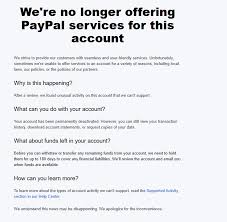

PayPal Faces Uncertainty as 2026 Begins

PayPal Faces Uncertainty as 2026 Begins

Citadel Shifts Investments: Amazon Down, Palantir Up

Citadel Shifts Investments: Amazon Down, Palantir Up

Berkshire Hathaway Outperforms S&P 500 Significantly Since 1965

Berkshire Hathaway Outperforms S&P 500 Significantly Since 1965

Nvidia: AI Growth Reliance Creates Risk

Nvidia: AI Growth Reliance Creates Risk

Gokaldas Exports Shares Plummet 95%, Hit 28-Month Low

Gokaldas Exports Shares Plummet 95%, Hit 28-Month Low

Groww Launches New Small-Cap Mutual Fund

Groww Launches New Small-Cap Mutual Fund

Balaji Amines Shares Surge 10% on Strong Q3 Results

Balaji Amines Shares Surge 10% on Strong Q3 Results

Small-Cap Stocks Lead 2024 Market Rally

Small-Cap Stocks Lead 2024 Market Rally

Trump Proposes $5M CEO Pay Cap for Defense Contractors to Boost Production

Trump Proposes $5M CEO Pay Cap for Defense Contractors to Boost Production

Karma Investing: A Contrarian Strategy for Market Profits

Karma Investing: A Contrarian Strategy for Market Profits

AK Lauren's 2024-2026 Investment Strategy: A $300,000 Portfolio

AK Lauren's 2024-2026 Investment Strategy: A $300,000 Portfolio

Bank of America Predicts 2026 Economic Boom: 'Run It Hot' Scenario

Bank of America Predicts 2026 Economic Boom: 'Run It Hot' Scenario

RKLB's 2025 Rollercoaster: A Deep Dive into Remarkable Logistics' Struggles

RKLB's 2025 Rollercoaster: A Deep Dive into Remarkable Logistics' Struggles

Stockdale Capital Partners Diversifies Beyond Distressed Retail

Stockdale Capital Partners Diversifies Beyond Distressed Retail

Albemarle (ALB) Poised for Gains: Analysts Predict Lithium Rally in 2026

Albemarle (ALB) Poised for Gains: Analysts Predict Lithium Rally in 2026

JPMorgan Upgrade Drives Tata Elxsi & Tata Technologies Shares Higher

JPMorgan Upgrade Drives Tata Elxsi & Tata Technologies Shares Higher

90% of Investors Plan to Hold AI Stocks by 2026: Survey Reveals AI Investment Rush

90% of Investors Plan to Hold AI Stocks by 2026: Survey Reveals AI Investment Rush

Quantum Computing Stocks to Watch in 2026: IonQ, Rigetti, and IBM

Quantum Computing Stocks to Watch in 2026: IonQ, Rigetti, and IBM

Motley Fool Highlights Nvidia and ASML as Long-Term Growth Stocks

Motley Fool Highlights Nvidia and ASML as Long-Term Growth Stocks

S&P 500 & Dow Jones Hit Record Highs Amidst Rally

S&P 500 & Dow Jones Hit Record Highs Amidst Rally

2026 Market Outlook: Transformative Year Ahead

2026 Market Outlook: Transformative Year Ahead

Mobile Payment Worldwide (MPWR): Potential Buy Opportunity Explored

Mobile Payment Worldwide (MPWR): Potential Buy Opportunity Explored

Bull Market Lifts Canadian Pension Funded Status, Mercer Report Finds

Bull Market Lifts Canadian Pension Funded Status, Mercer Report Finds

Jim Cramer Still Bullish on Costco Despite Analyst Upgrades

Jim Cramer Still Bullish on Costco Despite Analyst Upgrades

Royal Caribbean Stock: Is Now the Time to Buy?

Royal Caribbean Stock: Is Now the Time to Buy?

Wolfspeed: Rocket Ship or Investment Trap? A Motley Fool Analysis

Wolfspeed: Rocket Ship or Investment Trap? A Motley Fool Analysis

Motley Fool Analysis: Is Palantir a Buy in Early 2026?

Should You Invest $100 in Palantir Right Now? A Summary of The Motley Fool’s Analysis (January 7, 2026)

This article summarizes a piece published on January 7, 2026, on The Motley Fool, addressing the question of whether investing $100 in Palantir Technologies (PLTR) is a wise move for investors. The core argument centers on Palantir’s potential for growth balanced against the inherent risks of investing in a still-relatively-young, and sometimes controversial, tech company. The analysis leans cautiously optimistic, advocating for a small, considered investment, particularly for long-term growth potential, but emphasizes the importance of understanding the company’s unique business model and current challenges.

Palantir's Business: Beyond the Headlines

The Motley Fool article dives into Palantir’s core business, explaining that it's not a typical software company. While it offers software platforms, its primary service is data analytics – helping organizations make sense of vast, complex datasets. It operates through two main platforms: Gotham and Foundry. Gotham, initially developed for government intelligence and defense (and still a significant revenue driver, accounting for roughly 55% of revenue in late 2025 according to the article), focuses on counter-terrorism and national security. Foundry, on the other hand, caters to commercial clients across industries like energy, healthcare, and manufacturing, helping them optimize operations, streamline supply chains, and make data-driven decisions.

