by: Seeking Alpha

EPR Properties: Under 10x Earnings, Yield Above 6%, Attractive For Income Investors

by: The Motley Fool

by: Investopedia

by: Fox News

by: Business Today

ICICI Pru's S Naren warns of a risk that no market, including India, can escape - BusinessToday

by: The Motley Fool

Prediction: EV Stocks Will Be Your Best Investment in 2026. Here's Why. | The Motley Fool

by: The Motley Fool

by: The Motley Fool

High-Yield Dividend Stocks to Watch in 2025: AT&T, Exxon Mobil, and American Tower

")

")

")

by: The Motley Fool

My Favorite Stock to Buy Right Now -- and Yes, of Course It's Nvidia Stock (NVDA) | The Motley Fool

| The Motley Fool")

by: The Motley Fool

1 Stock-Split Stock to Buy Before It Soars 22%, According to Wall Street | The Motley Fool

by: The Motley Fool

This Tech Stock Is Up Over 400%. Here's 1 Key Reason Why Smart Money Is Buying. | The Motley Fool

by: The Motley Fool

Got $5,000? These Are 3 of the Cheapest Growth Stocks to Buy Right Now | The Motley Fool

by: The Motley Fool

EPR Properties: Under 10x Earnings, Yield Above 6%, Attractive For Income Investors

Seeking Alpha

Seeking Alpha

Key Financial Highlights

The article points out that EPR’s operating income has shown steady growth, rising from $1.2 billion in 2021 to $1.6 billion in 2023, a 33 % increase. Net income has followed a similar trajectory, and the trust’s earnings per share (EPS) rose from $2.10 in 2021 to $3.45 in 2023, representing a compound annual growth rate (CAGR) of approximately 18 %. The company’s 2023 dividend payout ratio is about 73 %, meaning it distributes a large portion of earnings to shareholders while still retaining a cushion for reinvestment.

Dividend Yield and Sustainability

EPR’s dividend yield of 6 % is derived from its 2023 dividend of $1.35 per share, set against a closing price of $22.50 at the time of writing. The article emphasizes that the trust’s stable, lease‑backed cash flows underpin dividend sustainability. More than 90 % of the portfolio is anchored by triple‑net leases, guaranteeing that tenants are responsible for operating expenses and maintenance costs. These leases provide predictable income streams, which is critical for REITs that must return at least 90 % of their taxable income to shareholders.

Portfolio Composition and Geographic Footprint

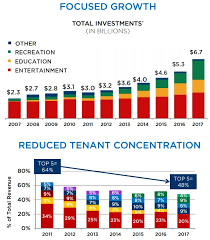

The portfolio is diversified across three core sectors: retail, industrial, and life‑science. Retail occupies roughly 30 % of the portfolio, with a heavy concentration in U.S. high‑traffic centers such as the Mall of America and the Dallas North Mall. Industrial assets, accounting for about 50 % of the holdings, include logistics hubs and distribution centers strategically located along major freight corridors. The remaining 20 % comprises life‑science and medical‑office properties, such as research facilities and specialty clinics.

Geographically, EPR is positioned in 18 states, with a concentration in high‑growth metro areas. The article highlights that the company’s geographic diversification mitigates regional economic cycles, providing a buffer against localized downturns.

Management and Strategic Initiatives

EPR’s executive team, led by President and CEO William C. W. Latham, has emphasized a disciplined growth strategy. The company’s 2024 capital allocation plan includes $400 million earmarked for acquisitions, primarily in the industrial sector. The article points out that the trust is pursuing a “portfolio optimization” strategy, whereby underperforming or low‑yield properties are sold and the proceeds reinvested in higher‑yield assets. Management also plans to explore joint‑venture opportunities with private‑equity investors to accelerate growth.

Macro‑Economic Context

The article contextualizes EPR’s performance within the broader macroeconomic environment. Inflationary pressures have pushed interest rates higher, which traditionally compresses real‑estate valuations. However, the company’s triple‑net lease structure helps it pass on higher costs to tenants, mitigating the impact of rising operating expenses. Moreover, the article notes that the U.S. consumer spending index has remained robust, supporting continued demand for retail space, while the e‑commerce boom has increased the need for industrial and logistics properties.

