[ Thu, Feb 26th ]: Toronto Star

[ Thu, Feb 26th ]: KCCI Des Moines

[ Thu, Feb 26th ]: WNYT NewsChannel 13

[ Thu, Feb 26th ]: This is Money

[ Thu, Feb 26th ]: London Evening Standard

[ Thu, Feb 26th ]: WSB-TV

[ Thu, Feb 26th ]: Dallas Morning News

[ Thu, Feb 26th ]: WSFA

[ Thu, Feb 26th ]: ThePrint

[ Thu, Feb 26th ]: investorplace.com

[ Thu, Feb 26th ]: CNBC

[ Thu, Feb 26th ]: The New Zealand Herald

[ Thu, Feb 26th ]: fox17online

[ Thu, Feb 26th ]: Post and Courier

[ Thu, Feb 26th ]: The Globe and Mail

[ Thu, Feb 26th ]: WJBF Augusta

[ Thu, Feb 26th ]: MoneyWeek

[ Thu, Feb 26th ]: American Association of Individual Investors

[ Thu, Feb 26th ]: Business Insider

[ Thu, Feb 26th ]: Investopedia

[ Thu, Feb 26th ]: NBC DFW

[ Thu, Feb 26th ]: The Topeka Capital-Journal

[ Thu, Feb 26th ]: Goodreturns

[ Thu, Feb 26th ]: Finbold | Finance in Bold

[ Thu, Feb 26th ]: moneycontrol.com

[ Thu, Feb 26th ]: CoinTelegraph

[ Thu, Feb 26th ]: WTOP News

[ Thu, Feb 26th ]: The Motley Fool

[ Thu, Feb 26th ]: reuters.com

[ Thu, Feb 26th ]: Seeking Alpha

[ Thu, Feb 26th ]: SecurityWeek

[ Wed, Feb 25th ]: CNBC

[ Wed, Feb 25th ]: legit

[ Wed, Feb 25th ]: Goodreturns

[ Wed, Feb 25th ]: CBS News

[ Wed, Feb 25th ]: The Globe and Mail

[ Wed, Feb 25th ]: moneycontrol.com

[ Wed, Feb 25th ]: MarketWatch

[ Wed, Feb 25th ]: CoinTelegraph

[ Wed, Feb 25th ]: Toronto Star

[ Wed, Feb 25th ]: WDAF

[ Wed, Feb 25th ]: WTOP News

[ Wed, Feb 25th ]: Seeking Alpha

[ Wed, Feb 25th ]: The Motley Fool

[ Wed, Feb 25th ]: Business Today

[ Wed, Feb 25th ]: Forbes

[ Wed, Feb 25th ]: ABC7 San Francisco

[ Wed, Feb 25th ]: Fortune

GLPI: Undervalued Opportunity Amidst Gaming Concerns

Locale: UNITED STATES

February 26th, 2026 - The gaming and leisure landscape is currently navigating a period of cautious optimism, and within it, Gaming and Leisure Properties (GLPI) stands out as a potentially undervalued opportunity for investors. While macroeconomic headwinds and concerns surrounding regional gaming revenue growth persist, a closer examination reveals a REIT with strong fundamentals, a compelling dividend yield exceeding 9%, and a portfolio built for resilience.

The Current Climate: Headwinds and Hesitation

The past year has seen a palpable shift in investor sentiment towards the gaming sector. Rising interest rates and persistent inflation continue to squeeze consumer discretionary spending - the lifeblood of casinos and entertainment venues. Simultaneously, the explosive growth of online gaming platforms represents a significant, evolving competitive threat to traditional brick-and-mortar establishments, particularly those reliant on regional demographics. This has naturally led to anxieties surrounding the sustainability of regional gaming revenues, traditionally a strong pillar for REITs like GLPI.

Adding to the pressure is the performance of Penn National Gaming (PENN), GLPI's largest tenant. While PENN has undertaken strategic initiatives to navigate these challenges, including its focus on omnichannel experiences and debt reduction, investor apprehension remains. This combination of macroeconomic factors, competitive pressures, and tenant-specific concerns has collectively dampened the market's enthusiasm for gaming and leisure properties.

Gaming and Leisure Properties: A Fortress of Income?

