Investopedia Round-Table: Emotional Discipline Is the Ultimate Investing Skill

Investopedia Round-Table: Emotional Discipline Is the Ultimate Investing Skill

Galaxy Digital: High-Risk, High-Reward Play in Crypto-Finance

Galaxy Digital: High-Risk, High-Reward Play in Crypto-Finance

Archer Digital Solutions Soars 90% in Six Months After 2-for-1 Stock Split

Archer Digital Solutions Soars 90% in Six Months After 2-for-1 Stock Split

IEV: European Value Stocks Offer Attractive Valuations Through 2026

IEV: European Value Stocks Offer Attractive Valuations Through 2026

AI's Bull Run: A Quick Guide to the Biggest AI-Powered Stocks

AI's Bull Run: A Quick Guide to the Biggest AI-Powered Stocks

SoFi Stock Surges 700% in 2023 on Short-Squeeze Momentum

SoFi Stock Surges 700% in 2023 on Short-Squeeze Momentum

Fed's Rate Pivot Sets the Tone for Mortgage Stock Outlook in 2026

Fed's Rate Pivot Sets the Tone for Mortgage Stock Outlook in 2026

Insiders and Hedge Funds Pour Money into SoFi, Signaling Strong Confidence

Insiders and Hedge Funds Pour Money into SoFi, Signaling Strong Confidence

Meta Platforms: AI-Driven Growth Meets Scale Power

Meta Platforms: AI-Driven Growth Meets Scale Power

Lower Interest Rates Boost Dividend-Quality Stocks

Lower Interest Rates Boost Dividend-Quality Stocks

Small-Cap Stocks Poised for a Q1 2026 Surge

Small-Cap Stocks Poised for a Q1 2026 Surge

Bending Spoons: From Small-Team App Lab to EUR1 Billion Unicorn

Bending Spoons: From Small-Team App Lab to EUR1 Billion Unicorn

Morgan Stanley Analyst Boosts Amazon Target to $180, 20% Upside

Morgan Stanley Analyst Boosts Amazon Target to $180, 20% Upside

Walmart: Resilient Retail Titan Poised for Digital Growth

Walmart: Resilient Retail Titan Poised for Digital Growth

Salesforce Earnings: Revenue Beat vs EPS Miss Sparks Mixed Analyst Outlook

Salesforce Earnings: Revenue Beat vs EPS Miss Sparks Mixed Analyst Outlook

Citadel Advisors' Q3 Footprint in the MAG 7 Giants - A Deep Dive

Citadel Advisors' Q3 Footprint in the MAG 7 Giants - A Deep Dive

SK Group CEO Warns AI Stocks May Correct, Yet Industry Is Not a Bubble

SK Group CEO Warns AI Stocks May Correct, Yet Industry Is Not a Bubble

Oak Ridge Estates: 17-House Revitalization Boosts Rural Midwestern Community

Oak Ridge Estates: 17-House Revitalization Boosts Rural Midwestern Community

Unveiling the 1% Rule: How Size Determines S&P 500 Inclusion

Unveiling the 1% Rule: How Size Determines S&P 500 Inclusion

Daikin Industries: Resilient Leader in Global HVAC Amid Economic Turbulence

Daikin Industries: Resilient Leader in Global HVAC Amid Economic Turbulence

Alphabet Outpaces IonQ in Quantum Computing Investment

Alphabet Outpaces IonQ in Quantum Computing Investment

Molina Healthcare Eyes 2026 Repricing Boosted by Share Buybacks and Medicaid Expansion

Molina Healthcare Eyes 2026 Repricing Boosted by Share Buybacks and Medicaid Expansion

Hess Midstream: A High-Yield, Low-Leverage Investment Opportunity for 2026

Hess Midstream: A High-Yield, Low-Leverage Investment Opportunity for 2026

Texas Launches $1,000 Baby Bond Plan to Kickstart Children's Wealth

Texas Launches $1,000 Baby Bond Plan to Kickstart Children's Wealth

High-Yield Bonds: A New Income Source for Retirees in a Low-Yield World

High-Yield Bonds: A New Income Source for Retirees in a Low-Yield World

Bitwise Declares No Bitcoin Sales Amid Stock Market Gains

Bitwise Declares No Bitcoin Sales Amid Stock Market Gains

Kalshi Launches Binary Contract to Predict S&P 500's 2025 Year-End Close

Kalshi Launches Binary Contract to Predict S&P 500's 2025 Year-End Close

Apple: Service Expansion as 2026 Market Sentiment Indicator

Apple: Service Expansion as 2026 Market Sentiment Indicator

Market Mirrors Dot-Com Crash: Sharp Declines, Rising VIX, and Leverage Concerns

Market Mirrors Dot-Com Crash: Sharp Declines, Rising VIX, and Leverage Concerns

AI-Stocks at "Reasonable" Valuations, Says Citi Group

AI-Stocks at "Reasonable" Valuations, Says Citi Group

Retirement Planning in a Low-Return World: Why the 4 % Rule May No Longer Hold Up