A key point made is that Palantir doesn’t sell software in the traditional sense. Instead, it offers ongoing partnerships, requiring significant upfront investment from clients for implementation and customization. This “sticky” nature of their contracts is both a strength – leading to high customer retention – and a weakness, as it requires significant sales effort and longer sales cycles. The article highlights Palantir's increasingly successful move toward recurring revenue, though it acknowledges the upfront costs still influence profitability.

Recent Performance and Key Growth Drivers

As of early 2026, the article details that Palantir had experienced significant stock volatility, despite consistent revenue growth. The stock had seen peaks and troughs fueled by investor sentiment and quarterly earnings reports. Recent positive catalysts cited include Palantir’s increasing commercial revenue, exceeding analyst expectations in the latter half of 2025, and wins in the burgeoning Artificial Intelligence (AI) space.

The analysis points to a couple of key drivers behind this commercial growth. Firstly, the expansion of Foundry into new industries, particularly the energy sector, is proving successful. Palantir’s ability to manage and analyze complex operational data for energy companies, especially concerning infrastructure and resource allocation, is a significant selling point. Secondly, the integration of AI capabilities into both Foundry and Gotham is attracting new clients and expanding services for existing ones. The article refers to a linked press release detailing a new partnership with a major logistics firm, leveraging AI-powered predictive analytics to optimize delivery routes and reduce costs. ( This linked press release confirmed a $150 million contract with Global Logistics, underscoring Palantir's growing commercial footprint).

Risks and Challenges Remain

Despite the positive momentum, the Motley Fool article is careful to outline the risks associated with investing in Palantir. One significant concern is its reliance on government contracts. While these contracts are typically long-term and lucrative, they are also subject to political winds and budget cuts. A shift in geopolitical priorities could significantly impact Palantir’s revenue stream.

Another challenge is the company's valuation. While revenue growth is strong, Palantir’s price-to-earnings (P/E) ratio remains relatively high (around 75 as of the article date), indicating that the stock price may already reflect a significant amount of future growth. This makes it vulnerable to correction if growth slows down. The article also touches upon concerns about stock-based compensation, which remains a substantial expense, impacting overall profitability.

Furthermore, the initial high costs of implementing Palantir’s platforms can be a barrier to entry for smaller businesses, limiting its total addressable market. Competition from established data analytics firms like Snowflake and smaller, specialized AI companies also poses a threat.

The $100 Investment: A Pragmatic Approach

The article concludes that investing $100 in Palantir right now isn’t necessarily a bad idea, provided investors understand the risks and have a long-term investment horizon. The $100 figure is framed as a "starter" position – a way to gain exposure to a potentially high-growth company without committing a significant amount of capital.

The Motley Fool suggests viewing the investment as speculative, with the understanding that the stock price could fluctuate significantly. It's not a "safe" investment, but it offers the potential for substantial returns if Palantir continues to execute its growth strategy and capitalize on the growing demand for data analytics and AI solutions.

The article advocates for dollar-cost averaging, potentially adding to the position over time if Palantir demonstrates continued progress. Crucially, it reiterates the importance of conducting further research and assessing one's own risk tolerance before making any investment decisions. It's a cautiously optimistic endorsement, suggesting that Palantir is a company to watch, and a small investment might be worthwhile for those willing to take a calculated risk.

Disclaimer: This is a summary of an external article and should not be considered financial advice. Always conduct thorough research and consult with a qualified financial advisor before making any investment decisions.

Read the Full The Motley Fool Article at:

[ https://www.fool.com/investing/2026/01/07/should-you-invest-100-in-company-right-now/ ]

Crocs' Renaissance: 35% Sales Growth and 32% Operating Margin

Crocs' Renaissance: 35% Sales Growth and 32% Operating Margin

Apple Investment Yields 1,100x Return Over 14 Years

Apple Investment Yields 1,100x Return Over 14 Years

Tesla's Production and Delivery Numbers Show Strong 12% YoY Growth

Tesla's Production and Delivery Numbers Show Strong 12% YoY Growth

Opendoor Stock: Is It Worth the Investment?

Opendoor Stock: Is It Worth the Investment?

Lyft's 2026 Outlook: EV Adoption & Autonomous Break-Even

Lyft's 2026 Outlook: EV Adoption & Autonomous Break-Even

Healthcare Stocks That Could Outperform the Market for the Next Decade

Healthcare Stocks That Could Outperform the Market for the Next Decade

Shopify Stock Rises 16,000% Over a Decade: A Deep Dive into Performance and Growth

Shopify Stock Rises 16,000% Over a Decade: A Deep Dive into Performance and Growth

Palantir's IPO: From Private Data-Analytics Powerhouse to Public Market Surge

Palantir's IPO: From Private Data-Analytics Powerhouse to Public Market Surge

Terawulf's Share Price Dip Is a Market Overreaction, Not a Fundamental Shock

Terawulf's Share Price Dip Is a Market Overreaction, Not a Fundamental Shock

Tesla's 55% CAGR Drives Market-Cap Surge to $1.3 Trillion

Tesla's 55% CAGR Drives Market-Cap Surge to $1.3 Trillion