by: Fox Business

Logan Paul Spends $5.3 Million on Pokemon Cards, Urges Young Investors to Diversify

by: Zee Business

Analyst Picks Highlight Potential Gains in Indian Stocks: Vedanta, BEL, Railtel & More

by: 24/7 Wall St

AI Infrastructure Stocks Poised for Explosive Growth: Analysts Predict Triple-Digit Revenue Jumps

")

for Long-Term Growth")

Stock Picking Skills Fading: The Rise of Index Funds

Seeking Alpha

Seeking Alpha

The Fading Craft of Stock Picking: How Indexing is Reshaping Investment & Eroding Expertise

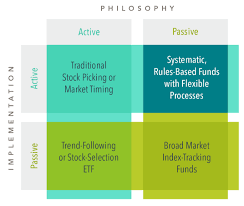

The world of investing has undergone a seismic shift in recent decades, and according to a recent Seeking Alpha article by Steven O'Hanley, the traditional art of stock picking is rapidly becoming a lost one. Driven by the relentless growth and dominance of index funds and ETFs, active managers are struggling, and the skills required to identify undervalued companies are increasingly atrophying within the investment community. The piece argues that this isn’t simply about underperformance; it's about a fundamental change in how markets function and the expertise available to navigate them.

O'Hanley lays out the core problem: the sheer scale of assets flowing into passive index strategies has created a powerful feedback loop. As more investors chase benchmark returns, they inherently funnel capital into those benchmarks, further reinforcing their dominance. This creates a situation where active managers are not only competing against a moving target (the constantly rebalancing index) but also facing pressure to deliver returns that justify higher fees – a difficult proposition when the average investor is perfectly content with mirroring market performance.

The article highlights several key points illustrating this trend. Firstly, it underscores the historical dominance of active management. For decades, skilled stock pickers genuinely outperformed indices, proving their value in identifying opportunities missed by broad-market strategies. However, over the last 15-20 years, this has dramatically reversed. The rise of low-cost index funds, particularly those tracking the S&P 500, has made it increasingly difficult for active managers to justify their existence. The sheer breadth of available ETFs covering every conceivable niche and strategy further complicates matters.

O'Hanley points out that this isn’t just about a few bad years for active managers. The persistent underperformance is statistically significant and widespread. Many actively managed funds consistently fail to beat their benchmarks after accounting for fees, a phenomenon often attributed to “closet indexing” – where fund managers passively track the index while still charging higher active management fees. This cynicism further erodes investor trust in the ability of active managers to deliver genuine alpha (returns above market performance).

The article then delves into why this shift is happening and its consequences. Low costs are a major driver. Index funds offer significantly lower expense ratios than actively managed funds, making them incredibly attractive to cost-conscious investors. Furthermore, the rise of algorithmic trading and quantitative strategies has made it harder for traditional fundamental analysis – the cornerstone of stock picking – to uncover hidden value. These sophisticated algorithms can process vast amounts of data far more quickly and efficiently than human analysts, eroding their edge.

A crucial element O'Hanley explores is the “index effect.” As companies are added to the S&P 500, they receive a massive influx of capital from index funds. This artificial demand often pushes stock prices higher, regardless of the company’s underlying fundamentals. This creates a situation where active managers who do identify undervalued companies find that those valuations are quickly corrected by the relentless buying pressure from passive investors. The article references research suggesting that this "index effect" can significantly distort market prices and make it more challenging to find true bargains.

The consequences of this trend, according to O'Hanley, extend beyond just investment returns. He argues that the decline in stock picking expertise is detrimental to market efficiency. When fewer individuals are actively analyzing companies and identifying mispricings, markets become less efficient, potentially leading to asset bubbles and increased volatility. The article implies a concern that the focus shifts from fundamental value creation to simply maintaining index weightings, which can incentivize short-term behavior rather than long-term growth.

The piece also touches upon the impact on the financial industry itself. As assets flow into passive strategies, investment banks and research firms are reducing their coverage of individual companies. This further diminishes the availability of fundamental analysis and makes it even more difficult for active managers to stay informed. The article suggests a vicious cycle is at play: less stock picking leads to less research, which in turn reinforces the dominance of passive investing.

Finally, O'Hanley poses a question about the future. While he acknowledges that index funds are likely here to stay, he suggests there’s still potential for skilled active managers who can adapt and embrace new technologies while maintaining a focus on fundamental value. He implies that finding these managers will require a shift in investor expectations – being willing to pay higher fees for potentially superior returns and understanding the inherent risks associated with active management. The article doesn't offer easy solutions, but it serves as a stark warning about the potential erosion of expertise and market efficiency if the current trend continues unchecked. The art of stock picking isn’t dead, but it is undeniably fading, and its survival depends on a renewed appreciation for fundamental analysis and a willingness to challenge the passive investing orthodoxy.

This article summarizes the key arguments presented in O'Hanley's piece and expands upon them with additional context and implications. It aims to capture the essence of his concerns about the decline of stock picking expertise and the impact of index fund dominance on financial markets.

Read the Full Seeking Alpha Article at:

https://seekingalpha.com/article/4851101-s-and-p-500-stock-picking-becomes-a-lost-art-as-index-forces-take-over

on: Mon, Dec 08th 2025

by: Seeking Alpha

S&P 500 Stock Picking Becomes a Lost Art as Index Forcers Take Over

on: Tue, Dec 23rd 2025

by: moneycontrol.com

India's Index-Fund Boom Is Not a One-Size-Fit Solution, Says Vikas Khemani

on: Wed, Nov 19th 2025

by: moneycontrol.com

BlackRock's $185 B Model: The New Driver Behind Global Equity Bets

on: Mon, Nov 17th 2025

by: Let's Talk Money! with Joseph Hogue, CFA

Start With a Solid Foundation: Setting Clear Goals and Choosing the Right Brokerage

on: Wed, Dec 17th 2025

by: Seeking Alpha

Safe-Asset Squeeze Looms: Treasury Yields Surge, Driving Capital Toward Equities

on: Wed, Dec 24th 2025

by: USA Today

Is the Classic 60/40 Portfolio Still Solid in an AI-Driven Market?

on: Fri, Dec 19th 2025

by: The Motley Fool

Three Vanguard ETFs to Build a Long-Term Portfolio with Just $500

on: Wed, Dec 17th 2025

by: AOL

on: Tue, Dec 16th 2025

by: The Daily Overview

Should You Invest in Stocks in 2026? History Shows a Long-Term Upside

on: Sun, Dec 14th 2025

by: Dallas Morning News

Motley Fool Launches Active-Style ETFs Offering Managed Growth Exposure

on: Sat, Dec 13th 2025

by: The Motley Fool

Investing in the Stock Market in 2026: Historical Trends and Future Outlook

on: Wed, Dec 03rd 2025

by: Local 12 WKRC Cincinnati