Despite the prevailing pessimism, GLPI presents a compelling case for consideration. The REIT operates as a leading triple-net lease REIT, meaning it owns gaming and entertainment venues and leases them to operators like Penn National. This structure significantly mitigates operational risk - tenants are responsible for property taxes, insurance, and maintenance, providing GLPI with a stable and predictable income stream.

Key Strengths of the GLPI Model:

- Inflation-Protected Revenue: A cornerstone of GLPI's stability lies in its lease agreements. Most contracts include built-in rent escalations tied to inflation indices like the CPI, effectively shielding the REIT from eroding purchasing power. This is particularly crucial in the current environment.

- Portfolio Diversification (Beyond Penn): While PENN represents a substantial portion of GLPI's revenue, the REIT has actively worked to diversify its tenant base. Investments in properties leased to other regional operators, as well as exploring opportunities in entertainment and hospitality beyond gaming, are reducing concentration risk. Recent acquisitions have broadened the portfolio, demonstrating a commitment to a more balanced revenue profile.

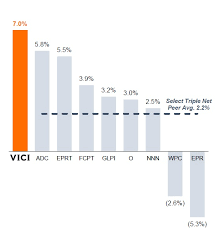

- Robust Financial Health: GLPI boasts a healthy balance sheet with a manageable debt load and a strong investment-grade credit rating (currently at BBB by S&P). This financial strength provides the REIT with flexibility to pursue strategic acquisitions, navigate challenging economic conditions, and maintain its attractive dividend.

- A Generous Dividend Yield: Currently yielding over 9%, GLPI's dividend stands out in a low-interest-rate environment. This makes it particularly appealing to income-seeking investors, offering a substantial return on investment.

- Strategic Capital Allocation: GLPI has demonstrated a disciplined approach to capital allocation, prioritizing accretive acquisitions and strategic investments that enhance portfolio quality and long-term growth potential.

Valuation Considerations and Future Outlook

Currently, the market appears to be discounting GLPI's long-term prospects. A normalized earnings multiple suggests significant upside potential if macroeconomic conditions stabilize and regional gaming revenues demonstrate resilience. The REIT's current price-to-funds from operations (FFO) ratio appears conservative compared to peers, suggesting the market isn't fully appreciating its strengths. Furthermore, increased adoption of sports betting - even if largely online - can create synergistic revenue opportunities for properties housing retail sportsbooks.

Risks to Consider

Of course, investing in GLPI isn't without risks. A prolonged economic downturn or a sharper-than-expected decline in regional gaming revenues could negatively impact the REIT's performance. Increased competition from online platforms remains a significant threat. Furthermore, any unforeseen financial difficulties faced by Penn National Gaming could pose a risk to GLPI's rental income. Vigilant monitoring of PENN's performance and the evolving regulatory landscape surrounding online gaming is crucial.

Conclusion: A Compelling Opportunity for Patient Investors

Gaming and Leisure Properties is not immune to the challenges facing the gaming sector. However, its strong fundamentals, diversified portfolio, inflation-protected lease structures, and exceptionally high dividend yield position it as a compelling investment opportunity. While a cautious approach to regional gaming is warranted, GLPI's resilience and long-term growth potential make it an attractive prospect for patient investors seeking a reliable income stream and potential capital appreciation. A gradual improvement in macroeconomic conditions, coupled with the stabilization of regional gaming revenues, could serve as catalysts for a significant rally in GLPI's share price.

Read the Full Seeking Alpha Article at:

[ https://seekingalpha.com/article/4875153-gaming-and-leisure-properties-market-still-undervalues-this-high-yield-casino-reit ]

[ Mon, Feb 23rd ]: The Motley Fool

[ Mon, Feb 23rd ]: The Motley Fool

[ Sun, Feb 22nd ]: Seeking Alpha

[ Sat, Feb 21st ]: Seeking Alpha

[ Fri, Feb 20th ]: Seeking Alpha

[ Mon, Feb 16th ]: Seeking Alpha

[ Sun, Feb 01st ]: Seeking Alpha

[ Tue, Jan 27th ]: The Motley Fool

[ Wed, Jan 21st ]: Seeking Alpha

[ Tue, Jan 20th ]: Seeking Alpha

[ Mon, Dec 08th 2025 ]: Seeking Alpha

[ Mon, Nov 17th 2025 ]: The Motley Fool