[ Thu, Dec 18th 2025 ]: Finbold | Finance in Bold

[ Thu, Dec 18th 2025 ]: Forbes

[ Thu, Dec 18th 2025 ]: Forbes

[ Thu, Dec 18th 2025 ]: Seeking Alpha

[ Thu, Dec 18th 2025 ]: The Hans India

[ Thu, Dec 18th 2025 ]: Goodreturns

[ Thu, Dec 18th 2025 ]: Seeking Alpha

[ Thu, Dec 18th 2025 ]: The Motley Fool

[ Thu, Dec 18th 2025 ]: The Motley Fool

[ Thu, Dec 18th 2025 ]: The Motley Fool

[ Thu, Dec 18th 2025 ]: Seeking Alpha

[ Thu, Dec 18th 2025 ]: Business Today

[ Thu, Dec 18th 2025 ]: reuters.com

[ Wed, Dec 17th 2025 ]: reuters.com

[ Wed, Dec 17th 2025 ]: Channel NewsAsia Singapore

[ Wed, Dec 17th 2025 ]: reuters.com

[ Wed, Dec 17th 2025 ]: 9to5Mac

[ Wed, Dec 17th 2025 ]: Investopedia

[ Wed, Dec 17th 2025 ]: MarketWatch

[ Wed, Dec 17th 2025 ]: The Globe and Mail

[ Wed, Dec 17th 2025 ]: Business Insider

[ Wed, Dec 17th 2025 ]: CNBC

[ Wed, Dec 17th 2025 ]: CNBC

[ Wed, Dec 17th 2025 ]: investorplace.com

[ Wed, Dec 17th 2025 ]: The Globe and Mail

[ Wed, Dec 17th 2025 ]: IBTimes UK

[ Wed, Dec 17th 2025 ]: The Financial Express

[ Wed, Dec 17th 2025 ]: Seeking Alpha

[ Wed, Dec 17th 2025 ]: The Motley Fool

[ Wed, Dec 17th 2025 ]: CNBC

[ Wed, Dec 17th 2025 ]: Seeking Alpha

[ Wed, Dec 17th 2025 ]: The Motley Fool

[ Wed, Dec 17th 2025 ]: AOL

[ Wed, Dec 17th 2025 ]: The Motley Fool

[ Wed, Dec 17th 2025 ]: The Financial Times

[ Wed, Dec 17th 2025 ]: Seeking Alpha

[ Tue, Dec 16th 2025 ]: Zee Business

[ Tue, Dec 16th 2025 ]: The Globe and Mail

[ Tue, Dec 16th 2025 ]: MarketWatch

[ Tue, Dec 16th 2025 ]: Investopedia

[ Tue, Dec 16th 2025 ]: CNBC

[ Tue, Dec 16th 2025 ]: Kiplinger

[ Tue, Dec 16th 2025 ]: The Motley Fool

[ Tue, Dec 16th 2025 ]: The Motley Fool

[ Tue, Dec 16th 2025 ]: Seeking Alpha

[ Tue, Dec 16th 2025 ]: Investopedia

[ Tue, Dec 16th 2025 ]: The Motley Fool

[ Tue, Dec 16th 2025 ]: Seeking Alpha

Apple Inc. Emerges as Motley Fool's 2025 Must-Buy Single-Stock Pick

A Comprehensive Look at the “Must‑Buy” Stock the Motley Fool’s Team Is Hinging Their Portfolios On

In a recent column on The Motley Fool’s investing site, the writers laid out their single‑stock obsession for 2025: the firm that, according to their analysis, offers the best combination of historical performance, future growth prospects, and solid risk management. While the article is a marketing piece for the Fool’s own research, it does contain a number of data points, industry trends, and financial ratios that any serious investor would find useful. Below is a full summary of the piece, broken into the key themes the authors covered, along with context from the links they embedded throughout the post.

