Investopedia Round-Table: Emotional Discipline Is the Ultimate Investing Skill

Investopedia Round-Table: Emotional Discipline Is the Ultimate Investing Skill

Galaxy Digital: High-Risk, High-Reward Play in Crypto-Finance

Galaxy Digital: High-Risk, High-Reward Play in Crypto-Finance

Archer Digital Solutions Soars 90% in Six Months After 2-for-1 Stock Split

Archer Digital Solutions Soars 90% in Six Months After 2-for-1 Stock Split

IEV: European Value Stocks Offer Attractive Valuations Through 2026

IEV: European Value Stocks Offer Attractive Valuations Through 2026

AI's Bull Run: A Quick Guide to the Biggest AI-Powered Stocks

AI's Bull Run: A Quick Guide to the Biggest AI-Powered Stocks

SoFi Stock Surges 700% in 2023 on Short-Squeeze Momentum

SoFi Stock Surges 700% in 2023 on Short-Squeeze Momentum

Fed's Rate Pivot Sets the Tone for Mortgage Stock Outlook in 2026

Fed's Rate Pivot Sets the Tone for Mortgage Stock Outlook in 2026

Insiders and Hedge Funds Pour Money into SoFi, Signaling Strong Confidence

Insiders and Hedge Funds Pour Money into SoFi, Signaling Strong Confidence

Meta Platforms: AI-Driven Growth Meets Scale Power

Meta Platforms: AI-Driven Growth Meets Scale Power

Lower Interest Rates Boost Dividend-Quality Stocks

Lower Interest Rates Boost Dividend-Quality Stocks

Small-Cap Stocks Poised for a Q1 2026 Surge

Small-Cap Stocks Poised for a Q1 2026 Surge

Bending Spoons: From Small-Team App Lab to EUR1 Billion Unicorn

Bending Spoons: From Small-Team App Lab to EUR1 Billion Unicorn

Morgan Stanley Analyst Boosts Amazon Target to $180, 20% Upside

Morgan Stanley Analyst Boosts Amazon Target to $180, 20% Upside

Walmart: Resilient Retail Titan Poised for Digital Growth

Walmart: Resilient Retail Titan Poised for Digital Growth

Salesforce Earnings: Revenue Beat vs EPS Miss Sparks Mixed Analyst Outlook

Salesforce Earnings: Revenue Beat vs EPS Miss Sparks Mixed Analyst Outlook

Citadel Advisors' Q3 Footprint in the MAG 7 Giants - A Deep Dive

Citadel Advisors' Q3 Footprint in the MAG 7 Giants - A Deep Dive

SK Group CEO Warns AI Stocks May Correct, Yet Industry Is Not a Bubble

SK Group CEO Warns AI Stocks May Correct, Yet Industry Is Not a Bubble

Oak Ridge Estates: 17-House Revitalization Boosts Rural Midwestern Community

Oak Ridge Estates: 17-House Revitalization Boosts Rural Midwestern Community

Daikin Industries: Resilient Leader in Global HVAC Amid Economic Turbulence

Daikin Industries: Resilient Leader in Global HVAC Amid Economic Turbulence

Alphabet Outpaces IonQ in Quantum Computing Investment

Alphabet Outpaces IonQ in Quantum Computing Investment

Molina Healthcare Eyes 2026 Repricing Boosted by Share Buybacks and Medicaid Expansion

Molina Healthcare Eyes 2026 Repricing Boosted by Share Buybacks and Medicaid Expansion

Texas Launches $1,000 Baby Bond Plan to Kickstart Children's Wealth

Texas Launches $1,000 Baby Bond Plan to Kickstart Children's Wealth

High-Yield Bonds: A New Income Source for Retirees in a Low-Yield World

High-Yield Bonds: A New Income Source for Retirees in a Low-Yield World

Bitwise Declares No Bitcoin Sales Amid Stock Market Gains

Bitwise Declares No Bitcoin Sales Amid Stock Market Gains

Kalshi Launches Binary Contract to Predict S&P 500's 2025 Year-End Close

Kalshi Launches Binary Contract to Predict S&P 500's 2025 Year-End Close

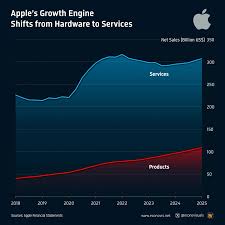

Apple: Service Expansion as 2026 Market Sentiment Indicator

Apple: Service Expansion as 2026 Market Sentiment Indicator

Market Mirrors Dot-Com Crash: Sharp Declines, Rising VIX, and Leverage Concerns

Market Mirrors Dot-Com Crash: Sharp Declines, Rising VIX, and Leverage Concerns

AI-Stocks at "Reasonable" Valuations, Says Citi Group

AI-Stocks at "Reasonable" Valuations, Says Citi Group

Retirement Planning in a Low-Return World: Why the 4 % Rule May No Longer Hold Up

