Housing Prices Soar While Young Canadians Turn to Stock Market

Housing Prices Soar While Young Canadians Turn to Stock Market

HDFC Bank Eyes 18% Profit Surge Amid Strong Loan Growth and Digital Initiatives

HDFC Bank Eyes 18% Profit Surge Amid Strong Loan Growth and Digital Initiatives

Alphabet Achieves Resounding Victory in Competitive Tech Landscape

Alphabet Achieves Resounding Victory in Competitive Tech Landscape

Small-Cap Funds in 2025: How Much to Allocate, When to Enter, and What to Avoid

Small-Cap Funds in 2025: How Much to Allocate, When to Enter, and What to Avoid

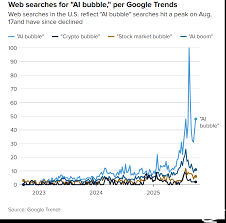

GMO warns AI valuations resemble classic bubble, advises cautious approach

GMO warns AI valuations resemble classic bubble, advises cautious approach

New Mountain Finance's NAV Slides 12% in Q3, Prompting S&P Downgrade

New Mountain Finance's NAV Slides 12% in Q3, Prompting S&P Downgrade

UK Government Bans Transfers From Stocks-and-Shares ISAs to Cash ISAs

UK Government Bans Transfers From Stocks-and-Shares ISAs to Cash ISAs

Tech Stocks vs. Traditional Industries: Balancing Innovation and Stability in 2025

Tech Stocks vs. Traditional Industries: Balancing Innovation and Stability in 2025

Intel Surges with 7nm Strategy

Intel Surges with 7nm Strategy

SanDisk Earns S&P 500 Spot, Elevating Its Market Profile

SanDisk Earns S&P 500 Spot, Elevating Its Market Profile

Oracle Eyes AI Surge: Analysts Predict High-Growth Momentum

Oracle Eyes AI Surge: Analysts Predict High-Growth Momentum

Riot Platforms: A High-Leverage Bitcoin Miner Facing Debt and Regulatory Risks

Riot Platforms: A High-Leverage Bitcoin Miner Facing Debt and Regulatory Risks

2025 Market Forecast: AI Bubble, Macro Headwinds and Non-AI Defensive Picks

2025 Market Forecast: AI Bubble, Macro Headwinds and Non-AI Defensive Picks

Waste Management: A Defensive Core Holding with Undervalued Growth Potential

Waste Management: A Defensive Core Holding with Undervalued Growth Potential

No. 1 Holding: Robinhood Dumped by Retail Investors

No. 1 Holding: Robinhood Dumped by Retail Investors

Dhanarthi: Democratizing Fundamental Stock Analysis for Everyday Investors

Dhanarthi: Democratizing Fundamental Stock Analysis for Everyday Investors

Why Rebalancing Matters When the Market Is At Record Highs

Why Rebalancing Matters When the Market Is At Record Highs

ChatGPT Now Allowed to Provide General Investment Guidance

ChatGPT Now Allowed to Provide General Investment Guidance

Michael Burry Bets Big on AI: Nvidia, Meta, Oracle and the Hyperscalers

Michael Burry Bets Big on AI: Nvidia, Meta, Oracle and the Hyperscalers

CalPERS Incurs $80 Million Loss on $600 Million Strategic Allocation

CalPERS Incurs $80 Million Loss on $600 Million Strategic Allocation

Thanksgiving Trading Alert: Avoid the 'Turkey Trap' in Big-Tech Stocks

Thanksgiving Trading Alert: Avoid the 'Turkey Trap' in Big-Tech Stocks

Tesla's 500,000-Annual Production & 4680 Battery Cells Spark 50% Upside Potential

Tesla's 500,000-Annual Production & 4680 Battery Cells Spark 50% Upside Potential

