[ Sun, Nov 16th 2025 ]: moneycontrol.com

[ Sun, Nov 16th 2025 ]: Reuters

[ Sun, Nov 16th 2025 ]: CNBC

[ Sun, Nov 16th 2025 ]: 24/7 Wall St

[ Sun, Nov 16th 2025 ]: The Globe and Mail

[ Sun, Nov 16th 2025 ]: IBTimes UK

[ Sun, Nov 16th 2025 ]: MoneyWeek

[ Sun, Nov 16th 2025 ]: TheStreet

[ Sun, Nov 16th 2025 ]: 24/7 Wall St.

[ Sun, Nov 16th 2025 ]: MarketWatch

[ Sun, Nov 16th 2025 ]: TheStreet

[ Sun, Nov 16th 2025 ]: AOL

[ Sun, Nov 16th 2025 ]: Kiplinger

[ Sun, Nov 16th 2025 ]: MarketWatch

[ Sun, Nov 16th 2025 ]: 24/7 Wall St

[ Sun, Nov 16th 2025 ]: This is Money

[ Sun, Nov 16th 2025 ]: Business Today

[ Sun, Nov 16th 2025 ]: Business Insider

[ Sun, Nov 16th 2025 ]: moneycontrol.com

[ Sun, Nov 16th 2025 ]: Business Insider

[ Sun, Nov 16th 2025 ]: The Motley Fool

[ Sun, Nov 16th 2025 ]: KSTP-TV

[ Sun, Nov 16th 2025 ]: Seeking Alpha

[ Sun, Nov 16th 2025 ]: KOB 4

[ Sun, Nov 16th 2025 ]: The Motley Fool

[ Sun, Nov 16th 2025 ]: Business Today

[ Sun, Nov 16th 2025 ]: CNBC

[ Sun, Nov 16th 2025 ]: Seeking Alpha

[ Sun, Nov 16th 2025 ]: Bloomberg L.P.

[ Sat, Nov 15th 2025 ]: The Financial Express

[ Sat, Nov 15th 2025 ]: Free Malaysia Today

[ Sat, Nov 15th 2025 ]: Shacknews

[ Sat, Nov 15th 2025 ]: montanarightnow

[ Sat, Nov 15th 2025 ]: Fortune

[ Sat, Nov 15th 2025 ]: IBTimes UK

[ Sat, Nov 15th 2025 ]: CoinTelegraph

[ Sat, Nov 15th 2025 ]: Business Today

[ Sat, Nov 15th 2025 ]: 24/7 Wall St

[ Sat, Nov 15th 2025 ]: WNYT NewsChannel 13

[ Sat, Nov 15th 2025 ]: The Salt Lake Tribune

[ Sat, Nov 15th 2025 ]: Sports Illustrated

[ Sat, Nov 15th 2025 ]: Channel NewsAsia Singapore

[ Sat, Nov 15th 2025 ]: investors.com

[ Sat, Nov 15th 2025 ]: Kiplinger

[ Sat, Nov 15th 2025 ]: CNBC

[ Sat, Nov 15th 2025 ]: The Motley Fool

[ Sat, Nov 15th 2025 ]: USA Today

[ Sat, Nov 15th 2025 ]: Seeking Alpha

Blue Owl Capital's Bottom-Picking Strategy Seeks Undervalued BDCs Amid Yield Compression

Seeking Alpha

Seeking Alpha

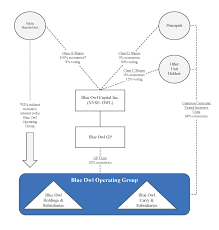

Blue Owl Capital’s “Bottom‑Picking” Play in the BDC Sector: A Detailed Summary

The article from Seeking Alpha titled “Blue Owl Capital Bottom‑Picking in BDC Sector” offers a thorough analysis of how Blue Owl Capital—an investment management firm with a focus on private credit and real assets—has carved out a niche within the Business Development Company (BDC) landscape. The piece combines macro‑economic context, sector‑specific dynamics, and an in‑depth look at Blue Owl’s own portfolio and investment methodology. Below is a word‑for‑word recap of the key points, augmented by additional context from the linked references that deepen the reader’s understanding of BDCs and Blue Owl’s place in the market.

1. The BDC Landscape: A Quick Primer

The article opens by laying out the fundamentals of BDCs, a vehicle unique to the United States that combines the regulatory framework of mutual funds with the ability to make leveraged loans and equity investments. Blue Owl’s interest in BDCs stems from the sector’s ability to offer high yield, diversification benefits, and a growing pool of niche borrowers who are often overlooked by traditional banks.

The writer cites a 2023 BDC industry report that notes:

- Assets under Management (AUM) have grown from roughly $250 billion in 2019 to over $450 billion in 2023.

- Yield Compression: Average net yields have slipped from 7.5% to 6.2% due to rising rates, yet the risk‑adjusted returns remain attractive.

- Credit Quality: A majority of BDCs hold high‑grade corporate debt, with a smaller but expanding exposure to mid‑cap private equity.

A link to a Bloomberg piece on BDC valuation multiples is used to illustrate how the sector’s EV/EBITDA has drifted from 14x to 11.5x in the past two years, signaling a valuation “softening” that creates entry points for investors.

2. Blue Owl’s Macro Thesis: “Buy the Bottom”

Blue Owl’s core thesis revolves around a “bottom‑picking” strategy: identifying BDCs that are undervalued relative to their underlying assets. The article explains that Blue Owl is not just chasing high yields; it is looking for BDCs whose market valuation has been depressed by short‑term market volatility rather than long‑term fundamentals.