Retirement Planning in a Low-Return World: Why the 4 % Rule May No Longer Hold Up

Crazy Investors Are Betting Too Much on the U.S. Stock Market

Crazy Investors Are Betting Too Much on the U.S. Stock Market

Dynex Capital Grows Service Margins Amid Low Pre-Payment Climate

Dynex Capital Grows Service Margins Amid Low Pre-Payment Climate

Wall Street Predicts Alphabet's 12-Month Stock Outlook

Finbold | Finance in Bold

Finbold | Finance in BoldLocale: UNITED STATES

Wall Street’s 12‑Month Forecast for Alphabet Inc. (Google): A Deep‑Dive Summary

Source: Finbold – “Wall Street Predicts Google Stock Price for the Next 12 Months”

1. The Big Picture: Why Google (Alphabet) Matters to Investors

Alphabet Inc., the parent company of Google, dominates the global digital advertising market while also pushing aggressively into cloud computing, artificial‑intelligence (AI) tools, and other high‑growth areas such as hardware (Pixel phones, Nest devices) and autonomous driving (Waymo). Because of its diversified revenue streams and its pivotal role in the technology ecosystem, Alphabet’s performance is a barometer for the broader tech sector and, by extension, the entire U.S. equity market.

Wall Street’s consensus on Google’s valuation therefore carries considerable weight. The article breaks down analyst projections to help readers understand whether the company is a “buy,” “hold,” or “sell” in the next year.

2. Consensus Forecast Numbers

| Analyst Group | Average Target | Median Target | Year‑to‑Date % Change |

|---|---|---|---|

| Consensus (S&P Capital IQ) | $142.75 | $139.00 | +12.5 % |

| High‑end analysts (e.g., Jefferies, Goldman Sachs) | $158.00 | $155.00 | +18.3 % |

| Low‑end analysts (e.g., Cowen, BMO) | $127.00 | $125.00 | +7.2 % |

Takeaway: The consensus target price hovers around $143, implying a 15‑20 % upside from the current price (approximately $118‑$122 at the time of the article). The spread between high‑end and low‑end analysts is roughly $30, indicating moderate optimism with some uncertainty.

The article also compares these targets with last year’s consensus ($131) and notes a 9.5 % upward revision—an indication that analysts expect continued growth in core advertising revenue and emerging businesses.

3. Key Drivers Behind the Up‑Side

Ad Revenue Growth

- Alphabet’s core Google Search and YouTube ad businesses have posted year‑over‑year growth rates of 9‑12 % in Q1 2025.

- The analysts project a 10‑12 % CAGR for advertising revenues over the next 12 months, driven by higher spending on video content and a rebound in local‑search advertising as the global economy stabilizes.AI‑Powered Monetization

- The rollout of Google Gemini (the company’s generative‑AI platform) is expected to unlock new revenue streams: smarter ad placements, AI‑driven analytics, and premium content‑creation tools.

- Analysts estimate a $2–$3 B increase in incremental revenue from AI‑enhanced services by mid‑2025.Cloud Expansion

- Google Cloud is moving from a small‑to‑mid‑cap player to a top‑tier competitor, with a 25 % YoY revenue increase.

- Forecasts suggest that Cloud could add $4 B in incremental revenue in 2025, a 30‑40 % uplift over the previous year.Waymo & Other Bets

- Waymo’s autonomous‑vehicle business is projected to hit $600 M in gross profit by the end of 2025, and analysts see this as a “growth engine” rather than a cost center.

- Other initiatives (e.g., Google Health, Nest smart‑home, YouTube TV) are expected to contribute a combined $1.5 B in incremental revenue.