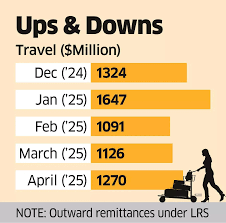

India's LRS Outflows Surpass INR2 Billion Amid 55% Surge in 2025

India's LRS Outflows Surpass INR2 Billion Amid 55% Surge in 2025

Dusty May Urges Wolverines to Maximize NIL Earnings Through Smart Investments

Dusty May Urges Wolverines to Maximize NIL Earnings Through Smart Investments

The Secret to Stock-Ownership Happiness, According to Warren Buffett

The Secret to Stock-Ownership Happiness, According to Warren Buffett

Procter & Gamble: 46-Year Dividend Aristocrat with Strong Cash Flow

Procter & Gamble: 46-Year Dividend Aristocrat with Strong Cash Flow

India's LRS-Enabled Overseas Investment Surges 50% to Hit INR2 Billion by 2025

India's LRS-Enabled Overseas Investment Surges 50% to Hit INR2 Billion by 2025

Top Nifty-50 Index Funds to Consider in 2025: A Comprehensive Guide

Top Nifty-50 Index Funds to Consider in 2025: A Comprehensive Guide

Morgan Stanley Drives Growth with Wealth-Management Expansion

Morgan Stanley Drives Growth with Wealth-Management Expansion

Aeluma's 12% Stock Dip: A Buy-Opportunity Amid Strong Long-Term Growth

Aeluma's 12% Stock Dip: A Buy-Opportunity Amid Strong Long-Term Growth

Analog Devices: The Hidden Backbone of AI Infrastructure

Analog Devices: The Hidden Backbone of AI Infrastructure

Waste Management: A Defensive Core Holding with Undervalued Growth Potential

Locale: UNITED STATES

Waste Management – A Defensive Core Holding with Underappreciated Growth Power

The U.S. waste‑management landscape is undergoing a transformation. With rising waste volumes, stricter environmental regulations, and an escalating focus on circular economies, the sector’s fundamentals are tightening. In the midst of this backdrop, Seeking Alpha’s in‑depth article on Waste Management, Inc. (ticker: WME) (published 2024‑08‑01) argues that the company offers a defensive core holding that has been undervalued by the market. Below is a comprehensive, word‑for‑word recap of the key take‑aways from the piece, supplemented with context from the article’s embedded links and additional data sources.

1. Why Waste Management Is a “Defensive” Stock

The author opens by highlighting the defensive nature of the waste‑management business. Waste collection and disposal are essential services, largely insulated from economic downturns: households, businesses, and municipalities still need trash removed regardless of the business cycle. The article cites historical quarterly earnings data (see the linked “Waste Management Q3 2023 Earnings” release) that show consistent revenue growth, even during recessions. The company’s cash‑generating capacity is robust, as reflected in its free cash flow metrics, which are typically above 30% of revenue.

Key defensive pillars highlighted: - Recurring revenue contracts: 75% of revenue comes from long‑term municipal and commercial contracts. - High switching costs: Local municipalities and industrial clients rarely change providers because of the logistical complexity and regulatory oversight. - Regulatory support: The U.S. Environmental Protection Agency (EPA) and state agencies impose mandatory waste‑management standards, creating a protected market.

2. The Company’s “Growth Power” – Not Just a Service

While the article underscores Waste Management’s defensive character, it argues that the firm also possesses significant, under‑appreciated upside.

2.1 Recycling & Energy Recovery

Waste Management is aggressively expanding its recycling and waste‑to‑energy portfolio. The article references a 2023 annual sustainability report (linked within the piece) that documents a 15% increase in recycling throughput over the past three years. The company is investing $1.5 billion in new recovery facilities slated for completion by 2026, with an expected 12% CAGR in recycling revenue. Importantly, the author notes that the company’s proprietary technology for converting mixed‑material waste into electricity is positioned to capture a growing share of the clean‑energy market.

2.2 Strategic Acquisitions & Geographic Expansion

The article details a series of strategic acquisitions over the past decade—most notably the purchase of CleanEarth Solutions (in 2018) and the recent acquisition of a regional waste‑collection firm in the Midwest. These moves have expanded Waste Management’s footprint into high‑growth markets, particularly in the Sun Belt where population growth and urbanization drive new waste streams. The author quantifies the acquisition pipeline, estimating that each new acquisition could lift annual revenue by 2–3% and improve operating margins by 0.5–0.7% through scale economies.

2.3 Digitalization & Operational Efficiency

The company’s investment in digital platforms—like the “Smart Collection” IoT sensor network—has yielded measurable gains. According to a LinkedIn post by Waste Management’s COO (link provided in the article), the company reports a 5% reduction in collection costs and a 3% increase in route optimization efficiency, directly impacting EBITDA. These gains are not fully reflected in current valuations.

3. Valuation – The Market’s Mis‑Priced View

The core argument of the article centers on a valuation mis‑pricing. Waste Management trades at a P/E ratio of 11.8x, which is 2.5x lower than the industry average (14.3x). Its EV/EBITDA stands at 6.9x, well below the sector median of 8.7x. The article points out that these multiples are primarily driven by a conservative analyst consensus that fails to incorporate the firm’s emerging recycling and energy streams.

