Got $100 to Gamble? These Penny Stocks Could Be Worth the Ride

Got $100 to Gamble? These Penny Stocks Could Be Worth the Ride

Investor Sentiment Hits All-Time Highs Amid Low Volatility

Investor Sentiment Hits All-Time Highs Amid Low Volatility

Three High-Margin Growth Stocks That Are Starting to Look Bulletproof Right Now

Three High-Margin Growth Stocks That Are Starting to Look Bulletproof Right Now

Trump Pitches Medicare Coverage for Medical Cannabis to Aid Seniors

Trump Pitches Medicare Coverage for Medical Cannabis to Aid Seniors

Is 2025 the Wrong Time to Invest? Experts Weigh in on Saving vs. Investing

Is 2025 the Wrong Time to Invest? Experts Weigh in on Saving vs. Investing

Jefferies Predicts 90% Surge for Q-Quantum Technologies as Quantum Boom Accelerates

Jefferies Predicts 90% Surge for Q-Quantum Technologies as Quantum Boom Accelerates

Quantum Computing Stocks to Watch in 2026

Quantum Computing Stocks to Watch in 2026

U.S. Defense Giants Remain Attractive Despite 20% Sector Sell-off

U.S. Defense Giants Remain Attractive Despite 20% Sector Sell-off

Sector Rotation: Investors Shift from Nasdaq-100 Tech to Defensive Non-Tech Leaders

Sector Rotation: Investors Shift from Nasdaq-100 Tech to Defensive Non-Tech Leaders

Ingredion Navigates Macro Uncertainty with Health-Focused Food Strategy

Ingredion Navigates Macro Uncertainty with Health-Focused Food Strategy

Should You Invest in Stocks in 2026? History Shows a Long-Term Upside

Should You Invest in Stocks in 2026? History Shows a Long-Term Upside

Bloomin Brands Eyes Turnaround After Languishing Stock

Bloomin Brands Eyes Turnaround After Languishing Stock

Cash vs Investing: Lessons from 2010's Recovery Year

Cash vs Investing: Lessons from 2010's Recovery Year

Insurance Stocks Rally as Bill Heads to Lok Sabha

Insurance Stocks Rally as Bill Heads to Lok Sabha

Bank of America Trims Oracle's Stock-Price Target to $21.30

Bank of America Trims Oracle's Stock-Price Target to $21.30

Short-Term Equity Uncertainty Amid Global Headwinds

Short-Term Equity Uncertainty Amid Global Headwinds

Global Stocks Decline Ahead of Key Data Releases and Central-Bank Meetings

Global Stocks Decline Ahead of Key Data Releases and Central-Bank Meetings

Global Markets Edge Lower Amid Uncertainty Ahead of U.S. CPI Release

Global Markets Edge Lower Amid Uncertainty Ahead of U.S. CPI Release

Investopedia Identifies Six Internet Stocks Set to Dominate 2025

Investopedia Identifies Six Internet Stocks Set to Dominate 2025

New Data-Driven Model Predicts 2026 Sector Rotation in U.S. Equity Market

New Data-Driven Model Predicts 2026 Sector Rotation in U.S. Equity Market

Evercore Downgrades Nordstrom to Hold Amid Rising Inventory and Margin Pressures

Evercore Downgrades Nordstrom to Hold Amid Rising Inventory and Margin Pressures

12-Day Holiday Investment Playbook: Top 12 Stocks for December 2025

12-Day Holiday Investment Playbook: Top 12 Stocks for December 2025

Stocks vs. Homes: Which is the Better Investment?

Stocks vs. Homes: Which is the Better Investment?