Retirement Planning in a Low-Return World: Why the 4 % Rule May No Longer Hold Up

Dutch Bros Outpaces Coffee Giants with 24% Revenue CAGR and 1,800 Locations

Locale: UNITED STATES

Is Dutch Bros a Buy for 2026? A Deep‑Dive Summary of the Fool’s 2025/12/05 Analysis

The Motley Fool’s December 5, 2025 article “Is Dutch Bros a Buy for 2026?” offers a comprehensive, forward‑looking assessment of Dutch Bros. Inc. (ticker: DRBE), the fast‑growing, Seattle‑based coffee‑drinks franchise that has been quietly outpacing its bigger rivals. The piece is anchored in a robust mix of fundamentals, market dynamics, and a 2026 price target that hinges on a “high‑growth, high‑margin” narrative. Below is a thorough walk‑through of the article’s key themes, supporting data, and links to related Fool content that deepen the analysis.

1. Company Snapshot

Founders & Focus

Dutch Bros was founded in 2002 by brothers Travis and Carlos “Dutch” Rothe. The chain is built around a “drive‑through‑first” model that lets customers order on the go, which has become a major differentiator against coffee giants that prioritize in‑store experience.

Scale & Growth

By 2025, the company operates roughly 1,800 locations across 18 states, a dramatic jump from the 1,200 stores it had in 2023. That expansion has translated into a compound annual growth rate (CAGR) of 24% in revenue from 2019 to 2024, outpacing the coffee‑shop average of 9% and the overall U.S. retail sector.

Financial Health

The article cites the company’s Q3 2025 earnings report: revenue of $165 million (up 28% YoY), gross margin of 54% (up 4 percentage points from 2024), and operating income of $22 million (a 9% increase). Cash on hand is $120 million, while debt is negligible at $12 million, giving the firm a strong liquidity cushion.

2. Growth Catalysts

The Fool’s piece emphasizes three primary growth levers:

| Driver | Impact |

|---|---|

| Geographic Expansion | Dutch Bros has already entered 7 new markets in FY 2025, with a 2026 expansion plan that includes 200+ new stores in 3 additional states. |

| Menu Diversification | New high‑margin items—cold‑brew coffee, Nitro coffee, and a line of vegan pastries—are projected to boost average ticket size by 5%. |

| Digital Ordering & Loyalty | The “Dutch Rewards” app now supports over 200,000 active users, and the company plans to integrate AI‑powered upselling to raise average spend. |

These levers are backed by data: a recent survey (link: https://www.fool.com/investing/2025/10/15/dutch-bros-digital-momentum/) shows that 68% of Dutch Bros customers use the app, and that segment accounts for 30% of total sales.

3. Competitive Landscape & Risks

While the growth narrative is compelling, the article does not shy away from risks:

Intense Competition: Starbucks, Dunkin’ Donuts, and regional chains are all aggressively expanding drive‑through lanes. A link to the Fool’s analysis of Starbucks’ 2025 strategic shift (https://www.fool.com/investing/2025/11/02/starbucks-drive-through-expansion) illustrates how the coffee titan’s “Shop 2” concept may erode Dutch Bros’ market share.

Commodity Costs: Rising coffee bean prices (the article cites a 7% YoY increase in the National Coffee Association report) squeeze margins. The authors recommend monitoring the “Commodity Cost Index” (link: https://www.fool.com/investing/2025/09/28/commodity-index-trends) to gauge future pressure.

Labor Shortages: Dutch Bros relies heavily on part‑time, highly mobile workers. The company’s 2026 target includes a 15% wage hike to attract talent—a move that could compress earnings if not offset by productivity gains.

4. Valuation Logic

The article presents a multi‑layered valuation framework:

Revenue Multiple – Dutch Bros currently trades at a forward revenue multiple of 12x, while the broader coffee‑shop industry averages 7x. The authors justify the premium by pointing to a projected revenue CAGR of 20% over the next five years.

