by: American Association of Individual Investors

Graham Holdings Outperforms Covissta: A Comparative Analysis

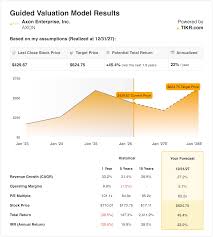

Axon Faces DOJ Review, Stock Price Drops

The Motley Fool

The Motley FoolLocale: UNITED STATES

Thursday, February 26th, 2026 - Axon Enterprise (AXON) has been a standout performer in the public safety technology sector, rapidly growing to become a dominant force in equipping law enforcement agencies. However, the company's trajectory is facing a new challenge: a Department of Justice (DOJ) review into its data handling practices. While Axon continues to demonstrate robust financial performance and a compelling long-term outlook, this investigation casts a shadow over its future and has already impacted its stock price.

A Decade of Growth Built on Modern Policing Needs

Axon's success isn't accidental. For over a decade, the company, originally known for its TASER devices, has successfully transitioned into a comprehensive provider of connected policing solutions. These solutions encompass not only less-lethal weapons, but crucially, a suite of software and data services - including body-worn cameras, digital evidence management systems (DEMS), and records management software. This pivot towards recurring revenue has been a key driver of Axon's impressive growth and improved profitability.

The demand for these technologies has surged as police departments nationwide grapple with increasing demands for transparency, accountability, and officer safety. Body-worn cameras, in particular, have become ubiquitous, offering a means to document interactions between officers and the public, potentially mitigating liability and improving trust. Axon's integrated system, offering a seamless workflow from data capture to analysis and storage, has positioned it as the preferred vendor for many agencies.

In the most recent quarterly report, Axon demonstrated this continued strength, reporting a 23% year-over-year revenue increase, exceeding analyst expectations. This growth isn't just topline; strong margins indicate Axon's ability to maintain pricing power and operate efficiently - characteristics that are attractive to investors.

The DOJ Review: Data Privacy Concerns Take Center Stage

The current DOJ review, however, represents a significant headwind. The investigation centers on how Axon collects, stores, and utilizes the vast amounts of data generated by its devices. While Axon maintains a commitment to privacy, the DOJ's scrutiny signals a potential for legal challenges and heightened regulatory oversight. This isn't a new area of concern - civil liberties groups and privacy advocates have previously raised questions about Axon's data practices. However, the involvement of the DOJ elevates the stakes considerably.

The core of the issue revolves around the potential for misuse of sensitive data captured by body cameras and other devices. Concerns include data retention policies, access controls, and the possibility of data being shared with third parties without proper consent or authorization. The sheer volume of data Axon handles - encompassing potentially millions of hours of video footage and associated metadata - presents a complex challenge for ensuring privacy and compliance.

Market Reaction and Future Implications

The market reacted swiftly to the news of the DOJ review, with Axon's stock price experiencing a notable decline. This response is understandable, as investors are factoring in the potential for substantial financial and reputational risks. Potential outcomes range from fines and restrictions on how Axon operates to more severe consequences, such as limitations on its ability to sell certain products or services.

The outcome of the DOJ review is the immediate catalyst for Axon's stock performance. A favorable resolution, confirming Axon's compliance with regulations, could trigger a rebound. Conversely, a negative finding could significantly depress the stock price and force Axon to overhaul its data practices.

Beyond the DOJ: Competitive Landscape and Growth Sustainability

Even if Axon successfully navigates the DOJ review, other challenges remain. The connected policing market is becoming increasingly competitive, with several companies vying for market share. This competition could lead to pricing pressure and reduced margins. Furthermore, maintaining a consistently high growth rate will be difficult as Axon's base revenue increases. The company will need to innovate continuously and expand its product offerings to stay ahead of the curve.

The Verdict: Cautious Optimism Remains

Axon Enterprise remains a fundamentally strong company with a compelling long-term thesis. Its technology is undeniably essential for modern policing, and its recurring revenue model provides a degree of stability. However, the DOJ review introduces a material risk that investors cannot ignore. A cautious approach is warranted until the outcome of the review is known. The future of connected policing is bright, but Axon's path forward is currently clouded by regulatory uncertainty.

Read the Full The Motley Fool Article at:

https://www.fool.com/investing/2026/02/26/axons-incredible-growth-returns-heres-the-bad-news/

The Motley Fool

on: Tue, Feb 03rd

by: CNBC

on: Tue, Feb 24th

by: The Motley Fool

on: Thu, Feb 19th

by: The Motley Fool

on: Thu, Feb 05th

by: fox17online

Economic Anxieties Grip Market: Recession and Inflation Concerns

on: Sat, Jan 24th

by: Seeking Alpha

on: Thu, Jan 15th

by: The New York Times

on: Wed, Feb 25th

by: The Motley Fool

on: Tue, Feb 24th

by: The Motley Fool

on: Sun, Feb 22nd

by: The Motley Fool

on: Thu, Feb 19th

by: The Motley Fool

on: Tue, Feb 17th

by: The Motley Fool

Novo Nordisk's Cagrisema: A Potential Leap in Diabetes & Obesity Treatment

on: Sat, Feb 14th

by: Seeking Alpha