[ Today @ 12:35 PM ]: WTOP News

[ Today @ 12:34 PM ]: Business Insider

[ Today @ 12:32 PM ]: KELO

[ Today @ 12:29 PM ]: Erie Times-News

[ Today @ 12:28 PM ]: Goodreturns

[ Today @ 11:06 AM ]: CNBC

[ Today @ 09:46 AM ]: American Association of Individual Investors

[ Today @ 09:19 AM ]: Tulsa World

[ Today @ 07:58 AM ]: MarketWatch

[ Today @ 05:49 AM ]: New York Post

[ Today @ 05:48 AM ]: Impacts

[ Today @ 04:55 AM ]: The Hill

[ Today @ 04:54 AM ]: wjla

[ Today @ 04:52 AM ]: Investopedia

[ Today @ 04:48 AM ]: Futurism

[ Today @ 04:44 AM ]: The Straits Times

[ Today @ 04:43 AM ]: The Center Square

[ Today @ 04:42 AM ]: Forbes

[ Today @ 04:41 AM ]: investorplace.com

[ Today @ 04:39 AM ]: Her Campus

[ Today @ 04:38 AM ]: The Virginian-Pilot

[ Today @ 04:37 AM ]: The Jerusalem Post Blogs

[ Today @ 04:36 AM ]: The Motley Fool

[ Today @ 02:42 AM ]: Seeking Alpha

[ Today @ 02:27 AM ]: Channel 3000

[ Today @ 12:22 AM ]: LiveNow Fox

[ Yesterday Evening ]: The Financial Times

[ Yesterday Evening ]: Seattle Times

[ Yesterday Evening ]: KSTP-TV

[ Yesterday Evening ]: reuters.com

[ Yesterday Evening ]: TweakTown

[ Yesterday Evening ]: WSB-TV

[ Yesterday Afternoon ]: Forbes

[ Yesterday Afternoon ]: Fox 11 News

[ Yesterday Afternoon ]: CBS News

[ Yesterday Afternoon ]: MSN

[ Yesterday Afternoon ]: Insider Monkey

[ Yesterday Morning ]: Seeking Alpha

[ Yesterday Morning ]: The Independent

[ Yesterday Morning ]: Finbold | Finance in Bold

[ Yesterday Morning ]: Fortune

[ Yesterday Morning ]: KOB 4

[ Yesterday Morning ]: The Hill

[ Yesterday Morning ]: BBC

[ Yesterday Morning ]: WPIX New York City, NY

[ Yesterday Morning ]: Impacts

[ Yesterday Morning ]: The Motley Fool

[ Yesterday Morning ]: Local 12 WKRC Cincinnati

Meta Downgraded to 'Neutral' Amidst Lingering Challenges

Locales: UNITED STATES, IRELAND

Sunday, March 22nd, 2026 - Meta Platforms (META) has enjoyed a promising start to 2026, with its stock climbing nearly 20% year-to-date. This positive trajectory was initially spurred by a surprisingly strong fourth-quarter earnings report and a shift in management's communication, highlighting progress in critical areas like Reels monetization and cost management. However, despite this apparent turnaround, analysts at [Investment Firm Name Redacted] have downgraded Meta from a 'Positive' to 'Neutral' rating, citing considerable challenges that remain largely unaddressed in the current valuation. This decision, while acknowledging recent improvements, underscores a growing sense of caution surrounding the tech giant's long-term prospects.

The Reels Revolution...Or Evolution?

For a considerable period, Meta's attempt to compete with TikTok through its Reels platform was a significant drag on investor confidence. Early iterations struggled to generate meaningful revenue, leading to concerns about wasted resources and a lack of strategic direction. Recent earnings calls, however, revealed a tangible improvement in Reels monetization. Meta has clearly begun to unlock revenue streams through advertising and other features within Reels, appeasing some investor anxieties. This success is partly attributable to a more focused strategy, prioritizing ad formats that resonate with Reels users and a more aggressive push towards creator partnerships.

