Receives IBD Rating Upgrade, Signaling Confidence")

")

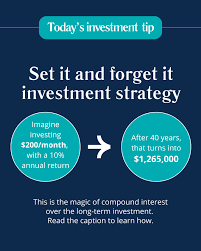

Automation: A Starting Point, Not a 'Set It and Forget It' Solution

The Globe and Mail

The Globe and MailLocale: CANADA

The Automation Foundation: More Than Just Set-and-Forget

The article rightly identifies automation as a cornerstone. The inertia that prevents many from investing isn't a lack of willingness, but a psychological barrier rooted in perceived effort. Automating monthly transfers from a checking account to various investment vehicles--TFSA, RRSP, or taxable accounts--effectively removes that barrier. However, automation shouldn't be viewed as a purely 'set it and forget it' solution. It's the starting point. Simply scheduling transfers isn't enough. The amount transferred needs to be realistic and sustainable. Starting small is excellent advice, but that initial amount should be consciously chosen, perhaps as a percentage of income, ensuring it scales with earnings.

Furthermore, consider where the automated funds are directed. A diversified portfolio, even with automated contributions, requires thought. Are funds being allocated appropriately across different asset classes? Is the automation set up to prioritize tax-advantaged accounts before taxable ones? Automation removes the 'what' of when to invest, but leaves the 'what' of where to invest still requiring active decision-making.

Regular Portfolio Reviews: Digging Deeper Than Performance Numbers

Quarterly portfolio reviews are critical, but simply observing performance metrics isn't sufficient. The article suggests focusing on whether you're "on track" - but what does that mean? This requires clearly defined financial goals. Are you saving for retirement, a down payment on a house, a child's education, or another specific purpose? The review should assess performance relative to those goals.

Beyond raw returns, consider factors like expense ratios, tax efficiency, and the overall risk profile of the portfolio. Are you truly comfortable with the level of risk you're taking? A deeper dive involves analyzing individual holdings. Have any positions significantly underperformed? Are there any overlapping investments creating unintended concentration risk? These insights inform rebalancing decisions, discussed below.

Rebalancing: A Disciplined Approach to Risk Management

Rebalancing isn't merely about selling high and buying low; it's a core risk management strategy. As the article explains, different asset classes perform differently over time, causing the initial asset allocation to drift. However, the frequency of rebalancing is also important. While annual rebalancing is common, some investors opt for threshold-based rebalancing - intervening when an asset class deviates a certain percentage from its target.

Rebalancing isn't cost-free, and frequent trading can erode returns. Therefore, a strategic approach is crucial. Consider the tax implications of selling appreciated assets in a taxable account. Tax-loss harvesting, selling losing investments to offset capital gains, can be integrated into the rebalancing process, further enhancing tax efficiency.

Strategic Adjustments: Adapting to Life's Evolving Landscape

The final step - adjusting your strategy periodically - acknowledges that financial planning isn't static. Life changes like marriage, the birth of a child, a job change, or nearing retirement necessitate a reassessment of financial goals and risk tolerance. Market conditions also play a role. While avoiding reactive, short-term adjustments is wise, ignoring fundamental shifts in the economic landscape would be a mistake.

This periodic review should involve a holistic look at your financial situation, including debt levels, income, expenses, and other assets. Are you on track to meet your long-term goals given your current trajectory? Do you need to increase your savings rate, adjust your asset allocation, or consider alternative investment strategies? Consulting with a financial advisor can provide valuable objective insights during this process.

Ultimately, building a better investing routine is about more than just automating transfers and reviewing performance. It's about cultivating a mindful, disciplined, and adaptable approach to wealth building--one that aligns with your individual goals, risk tolerance, and life circumstances. It requires a commitment to continuous learning and a willingness to make adjustments as needed.

Read the Full The Globe and Mail Article at:

https://www.theglobeandmail.com/investing/adv/article-build-a-better-investing-routine-with-these-four-steps/

on: Sun, Jan 11th

by: The Motley Fool

on: Sun, Jan 11th

by: The Globe and Mail

on: Fri, Feb 13th

by: The Motley Fool

on: Thu, Feb 05th

by: MarketWatch

Stock Market Ascent: Experts Warn of Common Investment Mistakes

on: Wed, Jan 28th

by: Seeking Alpha

on: Sat, Jan 24th

by: Nasdaq

on: Wed, Jan 21st

by: The Motley Fool

on: Sun, Jan 18th

by: USA Today

on: Mon, Jan 12th

by: The Motley Fool

on: Sat, Jan 10th

by: The Motley Fool

on: Thu, Nov 20th 2025

by: Let's Talk Money! with Joseph Hogue, CFA

on: Tue, Feb 17th

by: WTOP News