[ Fri, Feb 20th ]: Business Insider

[ Fri, Feb 20th ]: CNBC

[ Fri, Feb 20th ]: moneycontrol.com

[ Fri, Feb 20th ]: Sporting News

[ Fri, Feb 20th ]: The Globe and Mail

[ Fri, Feb 20th ]: This is Money

[ Fri, Feb 20th ]: BBC

[ Fri, Feb 20th ]: Investopedia

[ Fri, Feb 20th ]: Ghanaweb.com

[ Fri, Feb 20th ]: The Telegraph

[ Fri, Feb 20th ]: Defense News

[ Fri, Feb 20th ]: Goodreturns

[ Fri, Feb 20th ]: WTOP News

[ Fri, Feb 20th ]: Yen.com.gh

[ Fri, Feb 20th ]: WVUE FOX 8 News

[ Fri, Feb 20th ]: Staten Island Advance

[ Fri, Feb 20th ]: KOAT Albuquerque

[ Fri, Feb 20th ]: Business Today

[ Fri, Feb 20th ]: The Motley Fool

[ Fri, Feb 20th ]: Seeking Alpha

[ Fri, Feb 20th ]: Dayton Daily News

[ Fri, Feb 20th ]: New York Post

[ Fri, Feb 20th ]: The Salt Lake Tribune

[ Fri, Feb 20th ]: Forbes

[ Thu, Feb 19th ]: Patch

[ Thu, Feb 19th ]: Sporting News

[ Thu, Feb 19th ]: Associated Press

[ Thu, Feb 19th ]: WSB Radio

[ Thu, Feb 19th ]: Dayton Daily News

[ Thu, Feb 19th ]: This is Money

[ Thu, Feb 19th ]: WDRB

[ Thu, Feb 19th ]: KOB 4

[ Thu, Feb 19th ]: profootballnetwork.com

[ Thu, Feb 19th ]: Fox Business

[ Thu, Feb 19th ]: Orlando Sentinel

[ Thu, Feb 19th ]: fox17online

[ Thu, Feb 19th ]: Commercial Observer

[ Thu, Feb 19th ]: WNYT NewsChannel 13

[ Thu, Feb 19th ]: Investopedia

[ Thu, Feb 19th ]: Toronto Star

[ Thu, Feb 19th ]: Impacts

[ Thu, Feb 19th ]: Fortune

[ Thu, Feb 19th ]: The Motley Fool

[ Thu, Feb 19th ]: WISH-TV

[ Thu, Feb 19th ]: The Globe and Mail

[ Thu, Feb 19th ]: Seeking Alpha

[ Thu, Feb 19th ]: WTOP News

[ Thu, Feb 19th ]: CNBC

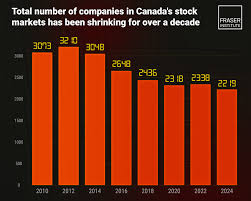

Canadian PE Faces Regulatory Hurdles

Locale: CANADA

Regulatory Hurdles: A Canadian Constraint

A significant deterrent to PE activity in Canada is its comparatively stringent regulatory environment. The Investment Canada Act (ICA) mandates a 'net benefit test' for foreign acquisitions, requiring a subjective assessment of whether the deal will positively contribute to the Canadian economy. This process, while intended to protect national interests, introduces considerable time, cost, and uncertainty for PE firms. Obtaining approval can be protracted and complex, diminishing the attractiveness of Canadian targets relative to those in jurisdictions with more streamlined processes, like the United States.

The Composition of the TSX: A Sectoral Imbalance

The TSX's sectoral composition further limits the scope for PE investment. The index is heavily weighted towards resource extraction industries (energy, mining, materials) and highly regulated sectors like banking, railways, and utilities. These industries, while often stable and providing consistent returns, generally don't align with the typical PE investment profile. PE firms typically favor companies with higher growth potential, operational flexibility, and opportunities for rapid value creation through restructuring or expansion. Resource companies are often subject to volatile commodity prices, while regulated industries face constraints on pricing and operational changes.

Canadian Pension Fund Dynamics: Shifting Investment Strategies

Traditionally, Canadian pension funds have been crucial limited partners (LPs) in private equity funds, providing a substantial portion of the capital deployed. However, a significant shift is underway. These funds are increasingly opting for direct investing, bypassing PE firms and investing directly in companies themselves. This 'internalization' of investment activity allows pension funds to capture a larger share of the profits and exercise greater control over their investments. Consequently, less capital is flowing through PE funds, reducing their capacity to pursue deals. The Canada Pension Plan Investment Board (CPPIB), for example, has demonstrably increased its direct investment allocations in recent years.

Maturity of Listed Companies: Limited Operational Upside

Many TSX-listed companies are mature, well-established businesses. While stable and profitable, they offer less opportunity for the aggressive operational improvements and growth initiatives that PE firms typically seek. PE firms thrive on identifying undervalued companies with potential for turnaround or expansion, but these opportunities are less prevalent among the more mature TSX constituents. The potential for substantial value creation through restructuring or innovation is often limited.

What to Expect: Continued, but Limited, Activity

Despite these headwinds, private equity will undoubtedly remain an active player in the Canadian market. We can anticipate a steady stream of smaller deals, corporate restructurings, and niche acquisitions. However, the likelihood of a transformative wave of take-private transactions dramatically altering the TSX is low. The unique combination of regulatory constraints, sectoral composition, shifting pension fund strategies, and the maturity of listed companies creates a challenging environment for large-scale PE investment. Investors shouldn't necessarily expect a flood of lucrative offers for TSX-listed companies. The global PE boom is real, but its impact on the Canadian stock market will likely be far more muted than many might hope.

Read the Full The Globe and Mail Article at:

https://www.theglobeandmail.com/business/commentary/article-private-equity-investing-stocks-tsx-ipo/

[ Tue, Feb 17th ]: InvestmentNews

[ Tue, Feb 17th ]: socastsrm.com

[ Tue, Feb 17th ]: WTOP News

[ Tue, Feb 10th ]: reuters.com

[ Tue, Feb 10th ]: The Globe and Mail

[ Fri, Feb 06th ]: reuters.com

[ Thu, Feb 05th ]: Seeking Alpha

[ Tue, Feb 03rd ]: The Globe and Mail

[ Thu, Jan 29th ]: The Motley Fool Canada

[ Fri, Jan 09th ]: The Globe and Mail