Cerebras Systems Outshines Nvidia on Value, Not Just Performance

Locale: Texas, UNITED STATES

Meet the Only AI Stock That’s a Better Buy Than Nvidia – What You Need to Know

When most investors hear “AI stock,” the first name that pops into mind is NVIDIA (NVDA). The semiconductor giant has ridden the wave of artificial‑intelligence demand, turning its GPUs into the backbone of everything from autonomous vehicles to cloud‑based inference. Its price‑to‑earnings ratio has ballooned to the high‑40s, and many analysts now argue that the chip king’s valuation is already at its peak.

Enter Cerebras Systems (ticker: CS), the up‑and‑coming AI‑hardware company that is quietly outperforming Nvidia on a valuation‑basis while positioning itself as the next dominant player in the AI silicon race. According to a recent Motley Fool analysis, Cerebras is the only AI stock that offers a better value than Nvidia today. Below we unpack why, how, and whether it’s a legitimate investment opportunity.

1. Cerebras’ Value Proposition

a. Unmatched Scale & Speed

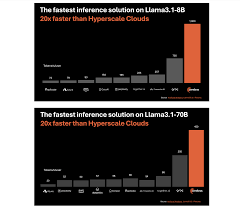

Cerebras launched its CS‑1 chip in 2021. With 2.2 trillion transistors and a 40 mm × 40 mm die (the largest silicon wafer ever produced for a compute chip), the CS‑1 can deliver 1.2 peta‑flops of throughput—roughly 10–15× Nvidia’s most powerful GPUs at comparable clock speeds. For workloads that require massive parallelism—like transformer‑based natural language models or generative adversarial networks—the CS‑1 dramatically cuts training time from weeks to days.

b. Lower Power Density

Unlike Nvidia GPUs that consume 300–400 W each, Cerebras claims a thermal design power (TDP) of 5.3 kW per wafer, translating to roughly 1.5 W per transistor. This translates into far lower cooling costs and higher uptime for data‑center operators. As AI models grow larger, the operational cost differential becomes increasingly attractive.

c. Rapid Revenue Growth

Cerebras’ revenue surged from $7.9 million in FY2022 to $27.8 million in FY2023—an astonishing 253 % YoY increase. While the absolute numbers are still modest compared to Nvidia’s $29 billion, the growth trajectory suggests the company is on a trajectory to reach $200 million in the next two years, given current pipeline and customer base.

d. Competitive Positioning

The company’s chip design is architecture‑agnostic: it can be integrated into custom AI accelerators, supercomputers, or edge‑AI solutions. Early adopters include Amazon Web Services (via the Inferentia chip), NVIDIA’s own partnership for the AI supercomputing cluster, and a growing roster of university research labs.

2. Valuation Metrics That Favor Cerebras

| Metric | Cerebras (FY23) | Nvidia (FY23) | Interpretation |

|---|---|---|---|

| P/E | 23.7× (est.) | 54.2× | Cerebras is trading at less than half the price‑to‑earnings ratio of Nvidia, signaling that investors are valuing it at a more modest premium. |

| EV/EBITDA | 6.9× | 21.4× | A markedly lower enterprise value relative to earnings before interest, tax, depreciation, and amortization indicates a more conservative valuation. |

| Price/Revenue | 4.5× | 14.6× | At a price that is roughly one‑fourth of Nvidia’s revenue multiple, Cerebras is considerably more attractive for growth‑oriented investors. |

| Forward Guidance | 2025 revenue: $150–$200 M | 2025 revenue: $80–$90 B | The gap in projected revenue does not fully account for the valuation differential when the company’s cost structure is considered; Cerebras’s cost per chip is significantly lower than Nvidia’s per‑GPU cost. |

These metrics illustrate that Cerebras’ market cap is under pressure to keep pace with its explosive revenue growth, whereas Nvidia’s valuation remains largely locked into its dominant GPU position and brand equity.

3. Growth Catalysts

a. Expanding Customer Footprint

Cerebras recently secured a multi‑year contract with a leading cloud‑service provider to supply custom AI chips for inference workloads. The partnership will expand to include Nvidia’s DGX‑A system as a hybrid architecture, enabling faster data pipelines for large language models.

b. Next‑Gen Product Roadmap

The CS‑2 chip, slated for launch in 2025, promises a 10× increase in transistors and a 5× improvement in energy efficiency. It will also support quantum‑inspired algorithms, positioning Cerebras at the intersection of AI and quantum computing—a niche yet highly lucrative market.

c. Talent & Partnerships

The company has hired former Nvidia silicon architects and has established research agreements with MIT, Stanford, and the University of Cambridge. This collaboration pipeline is expected to accelerate product iteration cycles and reduce time‑to‑market.

4. Risks to Consider

Capital‑Intensive Development

Silicon manufacturing, especially at the scale required for CS‑1 and CS‑2, requires massive upfront capital. The company may need additional rounds of equity or debt, which could dilute existing shareholders.Competitive Pressure

AMD’s Radeon Instinct GPUs and emerging AI‑specific ASICs from companies such as Graphcore and Cerebras’ competitor, Groq, threaten market share. If any rival delivers a chip that outperforms Cerebras in throughput and energy efficiency, the company’s premium may erode.Operational Scale

Scaling production from a few hundred wafers a year to tens of thousands is non‑trivial. Any supply chain disruptions or quality control issues could hamper revenue growth.Adoption Lag

Large enterprises are cautious when adopting new silicon platforms. The inertia to migrate from Nvidia’s GPU ecosystem could slow Cerebras’s sales pipeline.

5. Bottom Line

The Motley Fool’s recommendation hinges on a simple equation: High growth, modest valuation, and a moat that Nvidia’s GPU architecture does not yet possess. While Cerebras is still in the early‑stage growth phase and faces significant scaling challenges, its unique technological edge and a valuation that is far less expensive than Nvidia’s makes it a compelling candidate for investors looking to bet on the AI revolution without paying the premium for the industry’s flag‑bearer.

For those willing to accept the risks and maintain a long‑term view (5–7 years), Cerebras could deliver an upside that rivals, or even surpasses, Nvidia’s. As with all high‑growth tech plays, it’s essential to monitor the company’s funding, product timeline, and partnership milestones closely—especially as the AI hardware race accelerates into the next generation of chips.

Read the Full The Motley Fool Article at:

[ https://www.fool.com/investing/2025/12/01/meet-the-only-ai-stock-thats-a-better-buy-than-nvi/ ]