by: Business Insider

Sector Rotation: Investors Shift from Nasdaq-100 Tech to Defensive Non-Tech Leaders

by: Zee Business

Motilal Oswal Projects Strong Growth for HNI Wealth Management Amid India's HNI Boom

Achieves A+ Profitability: 20% YoY Revenue Growth and $2.56 EPS")

by: The Motley Fool

AI-Driven Surge: How Oracle and Broadcom Are Powering the Next Generation of Computing

by: Seeking Alpha

John Hancock Multi-Manager 2055 Lifetime Portfolio Q3 2025 Outperforms Benchmark with 7.1% Return

by: The Motley Fool

Palantir's Platform-First Model Positions It as a Government-Grade Analytics Leader

Cash vs Investing: Lessons from 2010's Recovery Year

This is Money

This is MoneyLocale: UNITED KINGDOM

Cash vs Investing: What 2010 Taught Us About Building Long‑Term Wealth

(A 500‑plus‑word summary of the Money article published on The Money – “Cash vs investing: 2010 returns compare best building long‑term wealth”)

1. The Big Picture

The article takes readers on a quick yet comprehensive journey through the performance of various investment vehicles in the year 2010 – a pivotal post‑financial‑crisis year – and distils that information into practical advice for anyone who wants to build wealth over the long haul. It asks the simple question: Should I keep my money in cash or invest it? and answers by looking at historical returns, risk, and the time‑horizon required to achieve financial goals.

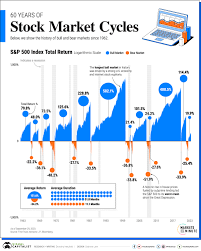

2. 2010 – The “Recovery Year”

2010 was the year that the global markets were still finding their footing after the 2008 crash. The article highlights how the markets bounced back:

| Asset Class | Approximate Return (UK) |

|---|---|

| Cash (Savings accounts, money‑market funds) | +0.1 % (after inflation, effectively negative) |

| UK Equities (FTSE 100, MSCI World) | +13–15 % |

| UK Bonds (gilts, corporate bonds) | +5–7 % |

| Real Estate (UK house price index) | +12–14 % |

| International ETFs (US, Global) | +12–15 % |

These numbers illustrate the stark contrast between low‑risk, low‑return cash and higher‑risk, higher‑return equities and property. The article stresses that cash in 2010 produced almost nothing – a key point for those who still think of savings accounts as a “safe” place to store money.

3. Why Cash Falls Short

Inflation Outpaces Interest

Even the best UK savings accounts were offering just over 0.1 % per annum in 2010, while UK inflation hovered around 2.5 %. That means real purchasing power fell.Opportunity Cost

The money kept in cash could have been invested in a diversified portfolio that, over a decade, might have doubled in value. The article calculates a simple scenario: £10,000 in cash versus £10,000 invested in an average‑returning equity index over ten years – the latter grows to roughly £20,000.Liquidity is Not a Freebie

While cash is easily accessible, its low return means that you’ll need to save far more to hit the same targets you could have reached by investing.

4. Investing – The Road to Wealth

The article doesn’t just point out cash’s shortcomings; it outlines the why behind why investing, especially in equities, is the most reliable way to grow wealth over time.

4.1 The Power of Compounding

A long‑term investor benefits from the compounding effect: interest earned on previously earned interest. The article shows that a 10 % annual return compounds into a 100 % gain in roughly 7.5 years, and a 15 % return does so in about 5 years. Even a modest 5 % return, when compounded over 30 years, more than triples the initial investment.

4.2 Diversification Balances Risk

The article advises a well‑balanced portfolio that includes:

- Equities – 50–70 % of the portfolio.

- Fixed income (bonds) – 20–30 % to dampen volatility.

- Real estate or property funds – 5–10 % for an additional inflation hedge.

- Cash – 5 % as a buffer for emergencies.

Such diversification keeps the portfolio’s volatility manageable while still capturing the higher returns of equities.

