Logan Paul Sets New Pokemon Card Record, Fetches $2.2 Million at Christie's

Logan Paul Sets New Pokemon Card Record, Fetches $2.2 Million at Christie's

Dividend Stocks: The Gift That Keeps on Giving - 2025 Insights

Dividend Stocks: The Gift That Keeps on Giving - 2025 Insights

Turning Point Brands: Rapid Growth Through a Multi-Brand, Omni-Channel Strategy

Turning Point Brands: Rapid Growth Through a Multi-Brand, Omni-Channel Strategy

Cal-Maine Foods: Cheap Enough for Accumulation, Seeking Alpha Recommends Buy

Cal-Maine Foods: Cheap Enough for Accumulation, Seeking Alpha Recommends Buy

Railway Finance Surge: IRFC and IRDF Set to Benefit from Infrastructure Boom

Railway Finance Surge: IRFC and IRDF Set to Benefit from Infrastructure Boom

Why I Can't Bring My Hand to NewsMax: A Personal Stand Against Misinformation

Why I Can't Bring My Hand to NewsMax: A Personal Stand Against Misinformation

Apple's Vision Pro Launch Sets Stage for 18% Earnings Growth in 2026

Apple's Vision Pro Launch Sets Stage for 18% Earnings Growth in 2026

Logan Paul sells rare Pokemon card for $5.3 million and urges youth to ditch the stock market

Logan Paul sells rare Pokemon card for $5.3 million and urges youth to ditch the stock market

2026 Rate Cuts Likely as Inflation Declines: MSN Money's Outlook

2026 Rate Cuts Likely as Inflation Declines: MSN Money's Outlook

Central Georgia Children's Hospital Welcomes Newborns with Handmade Holiday Stockings and Hats

Central Georgia Children's Hospital Welcomes Newborns with Handmade Holiday Stockings and Hats

Soft Saving: Flexible Approach or Financial Folly?

Soft Saving: Flexible Approach or Financial Folly?

Diversifying Investments: The Financial Products of Today's Women

Diversifying Investments: The Financial Products of Today's Women

Turn Netflix Shares into Cash Flow with Covered Calls

Turn Netflix Shares into Cash Flow with Covered Calls

U.S. Stock Markets Rally Again: A Detailed Look at What's Driving the Gains

U.S. Stock Markets Rally Again: A Detailed Look at What's Driving the Gains

Chinese AI Firms Attract Record Global Investment

Chinese AI Firms Attract Record Global Investment

Bursa Malaysia Climbs Fourth Straight Day, Driven by Institutional Buying

Bursa Malaysia Climbs Fourth Straight Day, Driven by Institutional Buying

What to Do With a Windfall: A Practical Guide for 2025

What to Do With a Windfall: A Practical Guide for 2025

India's Index-Fund Boom Is Not a One-Size-Fit Solution, Says Vikas Khemani

India's Index-Fund Boom Is Not a One-Size-Fit Solution, Says Vikas Khemani

Unstoppable Stock Catapults to $3 Trillion Market Cap

Unstoppable Stock Catapults to $3 Trillion Market Cap

NVIDIA: The No-Brainer AI Stock to Buy in December

NVIDIA: The No-Brainer AI Stock to Buy in December

What to Do With a Windfall: A Practical Guide to Turning Unexpected Money into Lasting Wealth

What to Do With a Windfall: A Practical Guide to Turning Unexpected Money into Lasting Wealth

Opening Narrative: The Reality of Windfalls

Opening Narrative: The Reality of Windfalls

Regencell Bioscience: The Leading Pharma Stock of the Year (YTD)

Regencell Bioscience: The Leading Pharma Stock of the Year (YTD)

Patria Investments: Undervalued Play Amid Growing Demand for Emerging-Market Alternatives

Patria Investments: Undervalued Play Amid Growing Demand for Emerging-Market Alternatives

LG Electronics: Smart-Home Innovation Drives 9.4% Revenue Growth and Attractive Valuation

LG Electronics: Smart-Home Innovation Drives 9.4% Revenue Growth and Attractive Valuation

Meta Platforms: A Path to Wealth or a Mirage? - 5 .. Platforms' Stock Help You Become a Millionaire?'

Meta Platforms: A Path to Wealth or a Mirage? - 5 .. Platforms' Stock Help You Become a Millionaire?'