However, while improved, Reels remains a fiercely competitive landscape. TikTok continues to dominate the short-form video market, and new entrants are constantly vying for attention. Maintaining momentum in Reels will require sustained innovation and a willingness to adapt quickly to changing user preferences - a costly and demanding endeavor.

The AI Arms Race: Meta Under Pressure

The burgeoning field of Artificial Intelligence (AI) presents both an opportunity and a threat to Meta. The company has invested heavily in AI research and development, aiming to integrate it across its platforms - from content recommendation algorithms to targeted advertising. This investment is crucial for maintaining user engagement and enhancing the overall platform experience.

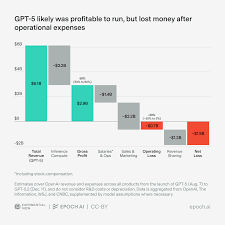

Yet, Meta faces formidable competition in the AI arena. OpenAI, with its groundbreaking GPT models, and Google, with its vast resources and established AI infrastructure, are setting a rapid pace of innovation. OpenAI's continual refinements to models like GPT-5 (launched late 2025) have significantly raised the bar, forcing Meta to accelerate its own AI efforts. The cost of staying competitive in this AI arms race is substantial, potentially impacting Meta's profit margins and requiring further significant investment.

Regulatory Storm Clouds Gathering

Beyond the competitive landscape, Meta operates under a growing cloud of regulatory scrutiny. Ongoing antitrust investigations, spearheaded by both domestic and international bodies, threaten to reshape the company's business practices. Regulators are focusing on Meta's market dominance in social media and its potential to stifle competition.

Furthermore, potential new legislation aimed at restricting data collection practices poses a significant risk. These regulations, driven by growing concerns over user privacy, could limit Meta's ability to personalize advertising and deliver targeted content - core components of its revenue model. Successfully navigating this complex regulatory environment will be a major challenge for Meta in the coming years, requiring proactive engagement with policymakers and a willingness to adapt its business practices.

Valuation: Is the Premium Justified?

While Meta's stock price has experienced a correction from its previous highs, analysts still contend that it carries a premium valuation compared to its peers. This premium reflects investor optimism regarding Meta's future growth potential, particularly in areas like the metaverse and AI. However, the downgrading analysts argue that this premium is not adequately justified given the aforementioned challenges. The risks associated with intensifying AI competition, evolving regulatory pressures, and the need for continuous innovation in a fiercely competitive market are not fully factored into the current stock price.

Looking Ahead: A Cautious Outlook

The decision to downgrade Meta to 'Neutral' is not a condemnation of the company's potential. Meta remains a powerful player in the tech industry, with a massive user base and a proven track record of innovation. However, the combination of competitive pressures, regulatory uncertainties, and valuation concerns warrants a more cautious approach. Investors should anticipate a period of heightened volatility and limited upside potential, at least in the short to medium term. The company needs to convincingly demonstrate its ability to overcome these headwinds and deliver sustainable, profitable growth before regaining a 'Positive' rating. The next few quarters will be critical in determining Meta's long-term trajectory.

Read the Full Seeking Alpha Article at:

[ https://seekingalpha.com/article/4878378-meta-time-to-sit-on-the-fence-downgrade ]

[ Last Wednesday ]: Seeking Alpha

[ Tue, Mar 10th ]: The Motley Fool

[ Thu, Mar 05th ]: Seeking Alpha

[ Sun, Mar 01st ]: IBTimes UK

[ Sun, Mar 01st ]: WTOP News

[ Fri, Feb 13th ]: The Motley Fool

[ Thu, Jan 29th ]: Investopedia

[ Tue, Jan 27th ]: The Motley Fool

[ Mon, Jan 26th ]: The Motley Fool

[ Thu, Jan 22nd ]: The Motley Fool

[ Thu, Jan 08th ]: The Motley Fool

[ Fri, Dec 05th 2025 ]: Seeking Alpha