: High Yield, High Risk?")

Arbor Realty Trust Faces Potential Permanent Damage

Seeking Alpha

Seeking AlphaLocale: UNITED STATES

Thursday, March 12th, 2026 - Arbor Realty Trust (ABR) has been under intense pressure in recent months, with its stock price experiencing a substantial decline. While some market observers suggest a potential buying opportunity exists, a deeper analysis reveals concerning signals that point toward more than just a temporary downturn. The question isn't if ABR is facing headwinds, but whether the damage is potentially permanent.

A REIT Navigating a Shifting Landscape

Arbor Realty Trust operates as a mortgage REIT, focusing primarily on the commercial mortgage market. Unlike traditional direct lenders, ABR functions as a capital provider, originating, securitizing, and managing mortgages - essentially, facilitating lending for other institutions. This model relies heavily on volume and the spread between funding costs and mortgage rates. The company's strategy involves acquiring and investing in commercial mortgages and mortgage-backed securities (MBS), generating revenue through interest income and fees.

The Plunge and the Allure of Value

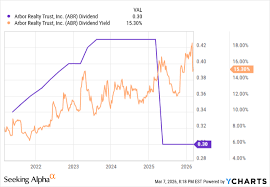

Since early 2022, ABR's stock price has plummeted from a high of approximately $21 to around $11.60 as of recent reporting. This significant decrease naturally draws the attention of value investors, who often seek out undervalued assets. However, a closer examination of the underlying factors suggests that this decline isn't simply a market overreaction, but a justifiable response to mounting challenges. The initial optimistic read of a value play is quickly tempered by a more sobering reality.

A Cascade of Challenges: Beyond Interest Rates

The current environment presents a multi-faceted challenge for ABR. While rising interest rates are a primary concern - making new mortgage originations more expensive and eroding the value of existing fixed-rate portfolios - they represent only one piece of the puzzle. Several other factors are converging to create a potentially unsustainable situation for the REIT.

- Macroeconomic Headwinds: A slowing economy, or even a recession, would inevitably lead to an increase in loan defaults. Commercial real estate, particularly sectors like office spaces, is already feeling the strain of changing work patterns and economic uncertainty. This directly impacts ABR's income and the value of its assets.

- Margin Compression: ABR's profit margins are demonstrably shrinking, and there are few indications of a near-term reversal. Competition within the commercial mortgage market is fierce, and the pressure to offer competitive rates is exacerbating the margin squeeze.

- Deteriorating Credit Quality: The most significant concern lies in the quality of the mortgages within ABR's portfolio. Early indicators suggest a rising risk of defaults, particularly in sectors vulnerable to economic downturns. This isn't simply about a handful of troubled loans; it represents a systemic risk to the company's financial stability.

- Securitization Complications: The ability to securitize mortgages and sell them off to investors is critical to ABR's business model. However, with increased market volatility and concerns about credit quality, securitization becomes more difficult and expensive, further impacting profitability.

Is Permanent Damage Looming?

The core question is whether these challenges constitute a temporary setback or herald a more permanent impairment of ABR's business. The mounting evidence suggests the latter. Critically, the company's management team has, thus far, demonstrated a limited capacity to adapt to the rapidly changing economic climate. While cost-cutting measures have been implemented, they appear insufficient to offset the combined impact of higher interest rates, shrinking margins, and potential loan defaults.

Furthermore, the company's reliance on originating and securitizing mortgages makes it particularly vulnerable to market fluctuations. Unlike REITs that hold physical properties, ABR's assets are largely illiquid and susceptible to rapid devaluation in a rising rate environment.

Valuation and Outlook - A Cautionary Stance

Despite the depressed price, ABR's current valuation doesn't adequately reflect the significant risks facing the company. While the allure of a 'bargain' is tempting, the potential for further price declines outweighs the potential for a quick rebound. A careful assessment reveals that this isn't a compelling value opportunity, but rather a potential value trap.

Recommendation: Given the significant headwinds and the lack of demonstrable adaptation from management, a hold or even sell recommendation is prudent at this time. Investors should closely monitor the company's financial performance, particularly its delinquency rates and ability to maintain margins, before considering any investment. The risks are simply too high, and the uncertainties surrounding ABR's future performance are too numerous.

Read the Full Seeking Alpha Article at:

https://seekingalpha.com/article/4881574-arbor-realty-market-pricing-temporary-pain-as-permanent-damage

Seeking Alpha

on: Wed, Jan 28th

by: Seeking Alpha

Arbor Realty Trust (ARY) Benefits from Yield Curve Improvement

Benefits from Yield Curve Improvement")

on: Tue, Mar 10th

by: WSB-TV

on: Sun, Mar 08th

by: Seeking Alpha

on: Wed, Feb 11th

by: Seeking Alpha

on: Tue, Feb 03rd

by: Seeking Alpha

Davenport Shifts to Value Investing Amid Economic Uncertainty

on: Mon, Nov 17th 2025

by: The Motley Fool

AGNC Investment Corp: A Three-Year Outlook on Mortgage-Backed REIT Performance

on: Sun, Mar 08th

by: Seeking Alpha

on: Tue, Feb 03rd

by: Seeking Alpha

on: Tue, Feb 03rd

by: Business Insider

Precious Metals Markets Face Turbulence: Silver Plummets, Gold Struggles

on: Tue, Jan 27th

by: AOL

on: Tue, Jan 27th

by: The Motley Fool

on: Mon, Jan 26th

by: Seeking Alpha