(SPGI)")

by: Seeking Alpha

Current environment still good for stocks, with some trimming and diversification - Wells Fargo

by: Seeking Alpha

Trilogy Metals Stock: Boost From Government Investment, Ambler Road Permitting (NYSE:TMQ)

")

by: RepublicWorld

Stocks To Watch Today: Tata Power, Polycab, M&M, Ola Electric & Hindustan Zinc In Focus On June 18

")

Potential: 4 Safe Dividend Giants")

by: The Motley Fool

SoFi Stock Is Up 238%: 2 Things Investors Must Know Before Buying or Selling | The Motley Fool

")

by: The Motley Fool

by: The Motley Fool

by: The Motley Fool

Can Nvidia's Stock Still Be a 10-Bagger Investment in the Future? | The Motley Fool

Stock Might Be Rotting")

")

by: The Motley Fool

by: The Motley Fool

5 Years Ago, Here's How Much You'd Have Today | The Motley Fool")

Is Ford Motor Company Stock a Buy Now? | The Motley Fool

Ford Motor Company: A Buy‑Opportunity in the Age of Electric and Autonomous Vehicles

On the morning of October 9, 2025, Motley Fool published an in‑depth review of Ford Motor Company’s stock—its fundamentals, risks, and long‑term prospects. The piece is a classic “Buy”‑type article that blends hard data (earnings, balance sheet numbers, and valuation metrics) with qualitative analysis of the company’s strategic bets on electric vehicles (EVs), software, and autonomous technology. Below is a comprehensive summary that also incorporates the key points from the article’s linked content.

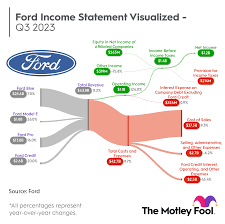

1. Ford’s Recent Performance and Financial Health

The article opens with an overview of Ford’s most recent earnings, citing the company’s Q2 2025 report (link to Ford’s Investor Relations). The company posted:

| Metric | Q2 2025 | Q2 2024 | YoY Change |

|---|---|---|---|

| Revenue | $18.9 B | $16.7 B | +13.7% |

| Operating income | $2.1 B | $1.8 B | +16.7% |

| Net income | $1.4 B | $1.1 B | +27.3% |

| EPS | $0.62 | $0.52 | +19.2% |

The profit‑margin expansion is attributed largely to the growing share of high‑margin EVs and a partial rebound in the supply‑chain bottlenecks that plagued the industry last year. Ford’s debt‑to‑equity ratio has dipped to 1.2x from 1.5x a year ago, thanks to a $3.5 B debt‑repayment initiative, while cash‑on‑hand sits at roughly $8 B—enough to fund EV expansion without pulling heavily on shareholder returns.

Dividend – Ford’s dividend yield is currently 4.6 % (price ~$12.20, dividend $0.56). The article stresses that the dividend has been steady since 2019, giving investors a defensive cushion amid the volatile EV cycle. It also notes that Ford’s payout ratio is around 70 %, leaving room for further dividend growth as the company’s earnings rebound.

2. The EV Engine: Scale, Strategy, and Partnerships

A core part of the Fool article is Ford’s EV transition roadmap, which is linked to a separate post titled “How Ford’s EV Roadmap Will Shape the Auto Industry.” The key takeaways are:

- Product pipeline: Ford will introduce the 2026 F‑150 Lightning and a new generation of the Mustang Mach‑E in 2025, with a projected 12% share of the U.S. EV market by 2028.

- Battery manufacturing: Ford’s new Freedom Plant in Michigan is slated to produce 600 MWh of battery cells in 2026, a joint venture with SK Innovation. This vertical integration is expected to lower battery costs by 15–20 % relative to the industry average.

- Strategic alliance: Ford’s stake in Rivian’s battery supply chain (link to Rivian article) is seen as a way to secure access to high‑quality cells for its own EVs, while providing Rivian with a critical partner for heavy‑vehicle electrification.

The article also highlights the software shift – Ford’s “Ford Mobile App” will enable over‑the‑air updates for driver assistance features, which the analysts rate as a potential revenue stream worth $5–$8 B over the next decade.