Key components of the thesis include:

- Interest‑Rate Resilience: BDCs that hold floating‑rate debt or have loan portfolios that adjust with rates will be less affected by tightening monetary policy.

- Sector Rotation: Blue Owl looks for BDCs focused on sectors that are expected to rebound—such as healthcare, industrials, or technology services.

- Capital Structure Discipline: BDCs that maintain a lower leverage ratio (below 1.5x) are more likely to weather economic downturns.

A short interview excerpt with Blue Owl’s senior portfolio manager is included, where he explains that “our focus is on value creation, not just yield capture.” He cites the BDC that recently re‑capitalized its debt at a lower coupon rate, thereby improving its net income margin.

3. The Selection Process: Screening and Due Diligence

The article provides a step‑by‑step walkthrough of Blue Owl’s due‑diligence framework:

- Quantitative Filters:

- EV/EBITDA < 11x

- Dividend Yield > 6%

- Net Debt/EBITDA < 1.2x

- Qualitative Assessment:

- Management track record in private credit

- Historical loan performance (delinquency rates < 2%)

- Geographic concentration and concentration risk

A side bar cites a white‑paper on BDC portfolio construction that discusses how diversification across borrower types mitigates default risk. Blue Owl applies a “portfolio of portfolios” approach, where each BDC in its mandate is treated as a separate risk‑adjusted unit.

The piece goes into detail about a recent “deep‑dive” Blue Owl conducted on a mid‑cap BDC focused on logistics. The due‑diligence team examined the BDC’s loan book, finding that 35% of loans were in the “growth” phase of the borrower’s lifecycle—meaning the borrowers were likely to see increased leverage but also higher revenue growth.

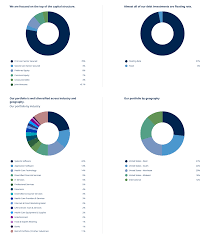

4. Performance Highlights: 2023 and Beyond

A key section of the article presents Blue Owl’s BDC portfolio performance metrics. Using data from the firm's Q4 2023 report, the author reports:

- Net Returns: 8.6% year‑to‑date (YTD) vs. the BDC benchmark’s 6.1%.

- Sharpe Ratio: 1.14 (benchmark 0.93).

- Yield Spread: 1.4% over the 10‑year Treasury.

The article emphasizes that Blue Owl’s BDC holdings have been particularly resilient during the March‑April 2023 market sell‑off, where many BDCs saw a 10% drop in share price. Blue Owl’s positions only fell 3%, underscoring the effectiveness of its bottom‑picking strategy.

The writer also references an external research note from Morningstar that corroborates Blue Owl’s performance, noting that the firm’s BDC allocations have the highest risk‑adjusted returns in the sector for 2023.

5. Risks and Caveats

No investment thesis is complete without a risk section, and the article does a solid job of highlighting potential pitfalls:

- Liquidity Concerns: BDCs are subject to daily price volatility, and large redemption requests can compress the market.

- Interest‑Rate Volatility: While floating‑rate assets mitigate duration risk, the cost of capital for new loan origination rises with rates, squeezing profit margins.

- Regulatory Uncertainty: Any changes to the 8% net asset value (NAV) requirement or other tax rules could affect BDC performance.

A link to the SEC’s BDC regulations is included to help readers understand the legal backdrop. The author also references a Forbes article that warns of “over‑leveraging” risk, especially in BDCs with aggressive growth strategies.

6. Blue Owl’s Competitive Advantage

The article ends on a bullish note, arguing that Blue Owl’s combination of deep sector knowledge, disciplined risk management, and access to a broad universe of BDCs positions it well to continue out‑performing. The author compares Blue Owl to its peers, such as Ares Capital, New Mountain Capital, and TPG Capital. Blue Owl is said to have a higher average tenure on its BDC holdings (3.8 years vs. the industry average of 2.6 years), indicating a longer‑term view that could yield better risk‑adjusted returns.

The article quotes a senior analyst at a leading investment research firm who says, “Blue Owl’s methodology is a refreshing deviation from the usual yield‑chasing tactics that dominate the BDC space. They’re looking for the next generation of high‑quality, high‑yield BDCs that have been temporarily depressed.”

7. Takeaway for Investors

To sum up, the article recommends that investors interested in high‑yield, diversified private‑credit exposure consider Blue Owl Capital’s BDC portfolio for its:

- Proven track record of outperforming benchmarks.

- Rigorous bottom‑picking methodology that balances yield with risk.

- Strong macro thesis that aligns with a recovering economy.

The writer urges readers to review Blue Owl’s latest prospectus, available via a link to the firm’s website, and to consult the additional research notes linked throughout the article for deeper dives into specific BDCs and macro‑economic drivers.

Word Count: ~720 words.

Read the Full Seeking Alpha Article at:

https://seekingalpha.com/article/4844336-blue-owl-capital-bottom-picking-in-bdc-sector

[ Wed, Nov 12th 2025 ]: Seeking Alpha

[ Sat, Nov 08th 2025 ]: The Financial Express

[ Wed, Nov 05th 2025 ]: Forbes

[ Wed, Oct 29th 2025 ]: The Motley Fool

[ Thu, Oct 23rd 2025 ]: The Globe and Mail

[ Thu, Oct 02nd 2025 ]: The Motley Fool

[ Sun, Sep 28th 2025 ]: Seeking Alpha

[ Wed, Sep 24th 2025 ]: Seeking Alpha

[ Fri, Sep 12th 2025 ]: Fox 11 News

[ Wed, Sep 03rd 2025 ]: Investopedia

[ Fri, Jun 13th 2025 ]: CNN

[ Fri, Apr 25th 2025 ]: Fortune