4.3 Tax‑Advantaged Accounts

A significant portion of the article is devoted to explaining how the UK’s Individual Savings Accounts (ISAs) and Self‑Invested Personal Pensions (SIPPs) can turbo‑charge returns. Contributions grow tax‑free or tax‑deferred, allowing the compounding power to run unhindered by the UK’s 20–40 % income tax and capital gains tax. The article reminds readers that the maximised annual ISA contribution for 2020‑2021 was £5,000; any unused allowance can be carried forward to the next tax year.

5. The “How” – Putting the Plan into Action

Start Early – The article shows a graph comparing a 10‑year versus a 30‑year plan. The 10‑year plan yields roughly £13,000 on a £10,000 investment (at 8 % average return), while the 30‑year plan yields £100,000. The difference is pure time.

Automate Your Investments – Setting up a monthly “robo‑advisor” or automatic contributions into an ISA or SIPP reduces the temptation to time the market and keeps you invested.

Re‑balance Periodically – As you age, your risk tolerance typically declines. The article suggests shifting from a 70/30 equity/bond mix to a 50/50 mix by the time you’re 55–60 years old. This keeps the portfolio aligned with your financial goals.

Stay Informed but Not Overreactive – Market volatility is inevitable. The article references the 2008 crash and the subsequent 2010 rally as an illustration that markets recover, and it encourages a “buy the dip” mindset rather than panic selling.

6. Links to Further Reading

The Money article pulls in several external sources to back up its claims:

Bank of England’s “Rate of Return on Cash” – The article cites the BoE’s 2010 statistical releases to show that cash yields were essentially zero.

S&P Global’s “Historical Market Returns” – This source provides the basis for the equity return figures and illustrates the long‑term trend.

The Treasury’s “Personal Tax Reliefs” – A reference page that explains the details of ISAs, pension contributions, and the associated tax reliefs.

“How to Use a SIPP” – A short guide on setting up a Self‑Invested Personal Pension, which the article uses to show how you can build a diversified portfolio in a tax‑advantaged wrapper.

Readers are encouraged to follow these links for deeper insight into each data set and to learn how to implement the strategies discussed.

7. Takeaway

In a nutshell, the Money article offers a clear, data‑driven verdict: Cash is too cheap in a low‑interest environment and fails to keep pace with inflation. In contrast, a diversified investment portfolio, particularly one heavy in equities and housed within tax‑advantaged accounts, delivers the compound returns required for genuine long‑term wealth building.

The lesson from 2010, then, is universal: put your money to work for you instead of letting it sit idle. Start early, stay diversified, and let the power of compounding do the heavy lifting.

Read the Full This is Money Article at:

https://www.thisismoney.co.uk/money/investing/article-15374509/Cash-vs-investing-2010-returns-compare-best-building-long-term-wealth.html

This is Money

on: Mon, Nov 17th 2025

by: MoneyWeek

High-Value Shares ISAs Can Be Worth 17 Times More Than Cash After Ten Years

on: Fri, Nov 21st 2025

by: The Motley Fool

Turning $10,000 into a Million in Ten Years - What the Numbers Really Show

on: Thu, Nov 20th 2025

by: Let's Talk Money! with Joseph Hogue, CFA

on: Fri, Dec 12th 2025

by: moneycontrol.com

on: Sat, Dec 13th 2025

by: The Motley Fool

Investing in the Stock Market in 2026: Historical Trends and Future Outlook

on: Tue, Nov 25th 2025

by: Moneywise

66% of American Investors Favor Real Estate as Their Top Alternative to Stocks and Bonds

on: Mon, Nov 24th 2025

by: 24/7 Wall St

Warren Buffett: The Investor Who Never Recorded a Negative Year

on: Tue, Dec 09th 2025

by: The Independent

on: Mon, Dec 01st 2025

by: Let's Talk Money! with Joseph Hogue, CFA

Beginner's Roadmap to Stock-Market Investing: Key Takeaways from MSN Money

on: Sat, Nov 29th 2025

by: The Motley Fool

Worried About the Stock Market? Here Are Two Sound Investments to Keep Your Portfolio Steady

on: Tue, Nov 25th 2025

by: The Motley Fool

Vanguard's 'Unstoppable' Momentum: 5,000% Surge in VOO and VIG Holdings

on: Sun, Nov 23rd 2025

by: The Motley Fool

Vanguard's VOO: The Low-Cost S&P 500 ETF That Might Be the Smartest Choice