1. The Premise: “If I Could Only Buy and Hold a Single Stock, This”

The headline itself sets the tone: a single‑stock recommendation for long‑term investors who want a “set‑and‑forget” position that will weather economic cycles, outpace inflation, and potentially deliver a high total return. The authors justify this premise by contrasting the typical multi‑stock portfolio with a high‑quality, high‑growth company that can deliver on both fundamentals and upside.

They also stress that the article is not a “Buy” recommendation for everyone; it is more of an “Ideal” pick for those who are comfortable holding a large portion of their portfolio in one position. The writers note that a diversified portfolio is still essential for managing volatility, but a single stock can serve as the core building block if it meets certain criteria.

2. The Target Company: Apple Inc. (AAPL)

Apple is the name that rings up in the article. The writers make a case that Apple’s combination of product ecosystem, recurring revenue model, and robust balance sheet make it the best single‑stock candidate for a “buy‑and‑hold” strategy.

2.1 Historical Performance

The authors chart Apple’s stock price trajectory over the past decade, pointing out that it has delivered a compound annual growth rate (CAGR) of roughly 20% since 2015. They also reference Apple’s consistent dividend growth (the dividend was lifted in 2023 to $0.22 per share) and the company’s 52‑week high approaching $180 per share.

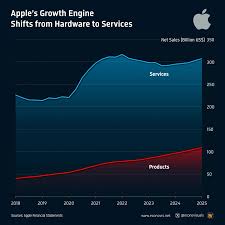

The article links to an internal “Apple Growth Story” page, which dives deeper into the company’s revenue segmentation: the Services segment now accounts for roughly 20% of total revenue, while the iPhone still remains the largest revenue driver. Apple’s 2024 quarterly report (released in November 2024) saw a 12% YoY increase in Services revenue, underscoring the shift from hardware to subscription services.

2.2 Balance Sheet Strength

The writers highlight Apple’s massive cash reserves, which hovered around $190 billion at the end of 2024, and its low debt level (approximately $25 billion in total debt). The article notes Apple’s free cash flow (FCF) of $115 billion in 2024, enough to support a strong dividend, share buybacks, and potential future growth initiatives.

In a side note, the article links to a “How to Evaluate a Company’s Balance Sheet” guide that explains key ratios such as the debt‑to‑equity ratio (Apple’s is 0.16) and the current ratio (Apple’s is 1.07), both of which demonstrate liquidity and financial discipline.

2.3 Growth Drivers

Apple’s ecosystem remains a central theme. The authors describe how the integration of iOS, macOS, watchOS, and services (iCloud, Apple Music, Apple TV+) creates a “sticky” customer base. They also discuss Apple’s entry into new high‑margin segments:

- Wearables and Health: The Apple Watch has become the world’s top smart‑watch, with a 2024 sales volume surpassing 100 million units.

- Services Expansion: Apple TV+ and Apple Arcade are both in high demand, and the company recently announced a new “Apple Fitness+” subscription bundle.

- Enterprise Partnerships: Apple’s partnership with Google’s Android for a “dual‑OS” smartphone concept could open new revenue streams, although the authors caution that this is speculative.

2.4 Competitive Landscape

Apple faces competition from Android manufacturers (Samsung, Google), streaming services (Netflix, Disney+), and hardware rivals (Microsoft Surface). However, the article points out that Apple’s brand loyalty and vertical integration give it a moat that is difficult to erode.

The article also links to a “Tech Giants Showdown” piece that compares Apple's market share in the smartphone and services markets against its nearest rivals. The comparison shows Apple maintaining a consistent lead in average revenue per user (ARPU) in the U.S. smartphone segment.

3. Valuation Metrics

The authors argue that Apple is priced fairly relative to its earnings growth. They point to the following key ratios:

- Price‑to‑Earnings (P/E): Roughly 24x, which is in line with the broader technology sector’s average (25–30x).

- Price‑to‑Sales (P/S): About 7x, also within the normal range for growth tech firms.

- PEG Ratio: 1.6, suggesting that Apple’s earnings growth justifies a modest premium.

