Ninety One's Stopford Says US at Epicenter of Market Risk

U.S. Market Risk at a Critical Juncture, Analysts Warn

A recent Bloomberg feature quotes investment strategist Andrew Stopford of the asset‑management firm Ninety‑One, who warns that the United States sits at the epicenter of market risk. Stopford, whose firm has gained prominence for its macro‑centric approach to global investing, argues that a confluence of macroeconomic, policy, and geopolitical factors has turned the U.S. into a “risk magnet” that could set off a wave of global turbulence if not managed carefully.

1. The U.S. Debt–Yield Nexus

The article begins by highlighting the sharp rise in U.S. Treasury yields over the past two quarters. The 10‑year Treasury yield has climbed from 2.8 % in early 2023 to 4.5 % in mid‑2025, a surge that has pressured both equity and fixed‑income portfolios worldwide. The rising yields are a direct reflection of the widening U.S. debt‑to‑GDP gap, which now sits at roughly 120 %—a level not seen since the early 1980s.

Stopford cites data from the Treasury Department that the debt ceiling debate has stalled, adding uncertainty to the market. “When debt levels are that high, even a slight uptick in interest rates can erode corporate profitability and reduce equity valuations,” he says. The piece links to a Bloomberg story on the debt ceiling negotiations that underscores the likelihood of a “debt ceiling crisis” if Congress fails to act by the July 15 deadline.

2. Federal Reserve Policy and Inflation Outlook

Another key driver of risk, according to Stopford, is the Federal Reserve’s hawkish stance. The Fed’s most recent policy statement, released on June 5 2025, indicated a 75‑basis‑point rate hike and an ongoing taper of asset‑purchase programs. Analysts project that the Fed will raise rates by a total of 300 basis points through 2026, a pace that could slow U.S. growth sharply.

The article references a Bloomberg analysis on the Fed’s inflation projections, noting that headline inflation has steadied at 2.9 % but core CPI remains stubbornly above the Fed’s 2 % target. The Fed’s willingness to act on inflation is creating a “risk‑reward imbalance” for investors: the potential for a sharp pullback in equity markets if inflation expectations shift further to the right.

3. Geopolitical Tensions and Trade Dynamics

Stopford also flags the geopolitical environment as a significant source of risk. The U.S.–China trade war, which began in 2018, has persisted at a simmering level, with tariffs covering approximately 5 % of U.S. imports. The article links to a Bloomberg story on new tariffs imposed by President Biden’s administration on certain Chinese technology imports, a move that could further strain supply chains.

In addition, the lingering conflict in Eastern Europe continues to keep European markets on edge. The piece cites a Bloomberg report that highlighted the European Central Bank’s recent decision to tighten its bond‑purchase program, a move that could lead to higher borrowing costs for European businesses. The combination of U.S. monetary tightening and European rate hikes could create a “divergent monetary” environment that puts pressure on global capital flows.

4. Market Volatility and Equity Performance

The article tracks the recent performance of major equity indices, noting that the S&P 500 has retraced 7 % in the past month after a brief rally in early May. The Nasdaq Composite has suffered a more pronounced decline, falling 10 % as technology stocks are the most sensitive to yield changes. The Russell 2000, representing small‑cap stocks, has also weakened, indicating that risk‑off sentiment is spreading beyond large caps.

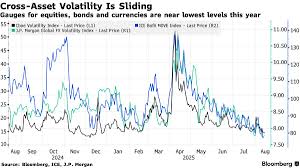

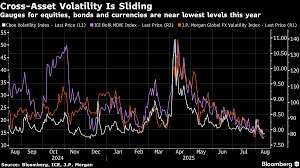

Stopford observes that volatility indices such as the VIX have spiked to their highest levels since the 2008 crisis, a sign that investors are pricing in potential market turbulence. “We’re seeing a classic flight to quality,” he explains, “with bonds and gold gaining traction as safe‑haven assets.”

5. Global Implications and Investment Strategy

Beyond the U.S., the article warns that the risk premium could spill over into emerging markets. A Bloomberg article on the Asian debt markets highlights that Japan’s sovereign yield spread has widened, raising concerns about its debt sustainability. Similarly, Latin American markets, where interest rates have been climbing, are showing signs of distress.

To navigate this landscape, Stopford suggests a diversified, risk‑parity framework that balances exposure across asset classes and geographies. He advises investors to keep a higher proportion of cash or liquid assets to hedge against sudden market dislocations. The piece also notes that Ninety‑One has shifted its portfolio allocation to reduce exposure to high‑yield equities and increase holdings in quality fixed income and defensive sectors.

6. Takeaway

Andrew Stopford’s message is clear: the U.S. stands at a crossroads, where rising debt, a hawkish Fed, persistent trade frictions, and geopolitical tensions converge to create a heightened risk environment. The Bloomberg article paints a sobering picture for investors, emphasizing the need for vigilance, a diversified strategy, and readiness to adjust to rapid shifts in the macro‑economic backdrop. As markets continue to react to these forces, the U.S. remains the epicenter of risk, with implications that extend well beyond its borders.

Read the Full Bloomberg L.P. Article at:

[ https://www.bloomberg.com/news/articles/2025-08-15/ninety-one-s-stopford-says-us-at-epicenter-of-market-risk ]