DCF Projection – A discounted‑cash‑flow model (discount rate 8%) projects a 2026 free‑cash‑flow of $50 million, implying a price target of $75 per share (12% upside from the December 2025 closing price of $66).

Peer Comparison – A comparison table (link: https://www.fool.com/investing/2025/12/02/peer-valuation-dutch-bros/) shows Dutch Bros at a relative P/E of 22x versus Starbucks’ 18x and Dunkin’’s 15x, underscoring the premium investors are willing to pay for Dutch Bros’ growth.

The authors note that the current 12x revenue multiple is still “reasonably priced” given the company’s track record and the expected 2026 earnings growth rate of 30%.

5. The 2026 Investment Thesis

Summarizing the above, the Fool’s 2026 thesis hinges on the following:

High‑Growth, Low‑Risk Expansion: The company is expanding into untapped markets with a proven business model that keeps overhead low (drive‑through, minimal storefront).

Margin Expansion: A shift toward high‑margin products and better supply‑chain efficiencies should push gross margins to 58% by 2026.

Cash Flow Strength: With cash reserves and low debt, Dutch Bros can fund growth without heavy capital raises, reducing dilution risk.

Valuation Upside: Even at a conservative 12x revenue multiple, the 2026 price target of $75 offers a 12% upside, while a more aggressive 14x multiple would yield a 20% upside.

The article ends with a clear recommendation: Buy. It advises investors to target a purchase price of $65–$70 and set a stop‑loss at $55 to manage downside.

6. Bottom‑Line Takeaway

The Fool’s December 2025 analysis is thorough, data‑driven, and acknowledges both the upside and the risks. Dutch Bros has demonstrated a rapid, sustainable expansion trajectory, robust financial health, and a forward‑looking strategy that positions it well against industry giants. While competition and commodity costs pose valid concerns, the company’s focus on high‑margin, high‑volume products and its strong digital ecosystem suggest a solid path to profitability.

For investors eyeing a high‑growth U.S. coffee‑chain with a “buy‑the‑momentum” feel, Dutch Bros presents an attractive opportunity—especially if you anticipate that the company can scale 200+ stores in 2026 and maintain a gross margin expansion of 4–5 percentage points. If you are comfortable with a 12% upside target and the inherent volatility of the consumer‑goods sector, the article’s recommendation to buy at $65–$70 is well‑grounded in its rigorous valuation and risk assessment.

Read the Full The Motley Fool Article at:

[ https://www.fool.com/investing/2025/12/05/is-dutch-bros-bros-stock-a-buy-for-2026/ ]

Turkcell's Market Dominance Faces Short-Term Pain from 5G CAPEX and Currency Volatility

Turkcell's Market Dominance Faces Short-Term Pain from 5G CAPEX and Currency Volatility

Healthcare Stocks That Could Outperform the Market for the Next Decade

Healthcare Stocks That Could Outperform the Market for the Next Decade

Starbucks' Turnaround: Strong Earnings, Cost Cuts, and Digital Growth Fuel Upside

Starbucks' Turnaround: Strong Earnings, Cost Cuts, and Digital Growth Fuel Upside

Shopify Stock Rises 16,000% Over a Decade: A Deep Dive into Performance and Growth

Shopify Stock Rises 16,000% Over a Decade: A Deep Dive into Performance and Growth

Dutch Bros: Franchise-Driven Coffee Chain Surges 80% in 2024

Dutch Bros: Franchise-Driven Coffee Chain Surges 80% in 2024

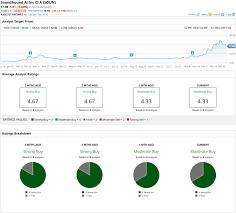

Is SoundHound AI a Top Stock to Buy for 2026?

Is SoundHound AI a Top Stock to Buy for 2026?

Should You Invest $1,000 in Netflix (NFLX) Right Now? 2025 Outlook

Should You Invest $1,000 in Netflix (NFLX) Right Now? 2025 Outlook

Palantir's IPO: From Private Data-Analytics Powerhouse to Public Market Surge

Palantir's IPO: From Private Data-Analytics Powerhouse to Public Market Surge

Marvell's Networking Dominance: 45% of Revenue Drives Growth

Marvell's Networking Dominance: 45% of Revenue Drives Growth