They emphasize that Apple’s earnings per share (EPS) growth is projected to remain at 12%–15% over the next five years. This is based on guidance from the company’s 2025 earnings report and corroborated by independent analysts’ forecasts.

4. Risks and Caveats

No investment is risk‑free, and the article lays out several downside scenarios:

- Macro‑Economic Headwinds: Rising interest rates could compress the valuation multiples for tech stocks, including Apple.

- Supply Chain Disruptions: Apple’s reliance on a global supply chain (particularly the shortage of semiconductors) may affect production timelines and costs.

- Regulatory Scrutiny: Antitrust investigations into Apple’s App Store policies could lead to higher compliance costs or reduced revenue from services.

- Competition from Emerging Platforms: Companies like Google’s “Android 14” with advanced AI features might erode Apple’s market share.

The writers link to a “Risk Management for Growth Stocks” article that outlines how to hedge against these risks, such as adding fixed‑income or commodity exposure to a portfolio that has a large Apple allocation.

5. Why Apple Is the “Single Stock” Recommendation

The authors close the article by summarizing Apple’s strengths:

- Resilient Cash Flow: Apple’s free cash flow is high enough to fund dividends and buybacks.

- Recurring Revenue: The Services segment is growing at a higher rate than hardware, providing a steady income stream.

- Strong Brand: Apple’s brand equity is arguably unmatched in consumer technology, fostering repeat customers.

- Strategic Moves: Apple’s expansion into health, streaming, and enterprise solutions positions it for multi‑sector growth.

They acknowledge that this recommendation is best suited for investors who have a long‑term horizon (10+ years) and can tolerate short‑term volatility. They encourage readers to use Apple as a core holding while still diversifying with other sectors or asset classes.

6. Additional Context from Embedded Links

The article is interwoven with internal links to other Fool research pieces that enrich the story:

- “Apple Growth Story”: Provides a deeper dive into revenue segmentation and service growth.

- “Tech Giants Showdown”: Offers a side‑by‑side comparison of Apple vs. Samsung and Google.

- “How to Evaluate a Company’s Balance Sheet”: Explains balance sheet metrics and why they matter.

- “Risk Management for Growth Stocks”: Discusses hedging strategies for a portfolio heavily weighted in growth tech.

These resources give readers a fuller picture of why Apple may be a logical core holding and how to incorporate it within a broader investment strategy.

7. Bottom Line

In summary, the Motley Fool’s article posits Apple Inc. as the optimal single stock for investors who want a “buy‑and‑hold” strategy that delivers both growth and income. By leveraging Apple’s robust cash flow, recurring services revenue, and brand strength, the authors argue that the company can continue to deliver solid returns over the long haul, even in a changing tech landscape. The piece is thorough, referencing internal data, valuation metrics, growth drivers, competitive context, and risk factors—all of which provide a solid foundation for a long‑term investment thesis.

Whether or not you agree with the recommendation, the article serves as a useful primer on how a well‑researched single‑stock pick can fit into a larger, diversified portfolio. It also underscores the importance of balancing core holdings with risk mitigation tactics, a principle that remains central to prudent investing.

Read the Full The Motley Fool Article at:

https://www.fool.com/investing/2025/12/17/if-i-could-only-buy-and-hold-a-single-stock-this/

[ Tue, Dec 16th 2025 ]: The Motley Fool

[ Mon, Dec 15th 2025 ]: The Motley Fool

[ Thu, Dec 11th 2025 ]: The Motley Fool

[ Tue, Dec 09th 2025 ]: The Motley Fool

[ Mon, Dec 08th 2025 ]: The Motley Fool

[ Mon, Dec 08th 2025 ]: The Motley Fool

[ Mon, Dec 08th 2025 ]: The Motley Fool

[ Fri, Nov 28th 2025 ]: The Motley Fool

[ Thu, Nov 27th 2025 ]: Seeking Alpha

[ Wed, Nov 26th 2025 ]: The Motley Fool

[ Sun, Nov 23rd 2025 ]: The Motley Fool

[ Sun, Nov 16th 2025 ]: The Motley Fool