by: Business Today

Tata AIA Launches MultiCap Opportunities Fund with Free Life-Insurance Cover for the First Year

: High-Growth Tech Powerhouse Gift")

by: Forbes

Santa-Claus Rally 2025: Wall Street's Holiday Cheer or the Grinch's Gains-Stealing Antics?

by: The Motley Fool

Nu Holdings Leads Brazil's Digital-Banking Revolution with 35% YoY Customer Growth

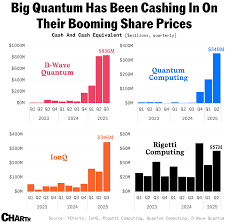

Investing in Quantum Computing: A 2025 Snapshot of Three Promising Stocks

The Motley Fool

The Motley FoolLocale: UNITED STATES

Investing in Quantum Computing: A 2025 Snapshot of Three Promising Stocks

Quantum computing is the technology that could, in theory, solve problems that are currently intractable for even the most powerful super‑computers. By exploiting phenomena such as superposition, entanglement, and tunneling, quantum machines can process a vast number of possible solutions simultaneously. This means that in the future we might see breakthroughs in cryptography, materials science, drug discovery, and complex optimization problems that impact logistics, finance, and energy. However, the industry remains in its infancy—quantum processors are still delicate, error‑rates are high, and the economic path to practical devices is unclear. The Motley Fool article “Want to invest in quantum computing? 3 stocks to buy” tackles this uncertainty head‑on, breaking the topic into three clear segments: why quantum matters, what the major players are, and how to weigh the risk versus reward for investors.

1. Why Quantum Computing Should Be on Your Radar

The piece opens by contrasting the current state of classical computing (the transistor‑based chips that dominate our laptops, phones, and data centers) with the emerging quantum paradigm. While Moore’s Law has slowed, the possibility of quantum advantage—where a quantum computer can outperform classical systems on certain tasks—offers a compelling long‑term narrative. The article points out that major tech firms are already investing billions in quantum research and that governments worldwide are pledging funding, signaling a macro‑trend that could shape the next decade of technology.

It also candidly notes the hurdles: quantum hardware is fragile, requires cryogenic temperatures, and suffers from decoherence. Even if breakthroughs arrive, the “software ecosystem” and talent pipeline lag behind. These practical challenges mean that any quantum‑focused investment is a long‑term play—one that may need to weather periods of under‑performance before the technology matures.

2. The Three Stocks: IBM, Honeywell, and Intel

The core of the article is a concise analysis of three publicly traded companies that are heavily involved in quantum computing. Each is chosen for a different reason—market position, innovation pipeline, and balance of risk and upside.

| Company | Why It’s In the Mix | Key Quantum Activities | Stock Snapshot |

|---|---|---|---|

| IBM (IBM) | Long‑standing leader, strong quantum ecosystem | • Qiskit open‑source SDK • IBM Quantum Network (cloud‑based access) • Roadmap toward “quantum advantage” in the next 5‑10 years | Large‑cap; historically stable; current valuation offers upside if quantum services grow. |

| Honeywell (HON) | New quantum division spun off as Honeywell Quantum Solutions (HQS) | • Trapped‑ion qubits (HQS)\n• Partnerships with Amazon Braket and Microsoft Azure\n• Quantum‑ready supply chain | Mid‑cap; high volatility but strong growth trajectory; HQS revenue growing fast. |

| Intel (INTC) | Silicon‑based spin‑qubits research; integrated classical‑quantum chip strategy | • Spin‑qubit platform on 7‑nm process • Joint ventures with startup Quantum Motion (for hardware) • Long‑term goal of quantum‑classical co‑processing | Large‑cap; stable; quantum research is a small portion of total spend but could become significant. |

IBM is the most obvious choice, given its decade‑long public presence in the quantum arena and its well‑established Qiskit community. The company’s quantum hardware and cloud services already generate recurring revenue, and analysts project a modest but steady increase as the quantum ecosystem matures.

Honeywell is a newer entrant but benefits from a focused quantum division and a business model that leverages its broader industrial and aerospace expertise. HQS’s partnership with major cloud providers (Amazon Braket, Microsoft Azure) gives it immediate market reach, while the company’s own R&D pipeline—particularly trapped‑ion technology—positions it as a high‑growth, albeit higher‑risk, play.

Intel is less flashy in terms of current quantum revenue, but its core competence in silicon fabrication gives it a plausible pathway to integrate quantum processors with classical systems. The company’s collaboration with startup Quantum Motion to build scalable spin‑qubit arrays is a key highlight. For investors who want the safety of a blue‑chip with a quantum bet, Intel offers that balance.