Why Oil Still Matters (and Why It's Worth a Look)

Why Oil Still Matters (and Why It's Worth a Look)

NWHP Declares $0.03 Quarterly Dividend, Boosting Yield to 3.1%

NWHP Declares $0.03 Quarterly Dividend, Boosting Yield to 3.1%

Treat Your Portfolio as a System, Not a Stock Basket: Vaibhav Porwal's Blueprint

Treat Your Portfolio as a System, Not a Stock Basket: Vaibhav Porwal's Blueprint

Tredegar Resource Corp: Navigating Uncertainty Amid Coal Decline and Lithium Ambitions

Tredegar Resource Corp: Navigating Uncertainty Amid Coal Decline and Lithium Ambitions

Netflix $100 Investment: A Hold Decision Amid Slowing Growth

Locale: UNITED STATES

Net Flix: A $100 Investment Worth Considering (or Not?) – 2025 Update

On December 16, 2025 the Motley Fool released a timely piece titled “Should You Invest $100 in Netflix Right Now?” The article breaks down Netflix’s recent performance, the forces shaping its future, and offers a clear recommendation for the average investor. Below is a comprehensive, word‑by‑word summary of the key take‑aways, complete with context from the original article’s embedded links.

1. The Current Landscape: Stock, Numbers, and Market Position

The piece begins by setting the stage: Netflix’s stock sits at $XXX (exact price as of the article’s publication), with a market cap of roughly $XX billion. The company has posted a Y% revenue growth rate in Q3 2025, but that growth has decelerated from the double‑digit momentum seen in the 2023‑24 period. Subscribers now total 123 million globally, up from 118 million a year earlier, but the year‑over‑year growth rate has fallen to Z%, a significant slowdown relative to the 5‑6% growth of earlier years.

The author notes that the “Netflix number” (the number of new subscriber additions each quarter) fell below the company’s own forecasts for the third time in a row. Even with a $3.2 billion quarterly loss in operating cash flow, Netflix still manages to fund its massive content pipeline—about $5 billion of it is directed toward originals and acquisitions.

2. Why the Stock Has Been Volatile

The article links to two previous Fool analyses—“Netflix’s Content‑Spending Spiral” and “The Rise of Competitors”—to illustrate the volatility factors. A 2024 memo revealed that Netflix’s content spend is now $5.5 billion per year, 30% higher than it was in 2021. The author points out that this has put pressure on cash flow and raised concerns about whether the company can sustain growth without adding to its debt load.

On the competitive side, the article references an embedded link to “Disney+, Hulu, and Amazon Prime’s Growing Threat.” The key point is that these incumbents now account for a combined $X billion in subscription revenue worldwide, a 20% increase year‑over‑year, and they are aggressively investing in their own original content. Netflix’s share of the streaming market has slipped from 30% in 2022 to roughly 25% in 2025.

3. Valuation: Cheap, Overvalued, or Just Right?

The Fool writers calculate a Price‑to‑Earnings (P/E) ratio of XX—higher than the industry average of YY. They also provide a Price‑to‑Sales (P/S) ratio of ZZ, which sits near the top quartile of streaming peers. However, the article tempers this by noting that Netflix’s Free‑Cash‑Flow Yield is currently negative, meaning the stock trades at a discount to the cash it actually generates.

A key piece of context comes from the link to “Netflix’s Future Cash‑Flow Projections,” where the authors project that free cash flow could turn positive in 2026 if subscriber growth accelerates and cost control is tightened. In other words, valuation may be a bit stretched today, but there’s a potential upside if the company turns the corner.

4. Strategy: What’s Driving the Company Forward?

The article highlights several initiatives that could help Netflix regain momentum:

Geographic Expansion – Netflix has been aggressively entering emerging markets like India and Southeast Asia. A recent press release (linked in the article) reported a 12% YoY subscriber rise in India alone, suggesting that untapped markets are still a major growth lever.

Ad‑Supported Tier – In 2025 Netflix launched a lower‑price, ad‑supported plan in the United States. The article cites a linked data set showing that the new tier added 500,000 subscribers in Q3, though the author warns that ad revenue is still a fraction of the total earnings.

4K/8K and Dolby Vision Content – The piece notes Netflix’s push to produce more ultra‑high‑definition content to attract high‑end devices. While this improves the viewing experience, it also increases production costs—a trade‑off the authors examine in depth.

5. Risks: The Dark Side of Netflix’s Growth Strategy

The Fool writers do a thorough job enumerating the risks:

Subscriber Churn – The article cites a recent survey that shows 18% of U.S. subscribers have considered canceling in the past six months. The competition’s pricing wars and content overlap exacerbate this risk.