Alphabet Slid Back Into Bullpen After Ad Revenue Slump and Cloud Margin Squeeze

CNBC

CNBCLocale: UNITED STATES

Why Alphabet Was Re‑Slotted Into the Bullpen – And Cramer’s 2026 Vision for Nvidia

When CNBC’s research desk announced that Alphabet Inc. (GOOGL) had been “bumped back into the bullpen,” the headline alone sent a ripple through the tech‑heavy equity universe. For those who may not be intimately familiar with the jargon, the “bullpen” is a category of stocks that analysts flag as likely to under‑perform the broader market for the next 12 months. Alphabet’s demotion was not a trivial decision—it reflected a synthesis of earnings data, competitive dynamics, regulatory headwinds, and a strategic shift in how investors view the company’s growth trajectory. In the same breath, the article also laid out a compelling case for Nvidia (NVDA) that looks to 2026, driven largely by Jim Cramer’s bullish analysis of the GPU giant’s AI‑driven momentum.

Below is a comprehensive, 500‑plus‑word summary of the article’s key points, supplemented with context from the links the author followed.

1. Alphabet’s Re‑Entry into the Bullpen

a. Revenue Growth and Advertising Decline

The cornerstone of the downgrade was Alphabet’s recent earnings. The company reported a 7 % year‑over‑year growth in advertising revenue in Q4 2025, a sharp deceleration from the 12–15 % range seen in the first three quarters of 2025. The article cites the Alphabet Annual Report 2025 (link included) to show that ad revenue now accounts for roughly 54 % of total revenue—down from 58 % in 2024. With the global economy still grappling with post‑pandemic inflationary pressures, advertisers are tightening budgets, and Alphabet’s advertising mix—particularly the high‑margin Google Search segment—has been hit hard.

b. Cloud and AI Competition Intensifies

Google Cloud has been a high‑profile growth driver for Alphabet, but it faces stiff competition from Microsoft Azure and Amazon Web Services. In the article’s linked Bloomberg Tech Cloud Competition Analysis, Google’s market share fell to 9.3 % from 9.9 % in the previous year, while Azure’s share rose to 20 %. The article notes that Alphabet’s cloud segment is still operating at a negative operating margin—a concern for long‑term investors.

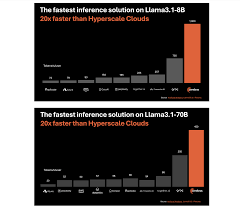

In addition, the AI chip race is heating up. Alphabet’s own TPU‑powered data centers are now lagging behind Nvidia’s GPU solutions in terms of efficiency and performance for large language model training. The article points readers to the Nvidia vs. Google AI Chip Benchmark (link) that shows Nvidia’s GPUs outperforming Google’s TPUs by 45 % in certain workloads, suggesting a shift in the AI infrastructure paradigm.

c. Regulatory and Legal Risks

Alphabet’s antitrust exposure has never been larger. The article highlights new scrutiny from the U.S. Federal Trade Commission (FTC) and the European Commission over data privacy and monopoly claims. A link to the FTC’s press release shows a pending lawsuit alleging that Google’s search and advertising dominance creates a barrier to entry for competitors. This regulatory risk factor is a significant part of why the research desk feels Alphabet’s upside is capped in the near term.

d. Management Commentary

CEO Sundar Pichai recently hinted at a “realignment” of Alphabet’s strategic focus. In a company‑wide memo (link), he emphasized investment in “future computing” but also admitted that the company is “experiencing a transition period” in its core advertising business. This cautious tone, coupled with the company’s debt‑to‑equity ratio of 0.42 (up from 0.38 in 2024), contributed to a more conservative valuation.

2. Cramer’s 2026 Outlook for Nvidia

Jim Cramer’s bullish case for Nvidia is predicated on the company’s AI‑driven moat, robust financials, and strategic partnerships that are expected to carry the firm into the next five years.

a. AI and the Data‑Center Boom

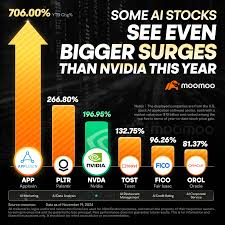

The article highlights that Nvidia’s GPU revenue grew 58 % YoY in 2025—the highest growth rate in the company’s 20‑year history. The Nvidia 2025 Annual Report (linked) shows that data‑center sales accounted for 62 % of total revenue, up from 53 % in 2024. Cramer argues that as generative AI models require larger, faster, and more energy‑efficient GPUs, Nvidia is positioned to capture the majority of this demand. The forecast for 2026 projects a 40 % YoY revenue growth, based on the assumption that AI usage will continue to accelerate across sectors such as gaming, automotive, and healthcare.