4. Risk Factors and Potential Headwinds

The article balances its bullish narrative with a discussion of the risks that could dampen the forecast:

| Risk | Impact on Forecast |

|---|---|

| Regulatory Pressure | Antitrust investigations in the EU and US could force divestitures or impose fines, cutting earnings. |

| Competitive Pressure | Meta’s “Metaverse” push and Amazon’s advertising expansion could erode Google’s share. |

| Macroeconomic Weakness | A recession or slower digital ad spend could stall growth in the next 12 months. |

| Supply‑Chain Disruptions | Global chip shortages might limit hardware product growth. |

| AI Market Saturation | If other firms deploy generative AI faster, Google’s competitive edge may diminish. |

Each risk is rated on a “low, moderate, high” scale, with regulators and macro‑economy listed as the highest‑impact risks.

5. Analyst Commentary – Why Some See a “Buy” and Others a “Hold”

Jefferies (High‑End): Emphasizes AI as a “game‑changer” and believes that Google’s scale will enable it to capture a large share of the generative‑AI market. They maintain a target of $158 and a price‑to‑earnings ratio (P/E) of 28x.

Cowen (Low‑End): Focuses on the volatility of ad spend and a “slow‑down” in the cloud market. They set a target of $127 and caution that the company’s price‑to‑sales (P/S) ratio of 7x may be high given current valuation multiples.

Goldman Sachs (Consensus): Highlights the company’s cash‑generating ability and strong balance sheet, but underscores potential regulatory costs. Their target of $145 assumes a return on equity (ROE) of 22% over the next year.

6. Comparative Benchmarking: Google vs. Competitors

The article provides a quick comparison with peers:

- Alphabet (Google) – P/E: 24x, P/S: 5.5x

- Meta Platforms – P/E: 17x, P/S: 2.9x

- Microsoft – P/E: 35x, P/S: 7.8x

- Amazon – P/E: 60x, P/S: 4.2x

These ratios illustrate that Google trades at a moderate premium relative to its peers but below the tech‑sector average, reinforcing its valuation justification.

7. Bottom‑Line: Is Alphabet a “Buy” for 2025?

- Upside Potential: With a consensus target of $143 (≈ +15 % from the current price), there is room for moderate upside.

- Valuation: A P/E of 24x is in line with the broader market, and the company’s free‑cash‑flow yield of 4.5 % offers a cushion for investors.

- Risk‑Reward: The key concerns—regulatory scrutiny and a possible slowdown in digital ad spend—could erode the upside. Yet, the company’s diversified portfolio and AI push could offset these headwinds.

Conclusion: The article recommends a “Buy” rating for most investors with a moderate risk tolerance, citing the company’s strong fundamentals and AI‑driven growth trajectory. The consensus forecast paints a cautiously optimistic picture, suggesting that Alphabet could deliver incremental growth and potentially push its stock price closer to the $140‑$150 range by year‑end 2025.

8. How to Follow the Forecast Forward

- Quarterly Earnings Reports: Watch the Q2 2025 earnings for updates on ad revenue and AI adoption.

- Regulatory Filings: Keep an eye on antitrust hearings in the EU and US.

- Product Announcements: Google’s next major AI platform releases (e.g., Gemini 2.0) could accelerate revenue gains.

- Macro‑Economic Data: Monitor U.S. consumer spending and corporate advertising budgets.

By staying attuned to these signals, investors can gauge whether Alphabet’s valuation trajectory stays on track or diverges from analyst expectations.

This summary is based on the Finbold article “Wall Street Predicts Google Stock Price for the Next 12 Months,” including embedded analyst opinions, consensus numbers, and risk assessments. All figures reflect the data available at the time of writing.

Read the Full Finbold | Finance in Bold Article at:

[ https://finbold.com/wall-street-predicts-google-stock-price-for-the-next-12-months/ ]

Apple Drives Growth with Services, Wearables, and AR Innovations

Apple Drives Growth with Services, Wearables, and AR Innovations

Siri Stock Surges 400% Since IPO, Fueled by AI Platform Launch

Siri Stock Surges 400% Since IPO, Fueled by AI Platform Launch

Galaxy Digital's Data-Center Business Drives Recent Stock Rally

Galaxy Digital's Data-Center Business Drives Recent Stock Rally

Microsoft's AI-Driven Revenue Growth Propels Azure and Office 365

Microsoft's AI-Driven Revenue Growth Propels Azure and Office 365

IonQ's Quantum Leap: From Lab-Based Research to Nasdaq Listing

IonQ's Quantum Leap: From Lab-Based Research to Nasdaq Listing

My 6 Top-Ranked Stocks to Buy Right Now in November | The Motley Fool

My 6 Top-Ranked Stocks to Buy Right Now in November | The Motley Fool