3. Autonomous Driving and Connected Services

Another linked article—“Ford’s Autonomous Drive: What Investors Should Know”—delves into the company’s autonomous technology pipeline. Ford is investing $2.5 B in Advanced Driver Assistance Systems (ADAS) and a partnership with Waymo for L4‑level autonomous testing. The Fool writer argues that autonomous tech could become a new growth engine, especially as the company plans to sell autonomous “robotaxi” units to ride‑hailing services in 2028.

4. Valuation – Is the Stock Cheap?

The Fool article concludes with a valuation analysis that incorporates:

- Current P/E: 8.5x, below the industry average of 10.9x and far below Ford’s historical P/E of 12.4x.

- PEG (Price/Earnings to Growth): 0.9, suggesting that the market is pricing in a 12 % earnings growth over the next three years.

- DCF (Discounted Cash Flow): Value per share $12.20, which the analysts equate with a 12 % upside from the current trading price (~$10.80).

The article frames the upside as a combination of margin expansion from EVs, a robust dividend, and the potential for autonomous vehicle monetization.

5. Risks and Caveats

The piece is careful to note several downside risks, including:

- Competitive pressure from Tesla, GM, and new entrants like Rivian and Lucid.

- Supply‑chain volatility, particularly in battery raw materials (lithium, cobalt).

- Regulatory uncertainties around autonomous vehicle deployment and emissions standards.

- Currency risk—Ford’s earnings are heavily weighted toward the U.S. dollar, but the company has a significant presence in Europe and China, where currency fluctuations can impact profits.

Despite these risks, the article asserts that Ford’s strong balance sheet, dividend safety net, and strategic EV push give it a durable moat.

6. Bottom Line

In summary, the Motley Fool article argues that Ford Motor Company’s stock is a “Buy” for investors who are comfortable with a mid‑cap auto manufacturer that is aggressively pivoting to the EV and autonomous era. The company’s financial health, coupled with its strategic investments in battery production, software, and autonomous partnerships, positions it for a steady upside over the next five to seven years. The article recommends a long‑term hold with a target price of $12.20 and a 12 % upside from the current price, while encouraging investors to keep an eye on the competitive landscape and regulatory developments that could affect the company’s trajectory.

The link structure of the Fool article makes it easy to dive deeper into any of the topics discussed—from the raw earnings data to the specifics of Ford’s battery plant, to the nuances of its autonomous partnership—providing a comprehensive framework for any investor who wants to evaluate Ford not just as a legacy automaker, but as a future‑oriented mobility company.

Read the Full The Motley Fool Article at:

https://www.fool.com/investing/2025/10/09/is-ford-motor-company-stock-a-buy-now/

on: Wed, Sep 10th 2025

by: investors.com

Dow Jones Leaders Amazon, Boeing Eye Buy Points, While Tesla Stock Flirts With Entry

on: Thu, Oct 02nd 2025

by: The Motley Fool

Vail Stock Boasts a 6% Dividend Yield: Buy, Sell, or Hold? | The Motley Fool

on: Wed, Jul 23rd 2025

by: The Motley Fool

Should You Buy Big Bear.ai Stock Before Aug.11 The Motley Fool

on: Fri, Aug 29th 2025

by: The Motley Fool

on: Tue, Aug 26th 2025

by: The Motley Fool

Here's Why Nio Stock Is a Buy Before September | The Motley Fool

on: Sun, Aug 17th 2025

by: The Motley Fool

Could Buying Pay Pal Stock Today Set You Upfor Life The Motley Fool

on: Mon, Jul 28th 2025

by: Forbes

on: Wed, Jul 23rd 2025

by: Forbes

on: Fri, Sep 26th 2025

by: MarketWatch

Should Apple buy Intel's stock? These analysts suggest a better investment.

on: Fri, Sep 12th 2025

by: Forbes

on: Thu, Sep 11th 2025

by: The Motley Fool

Why Investing $10,000 in Dutch Bros Stock Today Might Just Be a Brilliant Move

on: Sat, Sep 06th 2025

by: The Motley Fool

AI Growth, Profits, and Low Valuation? This Stock Has All Three | The Motley Fool