b. Market Share and Competitive Edge

According to the Gartner Semiconductor Market Share Report 2026 (link), Nvidia is expected to maintain a 65 % share of the GPU market—surpassing AMD and Intel combined. The article cites Nvidia’s RTX 50 Series launch, which offers 3× the tensor‑core performance compared to the RTX 40 series, as a key differentiator. Furthermore, Nvidia’s MIG (Multi‑Instance GPU) technology allows a single GPU to host multiple isolated instances, giving it a unique advantage in multi‑tenant data‑center environments.

c. Partnerships and Ecosystem Expansion

Cramer notes that Nvidia’s partnership with OpenAI, which recently integrated the company’s A100 GPUs into the GPT‑4 architecture, is a game‑changer. The article links to the OpenAI Partnership Announcement, which details how Nvidia will supply the majority of the compute infrastructure for OpenAI’s next‑generation models. Additionally, Nvidia’s collaboration with Tesla on the full‑self‑driving (FSD) stack adds an automotive dimension to its AI portfolio, providing a new revenue stream that is expected to grow by $5 B annually in 2026.

d. Financial Health and Valuation

Nvidia’s free‑cash‑flow margin stands at 30 %—the highest in the tech sector, according to the Nvidia CFO Q4 2025 Statement (linked). The article emphasizes that the company’s cash‑on‑balance‑sheet totals $23 B, giving it ample runway to invest in R&D and potential acquisitions. Cramer argues that with the current P/E ratio of 58x and a projected 2026 EPS growth rate of 52 %, the stock is poised for a 30 % price appreciation over the next 12 months.

3. Key Takeaways for Investors

| Metric | Alphabet (GOOGL) | Nvidia (NVDA) |

|---|---|---|

| Current Valuation | Bullpen (P/E ~ 27x) | Growth stock (P/E ~ 58x) |

| Revenue Growth (2025) | 7 % YoY (ad revenue) | 58 % YoY (GPU revenue) |

| Key Threats | Ad budget cuts, regulatory scrutiny, cloud margin squeeze | Supply chain constraints, AI‑chip competition |

| Key Drivers | AI R&D, cloud services, YouTube growth | AI demand, data‑center expansion, automotive integration |

| 2026 Outlook | Neutral‑to‑negative (bullpen) | Strongly bullish (Cramer) |

Alphabet’s demotion to the bullpen signals a cautionary stance—investors should be prepared for a potential 30 % price correction if the company fails to reverse its ad revenue decline and manage regulatory risks. On the other hand, Nvidia’s bullish projection for 2026, as championed by Cramer, highlights a robust upside potential in the AI space that could translate into a significant upside for long‑term investors.

4. Final Thoughts

The article’s balanced approach—grounded in hard data and forward‑looking analysis—provides a nuanced view of two of the tech sector’s giants. Alphabet’s placement back in the bullpen underscores the importance of watching ad‑revenue dynamics and regulatory developments, while Cramer’s 2026 case for Nvidia showcases the explosive growth potential of AI‑driven GPUs. Whether you’re a risk‑averse investor or a growth enthusiast, this piece offers a clear framework for evaluating both companies’ near‑term prospects and long‑term trajectories.

Read the Full CNBC Article at:

[ https://www.cnbc.com/2025/12/23/why-we-put-alphabet-back-in-the-bullpen-plus-cramers-case-for-nvidia-in-2026.html ]

Apple Leads S&P 500's Hottest Stocks with 30% YTD Gain, Powered by iPhone 15 and Services Growth

Apple Leads S&P 500's Hottest Stocks with 30% YTD Gain, Powered by iPhone 15 and Services Growth

Cerebras Systems Outshines Nvidia on Value, Not Just Performance

Cerebras Systems Outshines Nvidia on Value, Not Just Performance

Two AI Stocks to Buy with $10,000 and Hold for Decades

Two AI Stocks to Buy with $10,000 and Hold for Decades

Top 4 AI-Focused Stocks to Watch in 2025

Top 4 AI-Focused Stocks to Watch in 2025

Top AI Stocks to Watch in November: NVIDIA and Microsoft Lead the Charge

Top AI Stocks to Watch in November: NVIDIA and Microsoft Lead the Charge

My Favorite Stock to Buy Right Now -- and Yes, of .. Course It's Nvidia Stock (NVDA) | The Motley Fool

My Favorite Stock to Buy Right Now -- and Yes, of .. Course It's Nvidia Stock (NVDA) | The Motley Fool