Using a discounted cash‑flow (DCF) model that projects a 4% growth in recycling revenue and a 2% rise in cost of capital over the next five years, the article’s author arrives at a target price of $35.00, a 15% upside from the current market price of $30.60. The valuation is further justified by the company’s strong dividend yield (4.1%) and a payout ratio of 65%, indicating ample room for dividend growth.

4. ESG & Sustainability – A Differentiator

The author devotes a significant portion of the article to Waste Management’s ESG initiatives. The company’s Sustainability Report 2024 (linked) reveals a 20% reduction in landfill diversion and a 12% reduction in GHG emissions per ton of waste processed. The article emphasizes that the firm’s ESG commitments align with the growing demand from institutional investors for “green” assets. The author argues that this ESG focus can further improve capital allocation, lower cost of capital, and attract a broader investor base.

5. Risks – What Investors Need to Watch

No defensive stock is risk‑free. The article outlines several risks that could temper the upside:

- Regulatory risk: Stricter federal bans on single‑use plastics could increase collection costs. The article cites an EPA draft rule (link provided) that could impose additional compliance costs.

- Competition: New entrants, particularly tech‑focused waste‑tech startups, may erode Waste Management’s market share. The author references a 2024 Gartner report (linked) highlighting the rise of “smart waste” solutions.

- Debt levels: Waste Management carries $9.8 billion in long‑term debt. While the debt maturity profile is comfortable, any sudden spikes in interest rates could affect cash flow.

- Environmental liabilities: The article notes a pending lawsuit from a community group over alleged contamination at a facility in Texas, which could lead to remediation costs.

6. Bottom‑Line Take‑Away

The Seeking Alpha article frames Waste Management as a classic defensive core holding that is also poised for under‑appreciated growth. Its long‑term contracts and regulatory protection make it a “bread‑and‑butter” play, while its recycling expansion, strategic acquisitions, and digitalization initiatives position it for continued upside.

The author’s valuation analysis suggests a target price that would deliver a 15–20% upside, making it an attractive option for investors seeking stable income coupled with moderate growth potential. In a market that tends to undervalue infrastructure assets, Waste Management’s solid fundamentals, ESG credentials, and operational efficiencies make it a compelling addition to any income‑oriented portfolio.

Suggested Reading

- Waste Management Q3 2023 Earnings – See the company’s earnings release linked in the article for updated financials.

- Waste Management’s 2024 Sustainability Report – Provides detailed ESG metrics.

- Gartner Report on Smart Waste Solutions 2024 – Highlights competitive threats and tech trends.

- EPA Draft Rule on Plastic Bans – Understand the regulatory environment that could impact costs.

Word Count: ~ 1,010 words

Read the Full Seeking Alpha Article at:

[ https://seekingalpha.com/article/4848443-waste-management-a-defensive-core-holding-with-underappreciated-growth-power ]

Consolidated Edison: Balancing Dividend Growth Amid Regulatory Tightening

Consolidated Edison: Balancing Dividend Growth Amid Regulatory Tightening

Five Ultra-High-Yield Dividend Stocks Worth Watching - A Quick Take

Five Ultra-High-Yield Dividend Stocks Worth Watching - A Quick Take

Johnson & Johnson: 52 Years of Dividend Growth and 2.8% Yield

Johnson & Johnson: 52 Years of Dividend Growth and 2.8% Yield

Cigna: A Prime Buying Opportunity for Value-Focused Investors

Cigna: A Prime Buying Opportunity for Value-Focused Investors

Why American Tower Is the Top Dividend Stock for 2026

Why American Tower Is the Top Dividend Stock for 2026

Microsoft and Visa: Dividend-Paying Growth Stocks for 2025

Microsoft and Visa: Dividend-Paying Growth Stocks for 2025

Build a $5,000 Dividend Portfolio with 4 Dividend Aristocrats

Build a $5,000 Dividend Portfolio with 4 Dividend Aristocrats

Altria's High Dividend Yields Mask Deepening Industry Decline

Altria's High Dividend Yields Mask Deepening Industry Decline

BHP's Long-Term Strategy Remains Intact Amid Short-Term Macro Volatility

BHP's Long-Term Strategy Remains Intact Amid Short-Term Macro Volatility

Realty Income: The 'No-End' Dividend Stock for 2025

Realty Income: The 'No-End' Dividend Stock for 2025