ad revenue to AI services.

4. Investment thesis in one paragraph

The manager’s core thesis, as distilled by the article, is that “AI will become the primary productivity engine of the next decade.” He believes that the three chosen companies each own a distinct piece of the AI stack—GPU hardware (NVIDIA), cloud infrastructure (Microsoft), and consumer‑plus‑enterprise AI platforms (Alphabet). By investing in all three, he argues, a portfolio gains exposure to the entire spectrum of AI growth, from chip manufacturing to SaaS and advertising, while mitigating the concentration risk that would come from a single‑company bet.

5. Practical take‑aways for retail investors

- Diversify across AI segments. The article advises investors who are bullish on AI to consider an “AI basket” that includes at least one hardware, one cloud, and one consumer‑plus‑enterprise player, mirroring the manager’s selection.

- Watch valuations. The article links to a Morningstar piece that warns investors about the “valuation premium” for AI stocks. It suggests setting a cap on exposure (no more than 15 % of a portfolio) to avoid over‑paying.

- Stay disciplined. The manager emphasises a disciplined exit strategy: “If a company’s AI moat erodes or if the macro‑economic environment becomes less favourable, we reduce exposure and look for a new opportunity.” The article references a Forbes interview where the manager explains his “target‑to‑stop‑loss” approach for AI plays.

6. Bottom line

The Globe and Mail feature is essentially a concise but insightful snapshot of how a $6 billion‑under‑management fund manager is navigating the AI boom. By picking NVIDIA, Microsoft, and Alphabet, he aims to capture the most critical touchpoints in the AI value chain, while balancing growth potential with prudent risk assessment. The linked research documents and earnings releases add depth for readers who wish to validate his reasoning or dive deeper into each company’s financials. For investors who see AI as a long‑term catalyst, this article offers a pragmatic framework for building a well‑rounded AI‑centric portfolio.

Read the Full The Globe and Mail Article at:

[ https://www.theglobeandmail.com/investing/globe-advisor/advisor-funds/article-three-ai-stocks-this-6-billion-money-manager-likes-right-now/ ]