3. What the Numbers Say

The article pulls together a few key financial metrics that illustrate the potential upside and the risk profile of each stock:

IBM: Revenue from quantum services is still a tiny fraction (~1–2%) of total sales, but it’s growing at ~20% YoY. The company’s P/E ratio is around 15‑18, making it relatively cheap for a tech leader. Analysts foresee a 5‑10% upside over the next 5 years if quantum services expand.

Honeywell: Quantum‑related revenue is under 0.5% of total sales, but it’s accelerating at >30% YoY. The company’s enterprise valuation is in the 30‑35 range, indicating room for growth. However, the stock’s beta is high, and its earnings can be volatile due to the small base of quantum revenue.

Intel: Quantum research spend is roughly 0.3% of total R&D, but Intel’s large cash reserves allow it to maintain a steady investment pipeline. Its stock has a P/E of ~20, and the company’s beta is moderate. The upside is more conservative compared to Honeywell but supported by Intel’s broad market moat.

4. Risks and How to Mitigate Them

The article emphasizes three primary risk categories:

Technology Risk – Quantum hardware still has high error rates, and it is uncertain when or if a commercial quantum advantage will materialize. Mitigation: Choose a mix of companies with diverse approaches (hardware, software, ecosystem) so that failure of one technology does not wipe out the entire exposure.

Market Adoption Risk – Even if quantum computers become viable, the speed at which industry sectors (finance, pharmaceuticals, logistics) adopt them will determine the financial upside. Mitigation: Invest in companies that also have strong traditional business lines (IBM’s enterprise services, Intel’s CPUs, Honeywell’s aerospace contracts) so that the portfolio remains resilient if quantum adoption lags.

Competitive Risk – Startups such as IonQ, Rigetti, and QCI are aggressively pursuing quantum hardware, and larger tech firms could pivot to their own quantum strategies at any time. Mitigation: Keep a small quantum exposure (10–15% of a technology‑heavy portfolio) and re‑balance periodically.

5. Bottom Line: A Long‑Term, Diversified Bet

The Motley Fool article concludes that quantum computing is a “late‑stage frontier” technology, meaning it is not yet a mainstream commodity but holds the potential for significant upside in the 10‑20 year horizon. By allocating a modest portion of a diversified portfolio to one or more of the three companies highlighted—IBM, Honeywell, and Intel—investors can gain exposure to the quantum race without overcommitting. The recommended strategy is to:

- Start small – 5–10% of a tech‑heavy portfolio, or a few thousand dollars in a quantum‑focused ETF if available.

- Monitor – Watch quarterly earnings for quantum‑related revenue and press releases for breakthroughs.

- Re‑balance – Shift focus toward the company that demonstrates the strongest execution or technological lead over time.

In essence, the article encourages a patient, research‑driven approach to quantum investing: understand the science, keep an eye on financials, and stay disciplined amid a field that is still maturing. If you’re willing to wait for the quantum advantage to materialize, investing in IBM, Honeywell, and Intel now could pay dividends when the next wave of computational power hits the market.

Read the Full The Motley Fool Article at:

https://www.fool.com/investing/2025/12/21/want-to-invest-in-quantum-computing-3-stocks-that/

Like: 👍

on: Tue, Dec 16th 2025

by: MarketWatch

Quantum Computing Gets a Big-Name Backing - What It Means for Investors

on: Tue, Dec 09th 2025

by: The Motley Fool

Quantum Computing Is No Longer a Buzzword: Investors Should Watch These 3 Companies

on: Sat, Nov 22nd 2025

by: The Motley Fool

Quantum Computing Patents: The New Economic Moats of the Industry

on: Sat, Nov 29th 2025

by: The Motley Fool

Buffett's Quantum Surprise: Why IBM and Qualcomm Are Now In the Spotlight

on: Thu, Nov 06th 2025

by: Investopedia

Here's How Hot Quantum Stocks Have Been Lately--And What to Know About Them

on: Sun, Dec 07th 2025

by: The Motley Fool

Quantum Computing Stocks: 2025 Snapshot - What to Expect in One Year

on: Thu, Dec 11th 2025

by: The Motley Fool

Quantum Computing Stocks Set for 2026 Surge, Motley Fool Says

on: Mon, Nov 17th 2025

by: The Motley Fool

Quantum Computing Stocks Poised for Six-Figure Returns: IonQ and QuantumX

on: Sat, Dec 13th 2025

by: AOL

Quantum Computing Stocks to Watch in 2025: IonQ, D-Wave, and Quantum Motion

on: Sat, Nov 15th 2025

by: investors.com

Quantum Computing Stocks: A Snapshot of AMD, Qualcomm, IonQ, and IBM

on: Thu, Oct 16th 2025

by: The Motley Fool

Want to Invest in Quantum Computing? 5 Stocks That Are Great Buys Right Now | The Motley Fool

on: Tue, Dec 16th 2025

by: Finbold | Finance in Bold