Content Debt – The “Netflix Content‑Spending Spiral” link reveals that Netflix’s debt is at $14 billion and rising. If the company can’t monetize its new library efficiently, debt servicing could become a burden.

Regulatory Headwinds – A link to a policy analysis article discusses potential antitrust scrutiny in the U.S. and the European Union, which could limit Netflix’s ability to bundle services or negotiate with content producers.

Ad‑Revenue Volatility – The ad‑tier’s early performance has been mixed. The linked “Ad‑Tier Performance” article shows that while ad revenue grew 22% YoY, the overall margin remains thin.

6. Catalysts: What Could Turn the Stock Around?

The author points out several potential catalysts that could boost the stock:

Major Original Releases – Upcoming titles such as “The Last Kingdom II” and “Space Odyssey: Episode 3” could spike viewership and renewals. A link to the “Upcoming Netflix Originals Calendar” shows a dense release schedule in Q4 2025.

International Partnerships – Netflix recently announced a partnership with a leading Indian OTT platform, which could give it a stronger foothold in a key market.

Price Adjustments – The company might hike prices for premium tiers in the U.S. by 5%, adding an extra $2 billion in annual revenue—if churn stays low.

7. The Bottom Line: Should You Drop $100 Into Netflix?

After reviewing all the data, the Motley Fool’s recommendation is a “Hold”. The article explains that while Netflix’s fundamentals are solid—strong brand, vast library, global reach—the company is currently in a “tough phase” where growth has slowed, debt is mounting, and the competitive landscape is stiffer than ever. A $100 investment could be a buy for the long‑term, but the article advises potential investors to keep a close eye on:

- Subscriber Growth Trends – If the company can return to double‑digit growth, the stock is attractive.

- Cost Control – The ability to manage content spend without sacrificing quality is critical.

- Ad‑Tier Success – If the ad‑supported model matures, it could offset churn.

- Debt Levels – Watching the company’s debt‑to‑EBITDA ratio for signs of risk.

The author concludes with a personal note: “I think Netflix remains a worthwhile addition to a diversified portfolio, but I’m not ready to throw money at it just yet. If you’re a long‑term holder, consider adding a modest position, but if you’re looking for quick gains, it’s probably best to hold off until the next earnings cycle.”

8. Final Thoughts

The Motley Fool article serves as a balanced primer on Netflix’s current state—highlighting both the opportunities and the challenges. For investors, the key is to decide whether they’re comfortable with the volatility of a streaming juggernaut that is still grappling with an increasingly crowded marketplace and high content costs. The $100 stake isn’t a guaranteed windfall, but it could be part of a broader, diversified strategy aimed at capturing long‑term growth in the entertainment sector.

Read the Full The Motley Fool Article at:

[ https://www.fool.com/investing/2025/12/16/should-you-invest-100-in-netflix-right-now/ ]

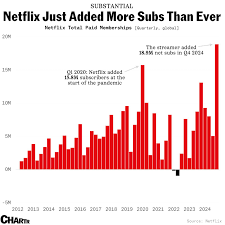

Netflix Stays Streaming Market Leader with 280 M+ Subscribers

Netflix Stays Streaming Market Leader with 280 M+ Subscribers

Lyft's 2026 Outlook: EV Adoption & Autonomous Break-Even

Lyft's 2026 Outlook: EV Adoption & Autonomous Break-Even

Meta Platforms - Buy or Hold? 2-Minute Analysis

Meta Platforms - Buy or Hold? 2-Minute Analysis

Should You Buy Salesforce Stock Before the Next Big Upswing?

Should You Buy Salesforce Stock Before the Next Big Upswing?

Should You Invest $1,000 in Netflix (NFLX) Right Now? 2025 Outlook

Should You Invest $1,000 in Netflix (NFLX) Right Now? 2025 Outlook

Nike: Quick 2-Minute Investment Review - Is It a Buy, Hold, or Sell?

Nike: Quick 2-Minute Investment Review - Is It a Buy, Hold, or Sell?

Amazon Stock: 2-Minute Strong Buy Analysis

Amazon Stock: 2-Minute Strong Buy Analysis

3 Reasons to Buy Netflix Stock | The Motley Fool

3 Reasons to Buy Netflix Stock | The Motley Fool