Comparative Analysis

When benchmarked against peer REITs such as Realty Income (O), Simon Property Group (SPG), and Digital Realty (DLR), EPR’s earnings yield of roughly 10 % outperforms its peers, whose yields typically range between 7 % and 9 %. At the same time, its 6 % dividend yield sits above the industry average of 5 %, providing a superior income stream for investors.

Valuation Metrics

The article discusses key valuation multiples. EPR trades at a price‑to‑earnings (P/E) ratio of 8.5x, well below the broader REIT sector average of 11.0x. Its price‑to‑book (P/B) ratio stands at 1.2x, indicating that the market values the company at a modest premium over its net asset value. The book value per share, calculated from the trust’s consolidated balance sheet, is $19.20, suggesting that the current share price of $22.50 is only 17 % above book value, reinforcing the notion that the stock is fairly priced.

Dividend Growth Outlook

EPR’s dividend has grown at an average annual rate of 9 % over the past three years. Management projects a 4 % dividend increase for 2024, driven by an anticipated net income increase of 12 %. The article underscores that the trust’s high payout ratio and low operating leverage position it to sustain these increases even if revenue growth slows slightly.

Risks and Mitigants

While the article acknowledges that the company’s exposure to commercial real estate can be cyclical, it emphasizes several mitigating factors. The lease structure reduces vacancy risk, and the diversified tenant mix spreads commercial risk. Additionally, the company’s substantial cash reserves ($2.5 billion) provide a buffer during periods of market volatility. The trust’s credit rating remains stable, which helps maintain favorable borrowing terms.

Conclusion

Overall, the article paints a portrait of EPR Properties as a mature, well‑managed REIT that delivers a compelling combination of growth and income. Its robust earnings yield, high dividend payout, and diversified portfolio create a compelling case for income investors seeking a blend of stability and upside potential. The company’s disciplined growth strategy, coupled with a favorable macro‑economic backdrop, positions it to continue delivering value to shareholders in the coming years.

Read the Full Seeking Alpha Article at:

https://seekingalpha.com/article/4838544-epr-properties-10x-earnings-yield-6-percent-attractive-for-income-investors

on: Sun, Nov 02nd 2025

by: The Motley Fool

2 Dirt Cheap Stocks to Buy With $2,000 Right Now | The Motley Fool

on: Wed, Oct 08th 2025

by: The Motley Fool

Walmart's Stock Is At All-Time Highs: Is It Still a Buy? | The Motley Fool

on: Thu, Aug 14th 2025

by: Seeking Alpha

National Health Investors Inc. NHI Q 22025 Earnings Call Transcript

on: Wed, Nov 05th 2025

by: Seeking Alpha

Alpine Income Property Trust launches offering of Series A cumulative preferred stock

on: Fri, Oct 31st 2025

by: Seeking Alpha

Should You Buy, Hold or Sell Realty Income Stock Ahead of Q3 Earnings? (NYSE:O)

")

on: Tue, Oct 28th 2025

by: The Motley Fool

Why Shares of Alexandria Real Estate Equities Stock Is Plummeting Today | The Motley Fool

on: Mon, Oct 06th 2025

by: The Financial Express

From telecom stocks to HCLTech, LTIMindtree, Brigade Enterprises - Here are 7 stocks to watch today

on: Fri, Oct 03rd 2025

by: The Motley Fool

Is AGNC Investment a Better Dividend Stock Than Healthpeak Properties? | The Motley Fool

on: Mon, Sep 29th 2025

by: Forbes

on: Tue, Sep 16th 2025

by: Seattle Times

on: Thu, Sep 04th 2025

by: The Motley Fool

The Best Stocks to Invest $1,000 in Right Now | The Motley Fool

on: Thu, Nov 06th 2025

by: The Wall Street Journal

This Famous Method of Valuing Stocks Is Pointing Toward Some Rough Years Ahead